How to write a balance sheet for a business plan

Table of Contents

What is a balance sheet?

Elements of a balance sheet, liabilities, how to write a balance sheet, manage your business finances with countingup.

A balance sheet is one of three major financial statements that should be in a business plan – the other two being an income statement and cash flow statement .

Writing a balance sheet is an essential skill for any business owner. And while business accounting can seem a little daunting at first, it’s actually fairly simple.

To help you write the perfect balance sheet for your business plan, this guide covers everything you need to know, including:

- What are assets?

- What are liabilities?

- What is equity?

A balance sheet is a financial statement that shows a business’ “book value”, or the value of a company after all of its debts are paid.

For those inside the business, it provides valuable financial insights, allowing the owners to assess their current financial situation and plan for the future.

For external investors, a balance sheet lets them know whether it’s a worthwhile investment.

Putting a balance sheet together isn’t all that difficult. You just need to know the value of three things:

- Owner’s equity

Once you know these three figures, there’s just a little bit of maths – nothing too scary though.

Assets are items or resources that have financial value. They might be physical items, machinery and vehicles, or they could be intangible items, like copyrights or brand identity .

Assets are separated into two groups based on how quickly you can turn them into cash. There are current assets and fixed assets.

Current assets are things that are fairly simple to value and sell, such as:

- Stock and inventory

- Cash in the bank

- Money owed to you (through unpaid invoices )

- Customer deposits

- Office furniture, equipment or supplies

- Phones or laptops

- Even relatively trivial items like a coffee machine or pool table

Fixed assets are valuable items that take much longer to sell, such as:

- Property or buildings

- Specialised equipment for your business operations

- Investments

- Vehicles

On your balance sheet, the asset column is the simplest. All you need to do is list each item your business owns, along with their individual values, in a separate column. Then, add up the values to get a total at the bottom.

Liabilities are the funds that you owe to other people, banks, or businesses. They can be:

- A business loan (the total, not the monthly payment amount)

- A mortgage or rent payment on a property

- Supplier contracts you owe

- Your accounts payable total

- Other financial obligations, such as paying wages or freelancers for support

- Taxes you’ll owe to HMRC

List these in the same way you did with your assets – on a spreadsheet with their values in a separate column.

When you know the value of your assets and liabilities, working your equity is simple – it’s just the total value of your assets, minus the total value of your liabilities.

Record the owner’s equity in the same column as your liabilities. When you add them all up, it should be the same value as your assets.

After you’ve totalled up your assets, liabilities, and owner’s equity, all that’s left to do is fill in your balance sheet.

Using a spreadsheet, record your assets on the left and your liabilities and owner’s equity on the right.

For example, here’s what a balance sheet might look like for a painter and decorator:

If you’ve recorded everything correctly, both sides should have the same total. Whenever you make a change, the balance sheet will change, but it should still be balanced.

For example, let’s say our painter and decorator sold their equipment. In that case, they’d lose an asset worth £200, but they’d also gain £200 in cash, so the asset total would stay the same.

Alternatively, let’s say they lost the equipment altogether and got no money for it. In that case, they’d lose £200, leaving their asset total at £5,600. Then, they’d have to adjust the other side, so it remains balanced, like this:

If your two totals are not balanced, it’s most likely for one of these reasons:

- Incomplete or missing information

- Incorrect data entry

- A mistake in exchange rates

- And inventory miscount

Basically, if things don’t look right, try not to panic. It’s normally a simple mistake, so go over the figures again and you’ll find the culprit.

The trickiest part of writing a balance sheet for a business plan is accurately recording financial information.

With the Countingup business current account, you’ll have access to a digital record of all your transactions in one simple app, giving you all the financial information you’ll need for a business plan.

Start your three-month free trial today.

Find out more here .

- Counting Up on Facebook

- Counting Up on Twitter

- Counting Up on LinkedIn

Related Resources

Business insurance from superscript.

We’re partnered with insurance experts, Superscript to provide you with small business insurance.

How to register a company in the UK

There are over five million companies registered in the UK and 500,000 new

How to set up a TikTok shop (2024)

TikTok can be an excellent platform for growing a business, big or small.

Best Side Hustle Ideas To Make Extra Money In 2024 (UK Edition)

Looking to start a new career? Or maybe you’re looking to embrace your

How to throw a launch party for a new business

So your business is all set up, what next? A launch party can

How to set sales goals

Want to make manageable and achievable sales goals for your business? Find out

10 key tips to starting a business in the UK

10 things you need to know before starting a business in the UK

How to set up your business: Sole trader or limited company

If you’ve just started a business, you’ll likely be faced with the early

How to register as a sole trader

Running a small business and considering whether to register as a sole trader?

How to open a Barclays business account

When starting a new business, one of the first things you need to

6 examples of objectives for a small business plan

Your new company’s business plan is a crucial part of your success, as

How to start a successful business during a recession

Starting a business during a recession may sound like madness, but some big

What Is a Balance Sheet? Definition, Formulas, and Example

Trevor Betenson

10 min. read

Updated May 2, 2024

Business financial statements consist of three main components: the income statement , statement of cash flows , and balance sheet. The balance sheet is often the most misunderstood of these components—but also extremely beneficial if you understand how to use it.

Check out our free downloadable Balance Sheet Template for more, and keep reading to learn the different elements of a balance sheet, and why they matter.

- What is a balance sheet?

The balance sheet provides a snapshot of the overall financial condition of your company at a specific point in time. It lists all of the company’s assets, liabilities, and owner’s equity in one simple document.

A balance sheet always has to balance—hence the name. Assets are on one side of the equation, and liabilities plus owner’s equity are on the other side.

Assets = Liabilities + Equity

- What is the purpose of the balance sheet?

Put simply, a balance sheet shows what a company owns (assets), what it owes (liabilities), and how much owners and shareholders have invested (equity).

Including a balance sheet in your business plan is an essential part of your financial forecast , alongside the income statement and cash flow statement.

These statements give anyone looking over the numbers a solid idea of the overall state of the business financially. In the case of the balance sheet in particular, what it’s telling you is whether or not you’re in debt, and how much your assets are worth. This information is critical to managing your business and the creation of a business plan.

The balance sheet includes spending and income that isn’t in the income statement (also called a profit and loss statement). For example, the money you spend to repay a loan or buy new assets doesn’t show up in the income statement. And the money you take in as a new loan or a new investment doesn’t show up in the income statement either. The money you are waiting to receive from customers’ outstanding invoices shows up in the balance sheet, not the income statement.

Among other things, your balance sheet can be used to determine your company’s net worth. By subtracting liabilities from assets, you can determine your company’s net worth at any given point in time.

- Key components of the balance sheet

Typically, a balance sheet is divided into three main parts: Assets, liabilities, and owner’s equity.

Assets on a balance sheet or typically organized from top to bottom based on how easily the asset can be converted into cash. This is called “liquidity.” The most “liquid” assets are at the top of the list and the least liquid are at the bottom of the list.

Brought to you by

Create a professional business plan

Using ai and step-by-step instructions.

Secure funding

Validate ideas

Build a strategy

In the context of a balance sheet, cash means the money you currently have on hand. In business planning, the term “cash” represents the bank or checking account balance for the business, also sometimes referred to as “cash and cash equivalents” or “CCE.”

A cash equivalent is an asset that is liquid and can be converted to cash immediately, like a money market account or a treasury bill.

Accounts receivable

Accounts receivable is money people are supposed to pay you, but that you have not actually received yet (hence the “receivables”).

Usually, this money is sales on credit, often from business-to-business (or “B2B”) sales, where your business has invoiced a customer but has not received payment yet.

Inventory includes the value of all of the finished goods and ready materials that your business has on hand but hasn’t sold yet.

Current assets

Current assets are those that can be converted to cash within one year or less. Cash, accounts receivable, and inventory are all current assets, and these amounts accumulated are sometimes referenced on a balance sheet as “total current assets.”

Long-term assets

Long-term assets are also referred to as “fixed assets” and include things that will have a long-standing value, such as land or equipment. Long-term assets typically cannot be converted to cash quickly.

Accumulated depreciation

Accumulated depreciation reduces the value of assets over time. For example, if a business purchases a car, the car will lose value as time goes on.

Total long-term assets

Total long-term assets is used to describe long-term assets plus depreciation on a balance sheet.

Liabilities

Like assets, liabilities are ordered by how quickly a business needs to pay them off. Current liabilities are typically due within one year. Long-term liabilities are due at any point after one year.

Accounts payable

Accounts payable is the money that your business owes to other vendors, the other side of the coin to “accounts receivable.” Your accounts payable number is the regular bills that your business is expected to pay.

Pay attention to whether this number is exceedingly high, especially if your business doesn’t have enough to cover it.

Sales taxes payable

This only applies to businesses that don’t pay sales tax right away, for example, a business that pays its sales tax each quarter. That might not be your business, so if it doesn’t apply, skip it.

Short-term debt

This is debt that you have to pay back within a year—usually any short-term loan. This can also be referred to on a balance sheet as a line item called current liabilities or short-term loans. Your related interest expenses don’t go here or anywhere on the balance sheet; those should be included in the income statement.

Total current liabilities

The above numbers added together are considered the current liabilities of a business, meaning that the business is responsible for paying them within one year.

Long-term debt

These are the financial obligations that it takes more than a year to pay back. This is often a hefty number, and it doesn’t include interest. For example, this number reflects long-term loans on things like buildings or expensive pieces of equipment. It should be decreasing over time as the business makes payments and lowers the principal amount of the loan.

Total liabilities

Everything listed above that you have to pay out or back is added together.

This is the sum of all shareholder money invested in the business and accumulated business profits. Owner’s equity includes common stock, retained earnings, and paid-in-capital.

Paid-in capital

Money is paid into the company as investments. This is not to be confused with the par value or market value of stocks. This is actual money paid into the company as equity investments by owners.

Retained earnings

Earnings (or losses) that have been reinvested into the company, that have not been paid out as dividends to the owners. When retained earnings are negative, the company has accumulated losses. This can also be referred to as “shareholder’s equity.”

This doesn’t apply to all legal structures for a business; if you are a pass-through tax entity , then all profits or losses will be passed on to owners, and your balance sheet should reflect that.

Net earnings

This is an important number—the higher it is, the more profitable your company is. This line item can also be called income or net profit. Earnings are the proverbial “bottom line”: sales less costs of sales and expenses.

Total owner’s equity

Equity means business ownership, also called capital. Equity can be calculated as the difference between assets and liabilities. This can also be referred to as “shareholder’s equity” or “stockholder’s equity.”

Total liabilities and equity

This is the final equation I mentioned at the beginning of this post, assets = liabilities + equity.

- How to use the balance sheet

Your balance sheet can provide a wealth of useful information to help improve financial management. For example, you can determine your company’s net worth by subtracting your balance sheet liabilities from your assets, as noted above.

Overall, the balance sheet gives you insights into the health of your business. It’s a snapshot of what you have (assets) and what you owe (liabilities). Keeping tabs on these numbers will help you understand your financial position and if you have enough cash to make further investments in your business.

Perhaps the most useful aspect of your balance sheet is its ability to alert you to upcoming cash shortages. After a highly profitable month or quarter, for example, business owners sometimes get lulled into a sense of financial complacency if they don’t consider the impact of upcoming expenses on their cash flow .

There are two easy-to-figure ratios that can be computed from the balance sheet to help determine whether your company will have sufficient cash flow to meet current financial obligations:

Current ratio

This measures liquidity to show whether your company has enough current (i.e., liquid) assets on hand to pay bills on-time and run operations effectively. It is expressed as the number of times current assets exceeds current liabilities.

The higher the current ratio, the better. A current ratio of 2:1 is generally considered acceptable for inventory-carrying businesses, although industry standards can vary widely. The acceptable current ratio for a retail business, for example, is different from that of a manufacturer.

Current ratio formula

Current Assets / Current Liabilities

Quick ratio

This ratio is similar to the current ratio but excludes inventory. A quick ratio of 1.5:1 is generally desirable for non-inventory-carrying businesses, but—just as with current ratios—desirable quick ratios differ from industry to industry.

Quick ratio formula

Current Assets – Inventory / Current Liabilities

Knowing your industry’s standards is an important part of evaluating your business’s balance sheet effectively.

- The limits of the balance sheet

Remember, the balance sheet alone doesn’t give you a complete view of your business finances. You’ll want to keep tabs on your profit & loss statement (income statement) and cash flow as well.

Your profit & loss statement will show you the sales you are making and your business expenses and calculates your profitability. This is crucial for understanding the core economics of your business and if you’re building a profitable business, or not.

Your cash flow forecast shows how cash is moving in and out of your business and can help you predict your future cash balances. Fast growth can reduce cash quickly, especially for businesses that carry inventory, so this is a crucial statement to pay attention to as well.

The three statements all work together to provide you with a complete picture of your business. The balance sheet also helps illustrate how cash and profits are very different things .

- Example of a balance sheet

Large businesses will have longer and more complex balance sheets for their businesses, sometimes having separate balance sheets for different segments or departments of their business. A small business balance sheet will be more straightforward and have fewer line items.

Here is a balance sheet from Apple, for example. You’ll see that it includes a complex stockholder’s equity section and several specifically itemized types of long-term assets and liabilities.

Apple’s balance sheet .

You’ll also notice that it says “Period Ending” at the top; this indicates that these numbers are reflective of the time up until the date listed at the top of the column. This terminology is used when you are reporting actual values, not creating a financial forecast for the future.

- Get familiar with your balance sheet

Most companies should update their balance once a month, or whenever lenders ask for an updated balance sheet. Today’s accounting software programs will create your balance sheet for you, but it’s up to you to enter accurate information into the program to generate useful data to work from.

The balance sheet can be an extremely useful financial tool for businesses that understand how to use it properly. If you’re not as familiar with your balance sheet as you’d like to be, now might be a good time to learn more about the workings of your balance sheet and how it can help improve financial management.

Create your balance sheet easily by downloading our Balance Sheet Template , and check out our full guide to write your financial plan.

Trevor is the CFO of Palo Alto Software, where he is responsible for leading the company’s accounting and finance efforts.

Table of Contents

Related Articles

11 Min. Read

How to Create a Sales Forecast

5 Min. Read

How to Improve the Accuracy of Financial Forecasts

8 Min. Read

How to Forecast Personnel Costs in 3 Steps

6 Min. Read

How to Forecast Sales for a Subscription Business

The Bplans Newsletter

The Bplans Weekly

Subscribe now for weekly advice and free downloadable resources to help start and grow your business.

We care about your privacy. See our privacy policy .

The quickest way to turn a business idea into a business plan

Fill-in-the-blanks and automatic financials make it easy.

No thanks, I prefer writing 40-page documents.

Discover the world’s #1 plan building software

Understanding a Balance Sheet (With Examples and Video)

Frances McInnis

Reviewed by

May 3, 2024

This article is Tax Professional approved

Balance sheets can help you see the big picture: the net worth of your small business, how much money you have, and where it’s kept. They’re also essential for getting investors, securing a loan , or selling your business.

So you definitely need to know your way around one. That’s where this guide comes in. We’ll walk you through balance sheets, one step at a time.

I am the text that will be copied.

What is a balance sheet?

The balance sheet is one of the three main financial statements , along with the income statement and cash flow statement .

While income statements and cash flow statements show your business’s activity over a period of time, a balance sheet gives a snapshot of your financials at a particular moment. It incorporates every journal entry since your company launched. Your balance sheet shows what your business owns (assets), what it owes (liabilities) , and what money is left over for the owners ( owner’s equity ).

Because it summarizes a business’s finances, the balance sheet is also sometimes called the statement of financial position. Companies usually prepare one at the end of a reporting period, such as a month, quarter, or year.

The purpose of a balance sheet

Because the balance sheet reflects every transaction since your company started, it reveals your business’s overall financial health. Investors, business owners, and accountants can use this information to give a book value to the business, but it can be used for so much more.

At a glance, you’ll know exactly how much money you’ve put in, or how much debt you’ve accumulated. Or you might compare current assets to current liabilities to make sure you’re able to meet upcoming payments.

The information in your company’s balance sheet can help you calculate key financial ratios, such as the debt-to-equity ratio, a metric which shows the ability of a business to pay for its debts with equity (should the need arise). Even more immediately applicable is the current ratio : current assets / current liabilities. This will tell you whether you have the ability to pay all your debts in the next 12 months.

You can also compare your latest balance sheet to previous ones to examine how your finances have changed over time. You’ll be able to see just how far you’ve come since day one.

Further reading: How to Read a Balance Sheet

A simple balance sheet template

You can download a simple balance sheet template here . You record the account name on the left side of the balance sheet and the cash value on the right.

What goes on a balance sheet

At a high level, a balance sheet works the same way across all business types. They are organized into three categories: assets, liabilities, and owner’s equity.

Let’s start with assets—the things your business owns that have a dollar value.

List your assets in order of liquidity , or how easily they can be turned into cash, sold or consumed. Bank accounts and other cash accounts should come first followed by fixed assets or tangible assets like buildings or equipment with a useful life longer than a year. Even intangible assets like intellectual properties, trademarks, and copyrights should be included. Anything you expect to convert into cash within a year are called current assets.

Current assets include:

- Money in a checking account

- Money in transit (money being transferred from another account)

- Accounts receivable (money owed to you by customers)

- Short-term investments

- Prepaid expenses

- Cash equivalents (currency, stocks, and bonds)

Long-term assets (or non-current assets), on the other hand, are things you don’t plan to convert to cash within a year.

Long-term assets include:

- Buildings and land

- Machinery and equipment (less accumulated depreciation )

- Intangible assets like patents, trademarks, copyrights, and goodwill (you would list the market value of what fair price a buyer might purchase these for)

- Long-term investments

Let’s say you own a vegan catering business called “Where’s the Beef”. As of December 31, your company assets are: money in a checking account, an unpaid invoice for a wedding you just catered, and cookware, dishes and utensils worth $900. Here’s how you’d list your assets on your balance sheet:

| ASSETS | |

|---|---|

| Bank account | $2,050 |

| Accounts receivable | $6,100 |

| Equipment | $900 |

| Total assets | $9,050 |

Liabilities

Next come your liabilities—your business’s financial obligations and debts.

List your liabilities by their due date. Just like assets, you’ll classify them as current liabilities (due within a year) and non-current liabilities (the due date is more than a year away). These are also known as short-term liabilities and long-term liabilities.

Your current liabilities might include:

- Accounts payable (what you owe suppliers for items you bought on credit)

- Wages you owe to employees for hours they’ve already worked

- Loans that you have to pay back within a year

- Credit card debt

And here are some non-current liabilities:

- Loans that you don’t have to pay back within a year

- Bonds your company has issued

Returning to our catering example, let’s say you haven’t yet paid the latest invoice from your tofu supplier. You also have a business loan, which isn’t due for another 18 months.

Here are Where’s the Beef’s liabilities:

Equity is money currently held by your company. This category is usually called “owner’s equity” for sole proprietorships and “stockholders’ equity” or “shareholders’ equity” for corporations. It shows what belongs to the business owners and the book value of their investments (like common stock, preferred stock, or bonds).

Owners’ equity includes:

- Capital (the amount of money invested into the business by the owners)

- Private or public stock

- Retained earnings (all your revenue minus all your expenses and distributions since launch)

Equity can also drop when an owner draws money out of the company to pay themself, or when a corporation issues dividends to shareholders.

For Where’s the Beef, let’s say you invested $2,500 to launch the business last year, and another $2,500 this year. You’ve also taken $9,000 out of the business to pay yourself and you’ve left some profit in the bank.

Here’s a summary of Where’s the Beef’s equity:

| LIABILITIES | |

|---|---|

| Accounts payable | $150 |

| Long-term debt | $2,000 |

| Total liabilities | $2,150 |

The balance sheet equation

This accounting equation is the key to the balance sheet:

Assets = Liabilities + Owner’s Equity

Assets go on one side, liabilities plus equity go on the other. The two sides must balance—hence the name “balance sheet.”

It makes sense: you pay for your company’s assets by either borrowing money (i.e. increasing your liabilities) or getting money from the owners (equity).

A sample balance sheet

We’re ready to put everything into a standard template ( you can download one here ). Here’s what a sample balance sheet looks like, in a proper balance sheet format:

Nice. Your balance sheet is ready for action.

Great. Now what do I do with it?

Because the balance sheet reflects every transaction since your company started, it reveals your business’s overall financial health. At a glance, you’ll know exactly how much money you’ve put in, or how much debt you’ve accumulated. Or you might compare current assets to current liabilities to make sure you’re able to meet upcoming payments.

You can also compare your latest balance sheet to previous ones to examine how your finances have changed over time. You’ll be able to see just how far you’ve come since day one. If you need help understanding your balance sheet or need help putting together a balance sheet, consider hiring a bookkeeper .

Here’s some metrics you can calculate using your balance sheet:

- Debt-to-equity ratio (D/E ratio): Investors and shareholders are interested in the D/E ratio of a company to understand whether they raise money through investment or debt. A high D/E ratio shows a business relies heavily on loans and financing to raise money.

- Working capital : This metric shows how much cash you would hold if you paid off all your debts. It signals to investors and lenders how capable you are to pay down your current liabilities.

- Return on Assets: A formula for calculating how much net income is being earned relative to the assets owned. The more income earned relative to the amount of assets, the higher performing a business is considered to be.

Next, we’ll cover the three most important ratios that you can calculate using your balance sheet: the current ratio, the debt-to-equity ratio, and the quick ratio.

The current ratio

Can your company pay its debts? The current ratio measures the liquidity of your company—how much of it can be converted to cash, and used to pay down liabilities. The higher the ratio, the better your financial health in terms of liquidity .

The ratio for finding your current ratio looks like this:

Current Ratio = Current Assets / Current Liabilities

You should aim to maintain a current ratio of 2:1 or higher. Meaning, your company holds twice as much value in assets as it does in liabilities. If you had to, you could pay off all the money you owe two times over.

Once you drop below a current ratio of 2:1, your liquidity isn’t looking so good. And if you dip below 1:1, you’re entering hot water. That means you don’t have enough liquidity to pay off your debts.

You can improve your current ratio by either increasing your assets or decreasing your liabilities.

The quick ratio

Also called the acid test ratio, the quick ratio describes how capable your business is of paying off all its short-term liabilities with cash and near-cash assets. In this case, you don’t include assets like real estate or other long-term investments. You also don’t include current assets that are harder to liquidate, like inventory. The focus is on assets you can easily liquidate.

Here’s how you get the quick ratio:

Quick Ratio = (Cash and Cash Equivalents + Marketable Securities + Accounts Receivable) / Current Liabilities

If your ratio is 1:1 or better, you’re sitting pretty. That means you’ve got enough quick-to-liquidate assets to cover all your short term liabilities in a pinch.

The debt-to-equity ratio

Similar to the current ratio and quick ratio, the debt-to-equity ratio measures your company’s relationship to debt. Only, in this case, the key value is your total equity.

This ratio tells you how much your company depends upon equity to keep running versus how much it depends on outside lenders. It’s calculated like this:

Debt to Equity Ratio = Total Outside Liabilities / Owner or Shareholders’ Equity

Generally speaking, a 2:1 ratio is considered acceptable. If the ratio gets bigger, you start running into trouble. It means your business relies heavily on debt to keep running, which turns off investors. The higher the ratio, the higher the chance that, in the event you need to pay off your debt, you’ll use up all your earnings and cash flows—and investors will end up empty-handed.

Examples of balance sheet analysis

We’ll do a quick, simple analysis of two balance sheets, so you can get a good idea of how to put financial ratios into play and measure your company’s performance.

Annie’s Pottery Palace, a large pottery studio, holds a lot of its current assets in the form of equipment—wheels and kilns for making pottery. Accounts receivable play a relatively minor role.

Liabilities are few—a small loan to pay off within the year, some wages owed to employees, and a couple thousand dollars to pay suppliers.

Annie’s is a single-member LLC—there are no shareholders, so her equity includes only her initial investment, retained earnings, and Annie’s draw($4,000).

Ratio analysis:

Current ratio: 22,000 / 7,000 = 3.14:1

Annie’s current ratio is very healthy. If necessary, her current assets could pay off her current liabilities more than three times over.

Quick ratio: 6,000 / 7,000 = 0.85:1

Her quick ratio isn’t looking so hot, though. Annie’s currently sitting just below 1:1, meaning she wouldn’t be able to quickly pay off debt.

Debt-to-equity ratio: 7,000 / 15,000 = 0.46:1

Annie’s debt-to-equity looks good. She’s got more than twice as much owner’s equity than she does outside liabilities, meaning she’s able to easily pay off all her external debt.

Final analysis:

Annie is able to cover all of her liabilities comfortably—until we take her equipment assets out of the picture. Most of her assets are sunk in equipment, rather than quick-to-cash assets. With this in mind, she might aim to grow her easily liquidated assets by keeping more cash on hand in the business checking account.

That being said, her owner’s equity is more than capable of covering her debt, so this problem shouldn’t be difficult to fix. It would be wise for Annie to take care of it before applying for loans or bringing on investors.

Example balance sheet analysis: Bill’s Book Barn LTD.

A lot of Bill’s assets are tied up in inventory—his large collection of books. The rest mostly consists of long-term investments and intangible assets. (Bill’s Book Barn is famous among collectors of rare fly-tying manuals; a business consultant valued his list of dedicated returning customers at $10,000.)

He doesn’t have a lot of liabilities compared to his assets, and all of them are short-term liabilities. Meaning, he’ll need to pay off that $17,000 within a year.

Finally, since Bill is incorporated, he has issued shares of his business to his brother Garth. Currently, Garth holds a $12,000 share in the business, a little shy of half its total equity.

Ratio analysis

Current ratio: 30,000 / 17,000 = 1.76:1

Since long-term investments and intangible assets are tough to liquidate, they’re not included in current assets—meaning Bill has $30,000 in assets he can more or less easily use to cover his liabilities. His ratio of 1.76:1 isn’t great—it doesn’t leave much wiggle room if he wants to pay off his liabilities. But it isn’t terrible, either—he’s just shy of a healthy 2:1 ratio.

Quick ratio: 7,000 / 17,000 = 0.41:1

Bill’s quick ratio is pretty dire—he’s well short of paying off his liabilities with cash and cash equivalents, leaving him in a bind if he needs to take care of that debt ASAP.

Debt-to-equity ratio: 17,000 / 15,000 = 1.13:1

Once we take into account his $13,000 owner’s draw, Bill’s owner’s equity comes to just $15,000, shy of his $17,000 in debt. Remember, an acceptable debt-to-equity ratio is 2:1. Bill is falling short of acceptable; if he had to pay off all his debts quickly, his equity wouldn’t cover it, and he’d need to dip into his company’s income. That makes his business unattractive to potential investors. Unless he changes course, Bill will have trouble getting financing for his business in the future.

Summary Analysis

Bill’s ratios don’t look great, but there’s hope. If he starts liquidating some of his long-term investments now, he can bump his current ratio up to 2:1, meaning he’d be in a healthy position to pay off liabilities with his current assets.

His quick ratio will take more work to improve. A lot of Bill’s assets are tied up in inventory. If he could convert some of that inventory to cash, he could improve his ability to pay of debt quickly in an emergency. He may want to take a look at his inventory, and see what he can liquidate. Maybe he’s got shelves full of books that have been gathering dust for years. If he can sell them off to another bookseller as a lot, maybe he can raise the $10,000 cash to become more financially stable.

Finally, unless he improves his debt-to-equity ratio, Bill’s brother Garth is the only person who will ever invest in his business. The situation could be improved considerably if Bill reduced his $13,000 owner’s draw. Unfortunately, he’s addicted to collecting extremely rare 18th century guides to bookkeeping. Until he can get his bibliophilia under control, his equity will continue to suffer.

Balance sheets can tell you a lot of information about your business, and help you plan strategically to make it more liquid, financially stable, and appealing to investors. But unless you use them in tandem with income statements and cash flow statements, you’re only getting part of the picture. Learn how they work together with our complete guide to financial statements .

Related Posts

Understanding Income Statements vs Balance Sheets

Understanding how income statements and balance sheets work together can help you plan your business's future growth.

How to Read the Bench Income Statement From Your Stripe Dashboard

We’ll take you step-by-step through the Bench income statement and how it describes the current financial state of your company.

A Primer on Accrued Expenses (6 Examples)

If you’ve received a good or service and plan to pay for it in the future, you have to record it in your books as an accrued expense. Here’s how to do it properly.

Join over 140,000 fellow entrepreneurs who receive expert advice for their small business finances

Get a regular dose of educational guides and resources curated from the experts at Bench to help you confidently make the right decisions to grow your business. No spam. Unsubscribe at any time.

- CRM Software

- Email Marketing Software

- Help Desk Software

- Human Resource Software

- Project Management Software

- Browse All Categories

- Accounting Firms

- Digital Marketing Agencies

- Advertising Agencies

- SEO Companies

- Web Design Companies

- Blog & Research

Capterra lists all providers across its website—not just those that pay us—so that users can make informed purchase decisions. Capterra is free for users. Software and service providers pay us for sponsored profiles to receive web traffic and sales opportunities. Sponsored profiles include a link-out icon that takes users to the provider’s website. Learn more.

Capterra carefully verified over 2 million reviews to bring you authentic software and services experiences from real users. Our human moderators verify that reviewers are real people and that reviews are authentic. They use leading tech to analyze text quality and to detect plagiarism and generative AI. Learn more.

Capterra’s researchers use a mix of verified reviews, independent research and objective methodologies to bring you selection and ranking information you can trust. While we may earn a referral fee when you visit a provider through our links or speak to an advisor, this has no influence on our research or methodology.

How To Prepare a Balance Sheet: A Step-by-Step Guide

Why should you create a balance sheet?

4 tasks to complete before preparing a balance sheet, use this guide to learn what goes into preparing an accurate balance sheet..

As an entrepreneur or a business owner, one of the biggest mistakes you can make is not taking the time to study your company’s financial statements. And worse still, not preparing them at all.

A balance sheet is among the most notable financial statements used to monitor the financial health of your business. For management, it informs internal decision-making, and for lenders and investors, it offers a quick look into your company's capability to make profits and pay back debt.

You can prepare a balance sheet on your own or hire accountants and bookkeepers to do it for you. Another way is to hand over the responsibility to an outside specialist firm by outsourcing the job. No matter which path you take, it’s important to understand how a balance sheet works as well as the basic steps to prepare it.

This article is for anyone who wants to understand how to prepare a balance sheet, which is often used by investors, creditors, and management. We explain why and how to create one as well as suggest technology tools to simplify your job.

A balance sheet summarizes your firm’s current financial worth by showing the value of what it owns (assets) minus what it owes (liabilities). It can be understood with a simple accounting equation:

Assets = Liabilities + Shareholders’ Equity

Preparing a balance is like creating a blown-up version of the above equation by vertically dividing the sheet into two parts with assets listed on the left, and claims of owners (equity) and liabilities are on the right. The two sides must always be equal.

The purpose of creating a balance sheet is to know the financial position of your business, particularly what it owns and what it owes by the end of an accounting period (usually after every 12 months). Therefore, a balance sheet is also called a position statement or a statement of financial position—it provides a snapshot of all assets and liabilities at a particular point in time.

Three ways using a balance sheet benefits your business:

It provides the basis for assessing risks and returns. By comparing your current assets against current liabilities, you can determine if you have enough capital to cover short-term debts (e.g., wages, lease payments) or if you need more to run everyday operations.

It’s instrumental in securing loans and investments. Most lenders and investors assess the balance sheet to see if your business can collect payments from clients, repay debts on time, and manage assets responsibly.

It shows the long-term sustainability of your business. By analyzing your balance sheet and finding out appropriate financial ratios from it, you can assess your business’s position in terms of profitability, productivity, and liquidity. You can also use these ratios to compare your performance against competitors’.

To create a balance sheet, you have to follow an order and prepare a few things first—like you would have to do for many other business processes.

1. Adjust entries in the general journal

Adjusting journal entries is necessary before preparing the four basic financial statements , including the balance sheet. It means updating your accounts at the end of an accounting period for items that are not recorded in your journal.

For instance, if you delivered goods worth $5,000 on the last day of the month but didn’t receive the amount until the next accounting period, then you’ll need to adjust your journal entry. Update your accounts by making such adjusting entries in the general journal.

What is a general journal?

A general journal is the first place where daily business transactions are recorded by date. Depending upon the practice followed in an organization, some may keep specialized journals such as a sales journal, cash receipts journal, and purchase journal to record specific types of transactions.

2. Post general journal transactions to the general ledger

After transactions are recorded and adjusted for in the general journal, they are transferred to appropriate sub-ledger accounts, such as sales, purchase, accounts receivable, inventory, and cash. This process is called posting.

While a general journal records business transactions on an everyday basis, general ledgers group these transactions by their accounts. The accounts are then aggregated to a general ledger at the end of the accounting period. The general ledger acts as a collection of all accounts and is used to prepare the balance sheet and the profit and loss statement.

3. Generate the final trial balance

Once you have adjusted journal entries and posted them in the general ledger, construct a final trial balance. Trial balance is a report that lists general ledger accounts and adds up their balances. Generating the trial balance report makes it much easier to check and locate any errors in the overall accounts.

The sum of all debits must always equal the sum of all credits in a trial balance report. If it doesn’t, it means there are errors you need to track down. You may have missed a transaction or calculated something incorrectly.

Use software for bookkeeping

Accurately recording financial data is a prerequisite for effective financial reporting. Indeed, you can still do your bookkeeping with pencil and paper. But, manual bookkeeping takes much longer and leaves space for human errors.

All accounting software tools generate trial balance as a standard report. You can streamline everyday bookkeeping tasks and ensure bookkeeping accuracy using accounting software .

4. Generate the income statement

An income statement is prepared before a balance sheet to calculate net income, which is the key to completing a balance sheet. Net income is the final amount mentioned in the bottom line of the income statement, showing the profit or loss to your business. Net income is added to the retained earnings accounts (income left after paying dividends to shareholders) listed under the equity section of the balance sheet.

Prepare an income statement by taking income and expense items (such as sales) from the trial balance and organizing them in a proper format.

Now that you understand the basics, let’s discuss (in the next section) the six steps to prepare a balance sheet.

Step #1: Determine a reporting date for the balance sheet

A balance sheet determines the financial position of your business at a particular point in time, not for a period. Thus, the header of a balance sheet always reads “as on a specific date” (e.g., as on Dec. 31, 2021).

A balance sheet is usually prepared at the end of a financial year (typically every 12 months on the last day of March or December), but it can be created at any or multiple points in time, say quarterly or half-yearly.

Step #2: Collect accounts that go on the balance sheet

From all the accounts mentioned in the general ledger and trial balance report, the balance sheet shows only the permanent accounts ( e.g., cash, fixed assets). Permanent accounts are those accounts whose balances are carried over to the next period.

Identify these accounts and note their balances. An example of permanent accounts or balance sheet accounts on a trial balance report is given below.

Illustration of balance sheet accounts in a trial balance report

Step #3: Calculate the total assets

The next step is to identify accounts from your trial balance that represent what you own—in other words, your assets such as cash and inventory. List them on the left to create the asset side of the balance sheet. You can classify asset accounts further into two types: current and noncurrent.

Current assets include assets that can be converted into cash as early as possible (typically within the next 12 months). Current asset accounts include cash, accounts receivable, and inventory.

Cash refers to both cash in hand and at the bank.

Accounts receivable refers to transactions for which money is yet to come from your customers—i.e., the amount you are owed.

Inventory is usually the biggest portion of current assets. On the balance sheet, it includes goods that are ready for sale as well as raw materials or half-done products.

Noncurrent assets include assets that cannot be converted into cash within the next 12 months. They are used to run daily business operations. Examples are plant/factory, machinery, furniture, and patents and copyrights (intangible assets).

List the values of each current and noncurrent asset component from the trial balance account, and add up the total current assets and the total noncurrent assets to calculate the grand total of assets.

Step #4: Calculate the total liabilities

Identify accounts from your trial balance that represent what you owe—in other words, your liabilities such as accounts payable (bills that you need to pay) and loans. List them on the right to create the liability side of the balance sheet. You can classify liability accounts further into two types: current and noncurrent liabilities.

Current liabilities are obligations or debts that are payable soon, usually within the next 12 months. They are also called short-term liabilities. Accounts payable and accrued payroll taxes are some commonly used current liability accounts.

Accounts payable includes bills or transactions for which money is yet to be paid to the suppliers or creditors. This is the amount you owe to others.

Accrued payroll taxes include the part of compensation your firm owes to employees and hasn’t been paid yet for the year, such as bonuses.

Noncurrent liabilities are obligations that will take more than the next 12 months to be repaid. They are also known as long-term liabilities. Examples include employees’ pensions.

List the values of each current and noncurrent liability component from the trial balance account, and add up the total current liabilities and the total noncurrent liabilities to calculate the grand total of liabilities.

Step #5: Arrange assets and liabilities in proper order

Once you have the assets and liabilities sections ready and sorted, arrange them in proper order. Assets should be arranged in the order of liquidity and liabilities in the order of discharge ability.

Arranging assets in the order of liquidity means putting assets that can be readily converted into cash at the top of the list and more permanent assets at the bottom. Similarly, arranging liabilities in the order of discharge ability means putting short-term obligations that are payable in the immediate future first and long-term and more permanent liabilities at the bottom.

Order of liquidity for assets | Order of discharge ability for liabilities |

|---|---|

Cash in hand Cash at bank Accounts receivable Vehicles Furniture and fittings Plant and machinery Land and building | Bank overdraft Accounts payable Creditors Loans Capital |

Step #6: Calculate shareholders’ equity

Mention shareholders’ equity on the right side of the balance sheet, right below the liabilities section. Shareholders’ equity, also known as the net worth of a company, shows the value of your business if it were to be liquidated or closed down.

It includes two types of investments: capital contributed by investors/owners and the earnings or losses accumulated in the business. The most common accounts listed under shareholders’ equity are common stock, preferred stock, treasury stock, and retained earnings.

Common and preferred stocks are the shares issued by a company. Common shares give voting rights to the owners, but in the event of a company being closed, common shareholders are paid back only after preferred shareholders.

Treasury stock refers to the shares repurchased from investors to protect the firm from a hostile takeover.

Retained earnings include earnings that are reinvested in the business. It’s calculated by adding net income to previous period’s retained earnings and deducting the amount paid to investors as a share of profits.

List the values of each shareholders’ equity component from the trial balance account, and add them up to calculate total owners’ liabilities. Next, calculate the total liabilities and shareholders’ equity by adding the final sum from step 4 and step 6.

Once this is done, you’ll have a complete balance sheet ready for you. Make sure the balance on the left side matches the balance on the right. If not, check your values again.

Illustration of a balance sheet with total assets matching total liabilities and owners’ equity

Prepared the balance sheet for your business? Check out how to analyze the numbers on your balance sheet to gain actionable insights into your financial health.

The integrity of a balance sheet is directly related to the information that goes into its preparation. Like most of your accounting tasks, accounting software can revamp recordkeeping and do much of the legwork while reducing errors. Use it to build a general ledger and trial balance with ease.

Doing key calculations and finding appropriate accounting ratios, such as working capital and debt-to-equity ratio, are key to analyzing your balance sheet. Financial reporting applications can help you interpret these ratios and understand the balance sheet.

Prepare a cover letter explaining the key points in the balance sheet when sending it to business leaders. Doing this will establish effective financial reporting practices that bring value to your business.

Thinking about hiring an accounting firm for help preparing your balance sheet? Browse our list of top accounting firms and learn more about their services in Capterra’s hiring guide .

Was this article helpful?

About the author s.

Amita Jain is a senior writer for Capterra, covering finance technology with a focus on expense management and accounting solutions for small-to-midsize businesses. After completing her master’s in policy studies from King’s College London, she began her career as a journalist in New Delhi, India, where she garnered first-hand knowledge of the startup space and the education sector. She spent nearly half a decade covering high-level events hosted by the United Nations and the Government of India. Her work has been featured in Gartner and Careers360, among other publications.

Amita’s research and writing for Capterra is informed by more than 130,000 authentic user reviews and over 30,000 interactions between Capterra software advisors and software buyers. Amita also regularly speaks to leaders in the finance and accounting space so she can provide the most up-to-date and helpful information to small and midsize businesses purchasing software or services.

When she’s not contemplating tech solutions for SMBs, Amita finds her zen in swimming, doodling, and indulging in animated sitcoms and science fiction.

Rina is a senior editor at Capterra. She has close to a decade of experience creating and editing content, especially for the IT, software, and finance domains. Passionate about minimalist storytelling, she prioritizes breaking down complex industry jargon into engaging stories accessible to all readers.

Rina holds a postgraduate degree in mass communication and journalism and a bachelor's degree in English literature. She started her career as a features writer for The Times of India, India’s premier English daily newspaper. Outside of work, she’s a doting mother to her dog daughter Puppy, a budding resin artist, and a proponent of financial literacy for women.

RELATED READING

Business Plan Balance Sheet: Everything You Need to Know

Preparing a business plan balance sheet is an important part of starting your own business. 3 min read updated on February 01, 2023

Preparing a business plan balance sheet is an important part of starting your own business. The balance sheet serves as one of three crucial parts of the company's financials along with cash flow and the income statement. The basics of the balance sheet include a few straightforward parts:

- Company assets.

- Liabilities.

- Owner's equity.

The balance sheet will also include income and spending that isn't represented in the profit and loss statement. For example, it will show loan repayments and the purchase of new assets. Additionally, the money that is taken in as a new loan will not show up on the P & L either.

Accounts receivable, or the money you are waiting to receive from your customers, will show up as an asset on your balance sheet and as it is not yet reported as income on your P & L statement. A balance sheet is your business's representation of why your profits are not yet considered cash. It creates the broad financial picture of your business while the profit and loss statement will show the company's financial performance over a set length of time.

A balance sheet always has to balance. It will have assets on one side and liabilities and equity on the other. The basic formula that a balance sheet follows is Assets = Liabilities + Equity. In the end, it is the balance sheet that will show a company's net worth. To determine net worth at any given time, all you need to do is subtract the liabilities from the assets.

Balance sheets are used for planning and not accounting which is one of the principles of lean business planning. To get a useful cash flow projection, you will need to summarize the aggregate of the rows on the balance sheet. It is always important to look at a balance sheet as a tool to forecast your cash.

Components of a Balance Sheet

Just as one business will differ from another, so will the assets and liabilities of the business. Even though the titles will vary, the equation and goal remains the same. You will need to have your business assets equal your liabilities and equity .

The assets on your balance sheet will often be in order from the top to the bottom with how easy they can be converted to cash. This is called liquidity . Your most liquid assets will be on top and your least liquid on the bottom. Typically assets will be listed as follows:

- Cash — This is money currently on hands such as in checking and savings accounts. It can also include money market accounts that can be converted to cash quickly.

- Accounts Receivable — This represents money that is owed to you but has not actually been received yet. This is often credit that is extended to customers through invoicing.

- Inventory — This includes all the finished goods and materials that are ready at your place of business but has yet to be sold.

- Current Assets — These are assets that can be considered able to be converted into cash within a year or less. This includes all your cash, accounts receivable, and inventory which will all be grouped together as current assets.

- Long-Term Assets — These are fixed assets that have a long-standing value such as land and equipment. They cannot be converted to cash as quickly.

- Accumulated Depreciation — This is the value that your assets will be reduced over time due to depreciation.

- Long-Term Assets — This is the total of long-term assets plus depreciation.

Liabilities

Liabilities will be ordered for time it would take to pay them off, with current liabilities needing to be paid in a year or less and long-term liabilities longer than a year.

- Accounts Payable — This is the amount of money that your business will owe to vendors or for regular bills.

- Sales Tax Payable — If your sales tax is not paid right away, it will accrue in this account until payment is made.

- Short-Term Debt — This is usually short-term loans that will be repaid in less than a year.

- Total Current Liabilities — The total amount of debt that the business will need to pay back in a year.

- Long-Term Debt — This amount includes the financial responsibilities that will take more than a year to pay back.

If you need help with a business plan balance sheet, you can post your legal need on UpCounsel's marketplace. UpCounsel accepts only the top 5 percent of lawyers to its site. Lawyers on UpCounsel come from law schools such as Harvard Law and Yale Law and average 14 years of legal experience, including work with or on behalf of companies like Google, Menlo Ventures, and Airbnb.

Hire the top business lawyers and save up to 60% on legal fees

Content Approved by UpCounsel

- S Corp Balance Sheet

- How to Prepare Annual Report of a Company

- Are Patents Intangible Assets

- How to Evaluate a Company for Investment?

- What Is Liability Business - Everything You Need to Know

- Common Stock Asset or Liability

- Financial Plan Sample For Small Business

- How to Check Up on a Business

- Cash on Hand

- Personal Assets

- Credit cards

- View all credit cards

- Banking guide

- Loans guide

- Insurance guide

- Personal finance

- View all personal finance

- Small business

- Small business guide

- View all taxes

You’re our first priority. Every time.

We believe everyone should be able to make financial decisions with confidence. And while our site doesn’t feature every company or financial product available on the market, we’re proud that the guidance we offer, the information we provide and the tools we create are objective, independent, straightforward — and free.

So how do we make money? Our partners compensate us. This may influence which products we review and write about (and where those products appear on the site), but it in no way affects our recommendations or advice, which are grounded in thousands of hours of research. Our partners cannot pay us to guarantee favorable reviews of their products or services. Here is a list of our partners .

Balance Sheet: Definition, Uses and How to Create One

Billie Anne is a freelance writer who has also been a bookkeeper since before the turn of the century. She is a QuickBooks Online ProAdvisor, LivePlan Expert Advisor, FreshBooks Certified Partner and a Mastery Level Certified Profit First Professional. She is also a guide for the Profit First Professionals organization. In 2012, she started Pocket Protector Bookkeeping, a virtual bookkeeping and managerial accounting service for small businesses.

Rick VanderKnyff leads the team responsible for expanding NerdWallet content to additional topics within personal finance. Previously, he has worked as a channel manager at MSN.com, as a web manager at University of California San Diego, and as a copy editor and staff writer at the Los Angeles Times. He holds a Bachelor of Arts in communications and a Master of Arts in anthropology.

Many or all of the products featured here are from our partners who compensate us. This influences which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money .

The balance sheet summarizes your business's financial status as of a certain date. It follows the accounting equation: Assets = Liabilities + Owner's equity. In non-accounting terms, the balance sheet tells you what your business owns (assets), what it owes (liabilities), and what the owner's stake in the business is (equity).

If you think of your financial statements as the story of your business, then the balance sheet serves as the CliffsNotes version of that story. Every transaction in your business impacts the balance sheet in some way.

» MORE: Nine basic accounting concepts every business owner should know

advertisement

QuickBooks Online

What does a balance sheet include?

The balance sheet includes three broad categories of information:

Liabilities.

Owner's equity.

Assets are the things your business owns. Most balance sheets break down assets into two subcategories.

Current assets are cash, cash equivalents, and things that can be easily converted into cash within the next 12 months. Your bank accounts, petty cash, accounts receivable (amounts customers owe to you), and inventory are all examples of current assets.

Fixed assets are things your business owns that aren't likely to be converted into cash (sold) within a 12-month period. This includes land, buildings, heavy equipment, vehicles, and long-term loans to customers. Some businesses also have intangible assets, like trademarks and patents, listed under fixed assets on their balance sheets.

Liabilities

Liabilities are amounts your business owes to others. As with assets, most balance sheets break down liabilities into two subcategories.

Current liabilities are amounts you are likely to pay within the next 12 months. This includes amounts due to vendors for utilities and inventory (accounts payable), credit card balances, sales tax and payroll taxes you've collected but not yet submitted to the government, and the portion of loan balances due within the next 12 months. In addition, if you have a line of credit for your business, that will usually be listed as a current liability on your balance sheet.

Long-term liabilities are amounts due in the future beyond the next 12 months. This would include the mortgage on your building, vehicle loans, and long-term leases.

Equity balances out the difference between assets and liabilities. It is your stake in the business. You can also look at equity as the amount the business owes to you.

Equity consists of:

Contributions you have made to the business (startup cash you invested, additional paid-in capital, etc.)

Retained earnings (amounts you have left in the business over time.)

Capital and preferred stock, if your business has other shareholders.

The current year's net income (from your profit and loss statement).

Let's look back at the accounting equation the balance sheet follows:

Assets = Liabilities + Equity.

Another way to look at this equation is

Assets - Liabilities = Equity.

In other words, equity is what is left for the business owner after all the liabilities are paid from the business's assets. Equity will be negative if a business's liabilities exceed its assets. This means the business owner might have to use their own money to pay the business's debts if it closes immediately. Negative equity can also negatively impact the selling price of the business.

» MORE: Best accounting software for small businesses

What does a balance sheet exclude?

The balance sheet excludes detailed information about the business's income and expenses. Instead, this detail is included in the business's profit and loss statement.

But remember: Every transaction in your business impacts the balance sheet in some way. Your business's income and expenses are summarized on the balance sheet as Net Income under the Equity section.

Looking for accounting software?

See our overall favorites, or choose a specific type of software to find the best options for you.

on NerdWallet's secure site

How can you make a balance sheet?

If your business is new and simple, you can create a manual balance sheet using the accounting formula. First, list your current bank account balances (assets), subtract any loans or amounts due to others (liabilities), and what is left is your equity in the business.

However, most businesses must rely on their accounting software to create an accurate balance sheet. The balance sheet is a standard report in all double-entry bookkeeping software.

To create a balance sheet in your accounting software, go to the reports section and look for financial reports. Since it is a common financial statement, the balance sheet should appear near the top of the list, often right after the profit and loss (or income) statement.

Some accounting software prompts you to enter a date range for the balance sheet report. This isn't wrong, per se, but it can be confusing. Unlike the profit and loss statement, which only shows information for a certain period, the balance sheet shows information as of a specific date. And that information includes a financial summary of your business from its start through the "as of" date on the balance sheet.

The purpose of the balance sheet

Before the advent of double-entry bookkeeping software, the balance sheet ensured the accuracy of a business's bookkeeping. For example, if the balance sheet was out of balance — meaning assets weren't equal to the combined value of liabilities and equity — then that indicated an error in the books.

Today's accounting software won't let you post an unbalanced transaction, so finding an out-of-balance balance sheet is rare. In fact, an unbalanced balance sheet usually indicates a technical problem inside the software. But that doesn't mean the balance sheet is obsolete. On the contrary, the balance sheet is an essential tool to help you — and potential investors — analyze your company's health at a glance and make sound business decisions.

» MORE: Chart of accounts: Definition, guide and examples

How the balance sheet can help you make business decisions

You can quickly analyze your business's financial health with a glance at the balance sheet. If equity is negative — meaning liabilities are greater than assets — that could indicate your business is in financial trouble. It would be best to meet with an accountant to discuss ways to increase your assets or decrease your liabilities, so your stake in the business is no longer negative.

If you want to go beyond a glance, you can quickly calculate three critical metrics from your business's balance sheet.

Current ratio

The current ratio measures your business's ability to pay your current liabilities. The formula is:

Current assets / Current liabilities = Current ratio

The current ratio tells you how many times your business can pay its current liabilities from the cash on hand. Anything less than 1 indicates your business does not have enough cash or cash equivalents to pay amounts due in the next 12 months.

Quick ratio

The quick ratio formula is:

(Cash & cash equivalents + Short-term investments + Accounts receivable) / Current liabilities = Quick ratio

The quick ratio is a measure of liquidity and is often the same as the current ratio.

Debt to equity ratio

The debt-to-equity ratio tells you how leveraged your business is or how much of your business is financed with debt. The formula is:

Total liabilities / Total equity = Debt-to-equity ratio

Notice that now we're looking at total liabilities — including long-term debt. A good debt-to-equity ratio is between 1 and 1.5. Anything higher than that can indicate your business is highly leveraged. This could make it harder to get financing at a favorable rate.

Other considerations

These ratios are good quick measurements of your business's performance in certain critical areas, but they don't tell the whole story. To make the best decisions for your business, you should review the balance sheet alongside the profit and loss statement and statement of cash flows. Enlisting the help of an accountant who knows your business and your industry is also key to using your balance sheet to make business decisions.

| Product | Starting at | Promotion | Learn more |

|---|---|---|---|

| QuickBooks Online 5.0 on QuickBooks' website | $30/month | 50% off | on QuickBooks' website |

| Xero 5.0 on Xero's website | $15/month | 30-day free trial | on Xero's website |

| Zoho Books 4.5 on Zoho Books' website | $0 | 14-day free trial | on Zoho Books' website |

| FreshBooks 4.5 on FreshBooks' website | $19/month | 30-day free trial | on FreshBooks' website |

- Search Search Please fill out this field.

- Building Your Business

- Becoming an Owner

- Business Plans

How to Write the Financial Section of a Business Plan

Susan Ward wrote about small businesses for The Balance for 18 years. She has run an IT consulting firm and designed and presented courses on how to promote small businesses.

:max_bytes(150000):strip_icc():format(webp)/SusanWardLaptop2crop1-57aa62eb5f9b58974a12bac9.jpg "balance sheet for a business plan")

Taking Stock of Expenses

The income statement, the cash flow projection, the balance sheet.

The financial section of your business plan determines whether or not your business idea is viable and will be the focus of any investors who may be attracted to your business idea. The financial section is composed of four financial statements: the income statement, the cash flow projection, the balance sheet, and the statement of shareholders' equity. It also should include a brief explanation and analysis of these four statements.

Think of your business expenses as two cost categories: your start-up expenses and your operating expenses. All the costs of getting your business up and running should be considered start-up expenses. These may include:

- Business registration fees

- Business licensing and permits

- Starting inventory

- Rent deposits

- Down payments on a property

- Down payments on equipment

- Utility setup fees

Your own list will expand as soon as you start to itemize them.

Operating expenses are the costs of keeping your business running . Think of these as your monthly expenses. Your list of operating expenses may include:

- Salaries (including your own)

- Rent or mortgage payments

- Telecommunication expenses

- Raw materials

- Distribution

- Loan payments

- Office supplies

- Maintenance

Once you have listed all of your operating expenses, the total will reflect the monthly cost of operating your business. Multiply this number by six, and you have a six-month estimate of your operating expenses. Adding this amount to your total startup expenses list, and you have a ballpark figure for your complete start-up costs.

Now you can begin to put together your financial statements for your business plan starting with the income statement.

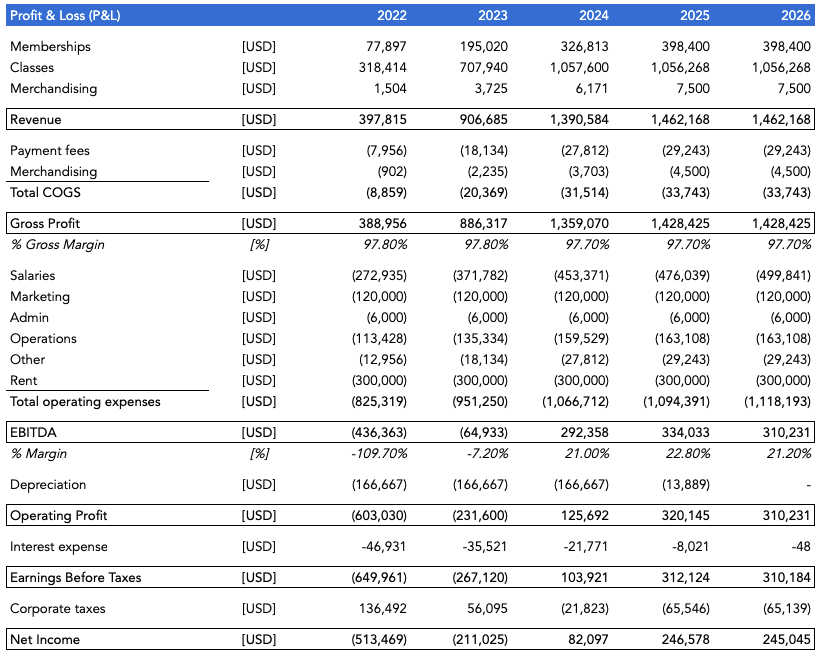

The income statement shows your revenues, expenses, and profit for a particular period—a snapshot of your business that shows whether or not your business is profitable. Subtract expenses from your revenue to determine your profit or loss.

While established businesses normally produce an income statement each fiscal quarter or once each fiscal year, for the purposes of the business plan, an income statement should be generated monthly for the first year.

Not all of the categories in this income statement will apply to your business. Eliminate those that do not apply, and add categories where necessary to adapt this template to your business.

If you have a product-based business, the revenue section of the income statement will look different. Revenue will be called sales, and you should account for any inventory.

The cash flow projection shows how cash is expected to flow in and out of your business. It is an important tool for cash flow management because it indicates when your expenditures are too high or if you might need a short-term investment to deal with a cash flow surplus. As part of your business plan, the cash flow projection will show how much capital investment your business idea needs.

For investors, the cash flow projection shows whether your business is a good credit risk and if there is enough cash on hand to make your business a good candidate for a line of credit, a short-term loan , or a longer-term investment. You should include cash flow projections for each month over one year in the financial section of your business plan.

Do not confuse the cash flow projection with the cash flow statement. The cash flow statement shows the flow of cash in and out of your business. In other words, it describes the cash flow that has occurred in the past. The cash flow projection shows the cash that is anticipated to be generated or expended over a chosen period in the future.

There are three parts to the cash flow projection:

- Cash revenues: Enter your estimated sales figures for each month. Only enter the sales that are collectible in cash during each month you are detailing.

- Cash disbursements: Take the various expense categories from your ledger and list the cash expenditures you actually expect to pay for each month.

- Reconciliation of cash revenues to cash disbursements: This section shows an opening balance, which is the carryover from the previous month's operations. The current month's revenues are added to this balance, the current month's disbursements are subtracted, and the adjusted cash flow balance is carried over to the next month.

The balance sheet reports your business's net worth at a particular point in time. It summarizes all the financial data about your business in three categories:

- Assets : Tangible objects of financial value that are owned by the company.

- Liabilities: Debt owed to a creditor of the company.

- Equity: The net difference when the total liabilities are subtracted from the total assets.

The relationship between these elements of financial data is expressed with the equation: Assets = Liabilities + Equity .

For your business plan , you should create a pro forma balance sheet that summarizes the information in the income statement and cash flow projections. A business typically prepares a balance sheet once a year.

Once your balance sheet is complete, write a brief analysis for each of the three financial statements. The analysis should be short with highlights rather than in-depth analysis. The financial statements themselves should be placed in your business plan's appendices.

- Search Search Please fill out this field.

What Is a Balance Sheet?

How balance sheets work, special considerations.

- Why Is It Important?

- Limitations

- Balance Sheet FAQs

- Corporate Finance

- Financial statements: Balance, income, cash flow, and equity

Balance Sheet: Explanation, Components, and Examples

What you need to know about these financial statements

:max_bytes(150000):strip_icc():format(webp)/jason_mugshot__jason_fernando-5bfc261946e0fb00260a1cea.jpg "balance sheet for a business plan")

- Valuing a Company: Business Valuation Defined With 6 Methods

- Valuation Analysis

- Financial Statements

- Balance Sheet CURRENT ARTICLE

- Cash Flow Statement

- 6 Basic Financial Ratios

- 5 Must-Have Metrics for Value Investors

- Earnings Per Share (EPS)

- Price-to-Earnings Ratio (P/E Ratio)

- Price-To-Book Ratio (P/B Ratio)

- Price/Earnings-to-Growth (PEG Ratio)

- Fundamental Analysis

- Absolute Value

- Relative Valuation

- Intrinsic Value of a Stock

- Intrinsic Value vs. Current Market Value

- Equity Valuation: The Comparables Approach