March 21 Deadline for Servicers to Assign to HUD Certain Reverse Mortgages to Protect Surviving Spouses

HUD created a March 21st deadline for reverse mortgage servicers to assign the reverse mortgage to HUD without financial penalty in order to protect certain surviving non-borrower spouses from foreclosure. This article explains the meaning of the deadline and what actions non-borrowing surviving spouses should take so that they can remain in their homes. For a certain category of surviving spouses, it is important to act before March 21 .

The Mortgagee Optional Election Option Protecting Non-Borrowing Spouses

Administered by HUD, the nation’s major reverse mortgage program is called the Home Equity Conversion Mortgage (HECM) program. HECM mortgages are made by private lenders, but under rules set out by HUD.

HECM reverse mortgage loans generally must be paid off when the last borrower dies, sells, or permanently relocates from the home. Since August 4, 2014, the HECM loan documents explicitly allow for a non-borrowing spouse to remain in the home after the borrower’s death, until the non-borrowing spouse either dies or moves out.

For HECMs made before August 4, 2014, non-borrowing spouses living in the home after the death of the borrower can end up in foreclosure unless they take action. HUD created the Mortgagee Optional Election (MOE) in 2015 to allow non-borrowing spouses with pre-August 2014 loans to remain at home after the borrower dies if they meet the eligibility criteria and continue to fulfill the terms and conditions of the loan. However, many non-borrowing spouses had been blocked from accessing the MOE program due to strict deadlines and a confusingly worded requirement to establish “good and marketable title or a legal right to remain in the home.”

HUD in 2019 Gives Non-Borrowing Spouses a Better Chance at Protection

HUD issued revised guidelines on September 23, 2019, announced in Mortgagee Letter 2019-15 , indicating that non-borrowing spouses no longer have to provide proof of marketable title or a legal right to remain in the home in order to be eligible for the MOE program. Moreover, there is no hard deadline for servicers to elect the MOE. The new policy relaxes program deadlines and also requires servicers to notify borrowers about the existence of the option and request the names of any non-borrowing spouse living in the home who may potentially qualify for the option. Borrowers will receive the notice and form along with the annual occupancy certification.

Timing and Process to Avoid Foreclosure

The MOE is still discretionary with the lender. In order to avoid being financially penalized by HUD, the lender must either initiate foreclosure or assign the loan to HUD through the MOE process within 180 days of the borrower’s death or the issuance of the mortgagee letter, whichever is later. For non-borrowing spouses who were previously blocked from the program due to missing a deadline, and whose spouses died months or years ago, the new Mortgagee Letter provides a new window of time in which lenders can elect the MOE without any financial penalty.

This window extends until March 21, 2020. Even after that date, lenders can elect the MOE, but might face interest curtailment due to their delay. Lenders may choose to make the MOE election even after starting the foreclosure process.

The surviving non-borrowing spouse still must establish her eligibility under the program’s guidelines. Eligible non-borrowing spouses include those who were married to the borrower at the time of loan closing (or engaged in a committed relationship akin to marriage); live in the home as a principal residence; and have a loan that is not due and payable for other reasons. If property charges are in arrears, even if the borrower was enrolled in a repayment plan prior to the death, the non-borrowing spouse must bring those charges current before the lender can assign the loan to HUD.

If the non-borrowing spouse qualifies for the MOE, the due and payable status on the loan will be deferred and the loan will not be subject to foreclosure until the spouse moves out of the home, dies, or fails to meet the terms and conditions of the loan, including paying the property charges. Though the spouse is required to meet the financial obligations of the loan (i.e., payment of ongoing property charges, home maintenance) she will not receive any proceeds from the HECM. The non-borrowing spouse must certify annually that these conditions for deferral continue to be met.

Importance of the March 21st Deadline

Non-borrowing spouses who have not been contacted and are still in the home despite the death of a borrower-spouse prior to September 23, 2019 should reach out to the mortgage company right away. There is a short window—up until March 21, 2020—during which the lender can put these older loans into the MOE program without financial penalty.

For More Information

NCLC has produced a fact sheet for non-borrowing spouses— Are You a Reverse Mortgage Non-Borrowing Spouse? Tips to Help You Remain in Your Home —which is available to download and distribute. The fact sheet has information on obtaining assistance with the process.

Also an important source of information is HUD’s guidance found in Mortgagee Letter 2019-15 (Sept. 23, 2019).

National Consumer Law Center, Home Foreclosures Chapter 14 is a detailed treatment of all foreclosure issues relating to reverse mortgages. See in particular § 14.3.3.3 and 14.3.3.4 .

Also of relevance is NCLC’s Mortgage Lending Chapter 9 , concerning the origination of reverse mortgages. See in particular §§ 9.3 and 9.7.2 . See also NCLCs Mortgage Servicing and Loan Modifications .

Meet the author

Sarah Bolling Mancini is Co-Director of Advocacy focusing on foreclosures, mortgage lending, and credit reporting issues. Sarah’s work centers on the racial justice issues surrounding homeownership, including access to sustainable mortgages and addressing the risks posed by land contracts, lease-options, home equity theft, heirs property, and property tax foreclosure. Sarah previously worked in the Home Defense Program of Atlanta Legal Aid, and has represented homeowners in litigation in state, federal district, and bankruptcy courts. She also clerked for the Honorable Amy Totenberg, U.S. District Court for the Northern District of Georgia. Sarah is a member of the Georgia Bar. She received her B.A. in public policy from Princeton University and her J.D. from Harvard Law School.

Related Publications

Home foreclosures.

Mortgage Lending

Related Articles

- Three Important New Protections Preventing Home Foreclosures

- Supreme Court Stops Equity Theft in Property Tax Foreclosures

- Homeowner Tactics to Overcome Problems with Tangled Titles

- HUD Removes Significant Obstacle to FHA Mortgage Loan Modifications

- LIBOR’s Death Will Soon Impact $1.4 Trillion in Consumer Contracts

Free First Chapters

The first chapter of each consumer law treatise is available for free in NCLC's Digital Library.

Click any NCLC title below to start reading now:

Debtor Rights

Fair Debt Collection Consumer Bankruptcy Law and Practice Student Loan Law Repossessions Access to Utility Service

Mortgages & Foreclosures

Mortgage Lending Mortgage Servicing and Loan Modifications Home Foreclosures

Deception & Warranties

Unfair and Deceptive Acts and Practices Federal Deception Law Automobile Fraud Consumer Warranty Law

Credit & Banking

Fair Credit Reporting Truth in Lending Consumer Credit Regulation Credit Discrimination Consumer Banking and Payments Law

Consumer Litigation

Collection Actions Consumer Class Actions Consumer Arbitration Agreements

- Personal Finance Financial Advisors Credit Cards Taxes Retirement

- Insurance Auto Vision Life Dental Health Medicare Home Life Business Pet

- Investing Stocks Options ETFs Mutual Funds Futures IPOs Bonds Index Funds Forex Prop Trading

- Alternative investing Real Estate Startups Collectables

- Mortgage Rates Calculator Reviews Purchase Refinance Self-Employed

- Cryptocurrency Exchanges Price Action Apps Earn Crypto Wallets

What Disqualifies You From Getting a Reverse Mortgage?

- You might be disqualified from getting a reverse mortgage if you don’t meet age requirements, are behind on other loans and payments, or don’t have enough equity in the home.

- Homes must meet the Department of Housing and Urban Development (HUD) and Federal Housing Administration (FHA) requirements while also serving as your primary residence or you might be denied a reverse mortgage.

- Applicants with poor credit, insufficient income to care for the home and pay property taxes or who have not completed a counseling session will often receive a denial.

If money is tight and you’re looking for options for added income, you might start wondering what disqualifies you from getting a reverse mortgage. You’ll need to meet several criteria or your application will be denied. Those criteria include being age 62 or older, having at least 50% equity in your home, and having enough income or assets to pay the property taxes and homeowners insurance. Let’s dive deeper into items that could disqualify you from getting a reverse mortgage and the alternatives available in case you are disqualified.

Reasons You May Be Disqualified From Getting a Reverse Mortgage

Under the age of 62, lack of complete ownership of the property.

- Your Home Is Not Your Primary Residence

Bad Credit History

- Too Little Equity

Property Is in Poor Condition

Failing to meet financial assessment requirements, behind on property taxes or homeowners insurance.

- Delinquent Federal Debts

You Have Yet to Finish a Counseling Session

- What if You Don't Qualify for a Reverse Mortgage?

Cash-Out Refinancing

- Home Equity Loan

Home Equity Line of Credit (HELOC)

Review requirements before applying for a reverse mortgage.

- Frequently Asked Questions

As reverse mortgages have grown in popularity, the qualification criteria have tightened somewhat. In 2015, FHA modified the rules, allowing lenders to complete a full financial assessment before granting funds to the borrower. That financial assessment has made it more challenging to qualify for the loan because the approvals are more strict. Review these reasons you might be disqualified from getting a reverse mortgage .

Borrowers who are less than 62 years of age will not qualify for traditional reverse mortgage products, though some banks have proprietary products that can help. The loan is designed to help supplement income for retirees while allowing them to stay in their homes that they know and are comfortable in. So if you haven’t reached age 62 yet, a home equity line of credit might be a better fit.

If your home does not meet the eligibility requirements, you can be denied the loan. You’ll need to own a single-family home, a multiunit home where you occupy one unit, a condo project that meets HUD requirements or FHA requirements, or a manufactured home that meets FHA requirements. If you don’t have complete ownership of the property, such as in the case of a co-applicant not included on the reverse mortgage application, your application will be denied.

Your Home Is Not Your Primary Residence

To pull equity from the home, it must be your primary residence. This means that you can’t apply for a reverse mortgage on a vacation home or a property where you only spend a small percentage of the year. You must live there the majority of the year to qualify for a reverse mortgage .

During the financial assessment, the lender will evaluate your credit report and look at how you’ve paid your debts previously. If you have missed payments and delinquent debts, you might receive a loan denial. Or if your debts consume too much of your income, the lender might find that you don’t have sufficient funds to complete the upkeep of the house and deny you the loan.

Too Little Equity

You can’t have loans on the home that exceed 50% of its value. In that case, you wouldn’t have enough equity to pull from the home for a reverse mortgage. Evaluate your home’s value and what you still owe on the home to calculate the equity you’ve built in it.

You must maintain your home to qualify for a reverse mortgage. During the application process, the lender will complete an appraisal to evaluate the home’s fair market value. They’ll be looking at the roof, HVAC, electrical, plumbing, windows and more. They want to know that the home is sound and the roof won’t leak and destroy everything or that a plumbing leak won’t lead to massive repairs that reduce the value of the home that is the collateral for your reverse mortgage loan.

If you are denied a reverse mortgage due to an area of the home being faulty, you can fix it up and apply again to prove that the home meets HUD requirements for health and safety.

Part of the reverse mortgage application process is completing a financial assessment with the lender. The lender will evaluate your income and assets to evaluate your ability to keep up with home maintenance, property taxes and homeowners insurance.

If you have inadequate income from your job, Social Security, 401(k) disbursements, pensions, rental income, investments or other sources, you won’t receive approval for the loan.

If you have delinquent property taxes, the lender might not grant you the loan. While you could use the loan to get current on your taxes, it signals to the lender that you don’t have sufficient funds to cover the taxes on an ongoing basis, which could lead to foreclosure. Staying current with homeowners insurance also protects the lender’s collateral for the loan in case anything serious happens to it, which is why they want to see that you’re making your premium payments.

Delinquent Federal Debts

You won’t qualify for a reverse mortgage if you are behind on payments for federal loans, such as federal student loans or income taxes. Proving that you’ll use the reverse mortgage proceeds to pay off these debts might still allow you to qualify for the loan.

All reverse mortgage borrowers must complete a counseling session with a HUD-approved counselor. During this session, you’ll learn the pros and cons of reverse mortgages and more about how they work. That way, you know your disbursement options and alternative loans that might be a better fit for your situation. Failing to complete the counseling session could be a reason you receive a denial from your application.

What if You Don’t Qualify for a Reverse Mortgage?

If you don’t qualify for a reverse mortgage with your first application, you have a few options. The first option is to wait. Giving it time until both applicants are age 62 or older or until you can get current on tax payments and homeowners insurance and fix up the house if the assessment shows it needs major repairs can all lead to approval later.

In the case of bad credit, spend some time working on your credit, either on your own or with a credit repair service. Work toward building more equity in the home by paying down your mortgage if you can.

Another option is to downsize your home. This allows you to reduce your monthly payments related to maintenance, energy, insurance and property taxes and might even mean you no longer have a mortgage payment. While letting go of your home might be disappointing, a downsize can help you purchase a property that is easier to maintain long-term and ensure you keep the equity you’ve built up in your home to pass to your heirs or ensure you can live there throughout retirement.

If waiting or downsizing are not of interest to you, consider one of these reverse mortgage alternatives.

Another way of accessing your home’s equity is through a cash-out refinancing. In this case, you’ll be taking on a new mortgage that is larger than your current one. For example, if you own a $500,000 home and currently owe $80,000 on it, you can increase the mortgage loan to $400,000. In this scenario, you would receive $320,000 at closing.

The catch with this is that you’ll need to be able to make the ongoing mortgage payments on the larger loan. Additionally, you’ll be subject to today’s mortgage terms, which might mean a higher interest rate than what you were paying.

Home Equity Loan

You can get a lump sum from your home’s equity with a home-equity loan. You’ll essentially be taking out a second mortgage on the home and using the home as the collateral. These loans often have a fixed interest rate with a fixed payment you’ll need to make each month. These loans often have a 30-year term.

When you fail to get a reverse mortgage, you might consider a home equity line of credit. The line of credit is determined using a portion of your home’s equity up to 85% less any outstanding loans on the home. During the draw period, which is often 10 years, you’ll only pay interest on the loan. At the end of the 10 years, you’ll start repaying the loan with principal and interest. These loans come with variable rates, which can be challenging when you’re on a fixed income during retirement.

Before applying for a reverse mortgage, review the lending requirements so you don’t get any surprises at the end of the application process. Make sure your affairs are in order before completing your application for best results.

Frequently Asked Questions

How hard is it to get a reverse mortgage.

As long as you meet the eligibility requirements, it is not hard to get a reverse mortgage.

Is getting a reverse mortgage a good idea?

A reverse mortgage can help you make ends meet during retirement and stay in your home. But you should only use it once you’ve exhausted other avenues, such as downsizing.

Who should not get a reverse mortgage?

You should get a reverse mortgage if you have adequate income to meet your home maintenance needs as well as property taxes and homeowners insurance. If you just need a little extra each month toward spending, a reverse mortgage can keep you in your home while supplying the income you need.

Get Ready for Take Off

Rocket Mortgage ® is an online mortgage experience developed by the firm formerly known as Quicken Loans®, America’s largest mortgage lender. Rocket Mortgage® makes it easy to get a mortgage — you just tell the company about yourself, your home, your finances and Rocket Mortgage® gives you real interest rates and numbers. You can use Rocket Mortgage® to get approved, ask questions about your mortgage, manage your payments and more.

You can work at your own pace and someone is always there to answer your questions — 24 hours a day, 7 days a week. Want a fast, convenient way to get a mortgage? Give Rocket Mortgage® a try .

About Rebekah Brately

Rebekah Brately is an investment writer passionate about helping people learn more about how to grow their wealth. She has more than 12 years of writing experience, focused on technology, travel, family and finance. Her work has been published in Benzinga, Hearst Bay Area, FreightWaves and Dallas Observer publications.

Reverse Mortgages Have 2 Notes and 2 Deeds of Trust

When it comes to signing final reverse mortgage loan documents, borrowers are often concerned when the notary presents them with two Deeds of Trust (or mortgages, depending on the location of the property) and a First and Second Note. To further complicate it, the Deed of Trust shows an amount much higher than anticipated and what was agreed upon. The concern over these items has caused several borrowers not to sign their final loan documents, which is why we strive to educate our borrowers prior to the final signing in order to prevent possible confusion.

The quick answer to why reverse mortgage loans have 2 Deeds of Trust and 2 Notes is that the first deed of trust secures the lender’s position and HUD assumes the second position because HUD is insuring that the homeowner will continue to receive loan payments in the event that the lender becomes incapable of making said payments.

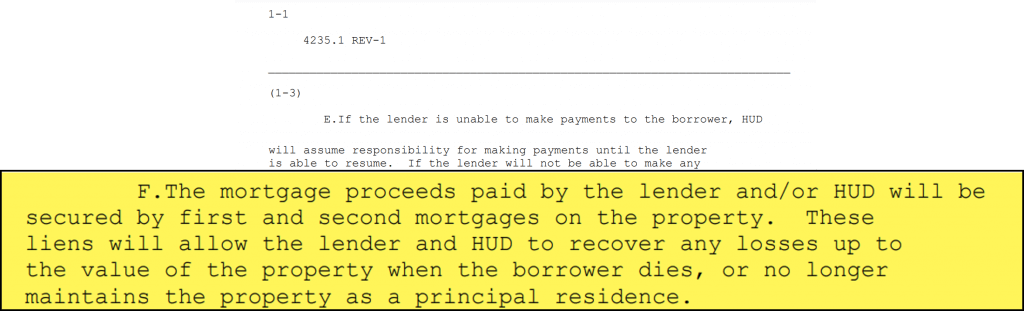

Going a little deeper into the explanation, the following quotes are direct from HUD Handbook 4235.1 REV 1. They discuss that every HECM reverse mortgage, fixed or adjustable, shall have a first and second Mortgage and Note. The borrower must only be presented with a copy of the first Note during the application process, but the existence and relationship of the second Note must be fully explained.

“A. Mortgage and note. The lender must provide a copy of the first mortgage and the appropriate first note (fixed or adjustable rate) for review by the borrower during the application process (see Paragraph 4-7), but not later than when the borrower signs the URLA. B. Second mortgage and note. The lender must complete a second mortgage and second note (fixed or adjustable rate) to secure any payments made by HUD to the borrower . A copy of the second mortgage and second note need not be provided for review by the borrower during the application process, however, their relationship to the first mortgage and first note should be fully explained. The second mortgage and second note secure any mortgage payments which might be made by HUD to the borrower in the event that the lender fails to make the payments under the loan Agreement.”

What the above quote says is that if the lender is unable to make payments to the borrower, then due to the second mortgage and note, HUD can step in and continue making the payments.

Additionally, the lender has the right to assign the reverse mortgage to HUD when the outstanding balance is equal to or greater than 98% of the Maximum Claim Amount, or when a request for a line of credit draw will cause the outstanding balance to equal or exceed 98% of the max claim amount. After assignment, HUD will be responsible to making all future loan advances. The second Note and Deed make this assignment possible.

Without having 2 mortgages and notes, HUD would not insure the loans and without HUD insuring the loans, lenders would not be willing to make them.

Moving on, the reason for the larger loan amount on the loan docs is that due do the fact that there is no maturity date with a reverse mortgage, HUD has designed a calculation by increasing the amount on the deed of trust by 150% of the maximum claim amount or appraised value, whichever is less.

Since reverse mortgages require no payments and the loan balance increases over time , HUD policy does not require a maximum mortgage amount to be stated in the mortgage; however most states do require an amount be stated. If the beginning balance of the loan was stated, then no amounts beyond this balance could be forwarded to the borrower.

Using an example, if a home appraised at $300,000, the amount recorded on the Note and Deed would be for $450,000. Similarly, if a home was valued at $625,500, the amount on the Deed would be $938,250. Since the current lending limit is $625,500, any home that appraises beyond $625,500 will also have $938,250 recorded.

The most important item to note is that the amount of money you owe on your reverse mortgage is equal to the money you borrow plus and accrued interest, mortgage insurance and financed fees.

So, when you go to sign your final paperwork remember that reverse mortgages have 2 Notes and 2 Deeds of Trust (or Mortgages), the amount on the loan documents will be equal to the 150% of the lesser of the maximum claim amount or appraised value and you owe only what you borrow, plus accrued interest, mortgage insurance and financed closing costs.

If you’re interested in finding out more about a reverse mortgage don’t hesitate to contact us by calling 1-888-888-4834.

Leave a Reply Cancel reply

Your email address will not be published. Required fields are marked *

- Call Us: (800) 565-1722

- How Reverse Mortgages Work

- Reverse Mortgage Pros and Cons

- Consider Downsides

- All Reverse Mortgage Calculator

- Free HECM Calculator (No Personal Info)

- Amortization Calculator

- Purchase Calculator

- 2024 Lending Limits

- Today's Reverse Mortgage Rates

- Counseling Locator

- 3 Types of Reverse Mortgages

- Home Equity Conversion Mortgage

- Jumbo Reverse Mortgage

- Purchase Reverse Mortgage

- Top 20 Reverse Mortgage Lenders

- Search by City or State

- Ask ARLO ™

- ARLO ™ Blog

- ARLO ™ Articles

America’s #1 Rated Reverse Lender

In your current area 100 homeowners are currently utilizing reverse mortgages to better enhance their retirement years, with 500,000 nationwide, great it looks like your home value estimate is about, please provide your estimated home value, the minimum qualifying age for a reverse mortgage is 55, great news your arlo ™ analysis is ready.

- Side-by-side loan comparisons

- Real-time interest rates

- ARLO™ advice to help you select the right program

- Real Time Analysis (Next Step)

- Analysis Via Email

Why Reverse Mortgages Have 2 Notes & 2 Trust Deeds

Borrowers often encounter confusion as they approach the crucial moment of signing their final documents for a reverse mortgage. They are introduced to a First and Second Trust Deed Note and Two Deeds of Trust (or mortgage, depending on the state laws applicable to the property).

Compounding the complexity, the amounts specified on the Note and Deed of Trust can be substantially higher than the sum the borrowers agreed to borrow. This discrepancy has led some borrowers to hesitate or even refuse to sign the documents at closing, primarily because they were not previously informed about the existence of multiple documents and the variances in the amounts stated.

In this article, we aim to shed light on the reasons behind the requirement for two deeds and two notes in the reverse mortgage process. Understanding the necessity for multiple documents and the rationale behind the differing amounts can significantly ease the concerns of borrowers.

Continue reading to explore the intricacies of these requirements and how they serve to protect the interests of all parties involved in a reverse mortgage transaction.

How Reverse Mortgages Are Recorded

When reading the manual on reverse mortgages, HUD explains that every reverse mortgage shall have both a First and Second Note, and while the borrower does not have to receive a copy of the Second Note before closing, its existence and relationship should be fully explained to the borrower (and thus this explanation to you).

The Second Note is not a separate loan encumbering the property as a traditional first and second loan. Instead, it secures any payments made to the borrower by HUD on their reverse mortgage. It “picks up,” if you will, where the payments made to the borrower or on the borrower’s behalf by the lender left off and those made by HUD start.

HUD Uses the Second Note For Your Protection

HUD can step into a reverse mortgage in a couple of instances and may advance funds on the part of the borrower. If the lender cannot make payments due to the borrower under the Loan Agreement, then HUD would step in and ensure that the borrower is paid.

In the case of a lender who becomes insolvent when borrowers depend on their reverse mortgage funds, HUD steps in and pays those funds to borrowers. This is one of the reasons why reverse mortgages have insurance .

HUD requires lenders to assign loans to them when the Loan to Value reaches 95% . From then on, HUD would make all future advances to the borrowers and may sometimes have to advance funds for taxes or insurance.

The second Note and Deed of Trust ensure that HUD’s position is covered under these circumstances, allowing them to continue to make any necessary advances to borrowers without the security they could not make.

How the HECM Note & Deed are Calculated

Next is the issue of the loan amount listed on the documents. HUD does not require a maximum mortgage amount to be stated on the mortgage because no payments are required. Many reverse mortgages have growth features in the lines available, and the balance owed increases as borrowers make no payments.

However, most states require an amount to be stated on the documents, leading to HUD’s dilemma. They cannot simply state the beginning balance as is the case with a typically amortizing loan or where a borrower’s borrowing power may increase with a growth rate on the line of credit or no amounts higher than this balance could be advanced to or on behalf of the borrower.

In cases such as tenure loans (payments for life) where borrowers continue to live in the home longer than the anticipated time frame, this would cause an abrupt stoppage of the payments, which would not be suitable for borrowers who depended on those monthly payments to live. Also, as is the case with the line of credit that grows over time on the unused portion, HUD states that a maximum amount stated as the beginning balance would prevent borrowers from using the growth balance of the line.

For this reason, the amount you will see on the Note and Deed (or Mortgage) will equal 150% of the Maximum Claim Amount , the total value of the property, or the HECM Lending Limit, whichever is less.

For example, if your home is worth $200,000, then the amount on the Deed would be $300,000 ($200,000 x 150%). If your home is worth $800,000, the amount on the Deed would currently be $1,200,000, and if your home value were to be at or above the current lending limit of $1,149,825 , the amount on the deed would be $1,724,737.50.

Bottom Line: You Only Owe What You Borrow

This concept is the same as a Home Equity Line of Credit (HELOC). When you close the loan, you sign documents for the entire amount. Still, you only have to repay the amount you borrow plus interest on that amount, not the entire line, if you use only some of it. The big difference is that with the reverse mortgage, there is an additional Note and Deed in case HUD also has to advance funds.

But it’s still the same – you only repay what you borrow plus the fees and interest that you financed (and any funds that the lender or HUD have to advance on your behalf, such as taxes, insurance, etc., if those are not paid in a timely manner).

So these are the things you need to know about reverse mortgage documents before it’s time to sign:

- There will be 2 Notes and 2 Deeds of Trust (or Mortgages).

- They do not secure a First and Second Lien. The second Note and Deed only secure any advances HUD may have to make to you after the lender stops and HUD begins.

- The loan amount on the documents will either be blank, total 150% of your property value or 150% of the HUD Lending Limit, whichever is less, depending on the state in which you live and their laws affecting the mortgage documents, but if an amount is stated, it will be higher than the amount of cash you are receiving at the close.

Regardless of the amount stated on the loan documents, just like HELOC documents, you only owe what you borrow plus applicable interest, mortgage insurance, financing fees, and any amounts the lender or HUD has to advance on your behalf.

You will receive a sample copy of the Note, the Deed of Trust, or the Mortgage and Security Agreement in your loan package. If you have any questions, please do not hesitate to ask so that you are not surprised at your closing.

Why are there two deeds of trust for a reverse mortgage?

Who holds the deed on a reverse mortgage, does a reverse mortgage have a note, can you deed transfer if you have a reverse mortgage, does a reverse mortgage show on the title, can you get a second mortgage lien after getting a reverse mortgage, is there a time limit from when the deed was put in my name before getting a reverse mortgage.

ARLO recommends these helpful resources:

- HUD Website

- Understanding the Reverse Mortgage Statement

Have a Question About Reverse Mortgages?

The Property ceases to be the Principal Residence of a Borrower for reasons other than death, and the property is not the Principal Residence of at least one other Borrower...

Leave a Reply to This Article

Reverse Mortgage

Reverse Mortgage Investors, HUD Contractors & Reverse Mortgage Servicers

Reverse Mortgage tax and title is one of our specialties. We provide the title work for Claim 22 Reverse Mortgage Assignments to HUD, running diligence that's specific for reverse mortgage servicers. We can conduct a HUD-specific Title Exam and Curative Review with an issue-remedy report generation.

- Reverse Mortgage Specific Title Search

- Reverse Mortgage Title Exam with Defect Flags

- Township Search for Unrecorded Liens with Demolition Check

- Reverse Mortgage Claim 22 HUD Assignment Review and Package Assembly

- Nationwide Document Prep and Recording

- Title Curative with Title Claim Support Automation, Negotiation, Gap Assign Prep, TPOL Retrieval

- TPOL Exceptions Review and Correlation to Title Results

Learn how our title reports, technology and data analysis save time and money on bulk order processing

Customer Login

Forgot password.

Everything You Need to Know About Reverse Mortgage Lending

- May 15, 2024

If you have substantial equity in your home, you might be a strong candidate for reverse mortgage lending.

In this kind of financial agreement, senior homeowners can borrow against the equity in their homes, receiving either a lump sum or regular payments. The loan is only due once they no longer live in that home.

A Home Equity Conversion Mortgage (HECM) is a specific reverse mortgage program available to those 62 years of age and older.

As the life expectancy grows in America, and more people are looking for financial stability in retirement, the HECM allows aging homeowners to tap into their wealth and make smarter decisions for their retirement.

HECMs are especially popular in California, where the cost of living and housing continues to rise. In fact, reports state that HECMs are more geographically concentrated than FHA-insured forward mortgages, and California remains the state with the largest share of HECM production .

If you think you might qualify for an HECM in California, there’s a lot to consider. Let’s dive deeper into the pros and cons of reverse mortgages, how to select one, and what makes you a good or bad candidate for this type of arrangement.

What Is a Reverse Mortgage?

In traditional mortgages, borrowers make monthly payments to a lender – but reverse mortgages work the other way around. The lender pays the homeowner, either through a lump sum, monthly payments, or a line of credit.

The loan balance increases over time as interest accumulates and is typically isn’t repaid until the homeowner sells the home, moves out permanently, or passes away.

Reverse mortgages can provide retirees with additional income, help cover expenses, or fund large purchases – but they also come with some risks, including potentially reducing the inheritance for heirs and accruing substantial interest over time.

Types of Reverse Mortgages

As we mentioned, an HECM loan is a type of reverse mortgage specifically designed for homeowners 62 and older. These loans are insured by the Federal Housing Administration (FHA) and allow homeowners to convert a portion of their home equity into cash.

HECM loans offer flexibility in how the funds can be accessed, including options for lump-sum payments, monthly payments, or a line of credit. Borrowers are not required to repay the loan as long as they continue to live in the home as their primary residence, maintain the property, and keep up with property taxes and homeowners insurance.

Proprietary

This is a type of reverse mortgage that is privately issued by a financial institution rather than being insured by the government, as is the case with federally insured Home Equity Conversion Mortgages (HECMs).

These proprietary reverse mortgages are typically offered by banks, mortgage companies, or other private lenders and may have different terms, eligibility requirements, and borrowing limits compared to HECMs. They can be advantageous for homeowners with higher home values who may exceed the maximum loan limits of HECMs or for those seeking more flexibility in accessing their home equity.

However, they may also come with higher fees and interest rates, as well as fewer consumer protections compared to federally-insured HECMs.

Single-Purpose

A single-purpose reverse mortgage is a type of reverse mortgage offered by some state and local government agencies and nonprofit organizations.

Unlike traditional reverse mortgages, which can be used for any purpose, single-purpose reverse mortgages are designed for specific use, such as paying property taxes or making home repairs. They typically have lower costs and are available to homeowners with lower incomes or higher levels of home equity.

One thing to note is that they may also have more limited eligibility criteria and loan amounts compared to other types of reverse mortgages.

The Pros and Cons of Reverse Mortgages

Like any type of financial agreement, reverse mortgages (including HECMs) come with an array of benefits and potential risks. Let’s talk about some of the biggest points any homeowner needs to recognize:

Arguably the biggest benefit of a reverse mortgage is that it provides a valuable source of supplemental income. By allowing retirees to access the equity in their homes without having to sell or downsize, a reverse mortgage can help cover living expenses, healthcare costs, or other financial needs during retirement.

Another appealing aspect of a reverse mortgage is that it eliminates the need for monthly mortgage payments. Also, the funds received from a reverse mortgage are generally tax-free, providing retirees with a significant financial advantage. They can use the money without worrying about tax implications, further enhancing their financial security in retirement.

Although reverse mortgages can be financially viable and advisable for many, there are some drawbacks to consider.

Firstly, they accrue interest and fees over time, potentially eroding the equity homeowners have built up in their homes. Additionally, the loan balance can grow substantially, especially if homeowners receive regular payments, which may leave less equity for heirs when the home is eventually sold.

Furthermore, if borrowers are unable to keep up with property taxes, insurance, and maintenance requirements, they risk defaulting on the loan, leading to foreclosure and the loss of the home. This aspect can be particularly concerning for heirs who may have hoped to inherit the property.

This brings us to our next section: understanding if the benefits of reverse mortgages outweigh the risks in your case.

Who Is a Good Candidate for a Reverse Mortgage?

The ideal candidates for a reverse mortgage are typically homeowners 62 and older who have substantial equity in their homes and are looking to supplement their retirement income without having to sell their property.

As of January 2023, the National Reverse Mortgage Lender Association estimated that seniors in the United States collectively held approximately 11.8 trillion dollars in home equity, highlighting the potential wealth tied up in residential properties.

Additionally, homeowners who have paid off their mortgages or have low remaining balances are particularly well-suited for reverse mortgages, as they can access a larger portion of their home’s equity.

It’s also best if individuals plan to stay in their homes for the long term and are financially stable enough to cover property taxes, insurance, and maintenance costs are good candidates, as these expenses are still their responsibility even with a reverse mortgage.

Common Misconceptions About Reverse Mortgages

One common concern about reverse mortgages is the fear of losing ownership of the home.

While it’s true that a reverse mortgage allows homeowners to tap into their home equity, they retain ownership of the property as long as they continue to meet the loan obligations, such as paying property taxes, insurance, and maintenance costs.

Another frequent misunderstanding involves rumors about incorrect risks, such as the belief that borrowers can owe more than the value of their home or be forced to move out if the loan balance exceeds the property’s worth.

In reality, reverse mortgages are non-recourse loans, meaning borrowers or their heirs will never owe more than the home’s appraised value at the time of repayment.

If you’ve heard confusing facts (or myths) about reverse mortgages, don’t hesitate to reach out to qualified financial professionals. HUD-approved reverse mortgage counselors can provide personalized and accurate guidance based on your specific situation.

How to Apply for a Reverse Mortgage

Your first step in accessing your full wealth is creating a clear map to success. By working with a professional, determine how much of your retirement budget is tied up in your home, what risks are associated with seeking a reverse mortgage, and how to proceed.

(2) Consider

Next, it’s time to consider which type of reverse mortgage suits your needs. Keep in mind that third-party counseling is mandatory for all reverse mortgage borrowers under the U.S. Department of Housing and Urban Development (HUD) , so you’ll need to find a certified counselor for this part of the process.

Once you’ve determined which reverse mortgage meets your needs, it’s time to apply and iron out the details with your lender – whether that be the state, a private bank, or a mortgage company.

(4) Repayment

After receiving your reverse mortgage funds, you can use them how you see fit (and under any requirements set by your loan). It’s only time to repay if you decide to sell the home or it’s no longer your primary residence.

Learn More With NeighborWorks Orange County

Our non-profit organization is committed to helping California homeowners build and maximize their wealth through various opportunities. Led by SoCal locals, we provide lending, realty, and educational tools to ensure homes are wealth-building assets – not liabilities.

If you’re interested in learning more about reverse mortgages, we’re here to help. Connect with Anthony Trinh (DRE #01420656 NMLS #334888) at (714) 408-9323 or [email protected] for more information.

U.S. Bank Foundation Boosts NeighborWorks Orange County with $225,000 Community Grant

We are thrilled to announce a generous show of support from the U.S. Bank Foundation, as it has awarded NeighborWorks Orange County with a $225,000 Community Possible grant. This substantial contribution will play a crucial role in empowering our communities and fostering positive impacts. At NeighborWorks Orange County, we are

The Black Homeownership Empowerment Initiative: Helping Black Southern Californians Build Wealth

At NeighborWorks Orange County, we’re committed to breaking down the strongest barriers to homeownership – including homeownership for Black Southern Californians. As an IRS-recognized 501(c)(3) and HUD-approved agency, we invest our profits back into our local communities instead of shareholders’ pockets. One of our primary investments is in homeownership education and

NWOC Newsletter – December 2023

As we bid farewell to 2023, the NWOC team would like to extend our heartfelt thanks to each of you for your unwavering support throughout this incredible year. Together, we’ve achieved remarkable milestones and made a positive impact in our community. Your dedication has been the driving force behind our

NeighborWorks Orange County Receives CalHFA Funding

NeighborWorks Orange County empowers people and communities to build wealth through homeownership, financial education, and access to affordable homes. With an emphasis on affordability and sustainability, our team of certified counselors provides counseling in Rental, Pre-Purchase, Mortgage Delinquency & Default and HECM/Reverse Mortgage Counseling with a goal to sustain and

Send Us A Message

NeighborWorks Orange County empowers people and communities to build wealth through home ownership,financial education, and access to affordable homes.

We are a 501(c)(3) tax exempt organization promoting home ownership since 1977. DRE# 01304167 | NMLS# 318036 1748 W. Katella Avenue Suite 202 Orange, CA 92867 714-490-1250 | [email protected]

Subscribe to our Quarterly Newsletter

Subscribe to our quarterly newsletter.

- HousingWire

- Altos Research

- Reverse Mortgage Daily

- Newsletters

- HousingWire Annual

- Gathering of Eagles

- Virtual Events

Popular Links

- Mortgage Rates Center

- Whitepapers

- Marketing Solutions

- We’re Hiring

The month in reverse mortgage rates: May 2024

Dan Hultquist returns with a look at note rates before offering a look at HECM rate movements over the past 30 days

- Click to share on Twitter (Opens in new window)

- Click to share on Facebook (Opens in new window)

- Click to share on LinkedIn (Opens in new window)

- Click to email a link to a friend (Opens in new window)

- Click to share on SMS (Opens in new window)

- Click to copy link (Opens in new window)

In March , we explored the difference between Home Equity Conversion Mortgage (HECM) “expected rates” and “note rates” and why most reverse mortgages depend on these two interest rates. In April , we specifically focused on expected rates. We showed that when expected rates increase and round up to the next 1/8% (0.125%), the principal available to a prospect is typically reduced by an average of 0.6% (of the home’s value).

In the month since my last rate update was published, expected rates increased 39 basis points (0.39%), which rounds to 3/8%, or 3 principal limit cuts. Sadly, these higher expected rates have reduced the initial funds available for new HECM applicants.

But could there be a silver lining to higher rates? Maybe. When short-term rates increase, existing HECM clients will see their borrowing capacity increase at a faster rate. This brings us to the second rate, the note rate.

What about note rates?

Interest charges simply accrue. If payments are not made, then the loan balance will rise.

Therefore, it’s understandable why rising rates might cause concern for many borrowers. However, rate increases from month-to-month don’t impact the principal and interest payments of a reverse mortgage; those required monthly payments went away when the reverse mortgage was funded.

So, what is the benefit of higher note rates?

Homeowners with sizeable loan balances generally want interest rates to go down, but borrowers who are willing and able to wait to draw funds will benefit from higher rates. This is because the unused principal of a HECM adjustable-rate mortgage (ARM) will grow at the same rate that is applied to the loan balance.

For example, a HECM loan balance accruing interest at 7.50% (+0.50% in MIP) would have a line of credit (LOC) growing at an annual rate of 8%, compounding monthly at 1/12th of that rate.

The same is true of any unused proceeds like a Life Expectancy Set-Asides (LESA). In fact, repair set-asides and funds allocated for tenure and term payments will grow in the borrower’s favor as well, providing greater borrowing power in the future.

Consider 62-year-old “Harry Homeowner” who has no existing mortgage. Harry wishes to utilize the HECM ARM line of credit and its growth for future cash flow needs. Harry establishes an initial line of credit of $200,000. The LOC and its growth can be modeled (below) to demonstrate the power of compounded growth at various rates.

- With a note rate of 5% , the LOC after 15 years would grow to $455,517 .

- With a note rate of 9% , the LOC after 15 years would grow to $826,919 .

May 2024 update

The 10-year CMT weekly average (used for calculating expected rates) increased 39 bps over the last month. However, the trend is lower after last week’s jobs report.

The current weekly average 4.61% is added to the lender margin and in effect for loans originated May 7 through May 13. The spread between the average 10 year and 1-year CMT has narrowed as shown here:

This column does not necessarily reflect the opinion of Reverse Mortgage Daily and its owners.

To contact the author of this story: Dan Hultquist at [email protected]

To contact the editor responsible for this story: Chris Clow at [email protected]

- Reverse rates

- Understanding Reverse

Leave a Reply Cancel reply

Your email address will not be published. Required fields are marked *

Save my name, email, and website in this browser for the next time I comment.

Most Popular Articles

Latest articles.

Saving for retirement is crucial for real estate agents, many of whom are self-employed. Understanding the benefits and drawbacks of each plan can help you make informed decisions and ensure a secure financial future after your last sale.

Sun Belt cities lead the way for new home sales

Higher rates are impacting future housing production , uwm cuts out title insurer with updated trac+ program, rolls out 0% down purchase initiative , hud, white house announce $40m to expand housing counseling , new york-based corcoran affiliate acquires independent brokerage .

Remember me

Don't have an account? Please Sign Up

IMAGES

VIDEO

COMMENTS

November 11th, 2020. Hello Carolyn, All HUD HECM reverse mortgages operate the same way and one of the provisions is that if the loan reaches 98% of the original value, the loan is assigned to HUD. The terms of the loan remain unchanged and you do not need to do anything.

Reverse mortgage counseling assists clients who seek to convert equity in their homes into income that can be used for any purpose such as, but not limited to, ongoing property taxes, property insurance, home repairs and improvements, medical costs, and living expenses. This chapter covers specific requirements for this type of housing counseling.

2023-10 Modifications to the Home Equity Conversion Mortgage (HECM) Assignment Claim Type 22 (CT-22) Submission Criteria and Documentation Requirements; 2023-09 ... 2015-24 Single Family Foreclosure Policy and Procedural Changes for HUD Title II Forward Mortgages and Reverse Mortgages; 2015-15 Mortgagee Optional Election Assignment for Home ...

A reverse mortgage enables you to withdraw a portion of your home's equity to supplement your income, or to purchase a home. There are no monthly principal and interest payments. The only reverse mortgage insured by the US Federal Government is called a Home Equity Conversion Mortgage (HECM) and is only available through an FHA approved lender ...

The only reverse mortgage insured by the U.S. Federal Government is called a Home Equity Conversion Mortgage (HECM), and is only available through a Federal Housing Administration (FHA)-approved lender. The HECM is the FHA's reverse mortgage program that enables you to withdraw a portion of your home's equity to use for home maintenance ...

HUD approved housing counselors provided 8% of overall housing counseling to reverse mortgages and scam awareness with over 72,916 clients served in FY 2015. Seniors 65 and older makeup 13% of the total Population. Seniors 65 years and older are expected to more than double between 2012 and 2060 (from 43.1 million to 92 million) representing 1 ...

Subject Updates to Mortgagee Optional Election (MOE) Assignment for Home Equity Conversion Mortgages (HECMs) with FHA case numbers assigned prior to August 4, 2014. Purpose Pursuant to the authority granted in the Reverse Mortgage Stabilization Act of 2013, 12 U.S.C. § 1715z-20(h)(3), this Mortgagee Letter amends regulations

7 • 1988 - HUD gains the authority to insure reverse mortgages through the FHA when President Ronald Reagan signs the reverse mortgage bill into law. The reverse mortgage government insured loan is established. • 1989 -The first FHA-insured HECM is issued to Marjorie Mason of Fairway, Kansas by the James B. Nutter Company of Kansas City, MO.

HECM Claim Type 22 (CT-22) Assignment Requests are processed through HUD's Home Equity Reverse Mortgage Information Technology (HERMIT) system. Therefore, Mortgagees should refer to the HERMIT User Guide for technical instructions on initiating and submitting a CT-22 Assignment Request. Basic Assignment Eligibility Criteria

HUD No. 23-097 HUD Public Affairs (202) 708-0685 FOR RELEASE Wednesday May 17, 2023 Federal Housing Administration Finalizes Policies to Expedite Claims Processing for Home Equity Conversion Mortgages New policies are expected to shorten the timeframe for mortgagees to receive Home Equity Conversion Mortgage assignment funds. WASHINGTON - Today, the Federal Housing

Servicing: Assignments to HUD, Part I: Reasons, Processes and Purpose. Written by Jason Perez, as originally published in The Reverse Review. Whether you are involved in reverse mortgage loan ...

The mortgagee letters listed on this page update the policies in HUD Handbook 4235.1. View all HECM Mortgagee Letters and a comprehensive list of all Mortgagee Letters on HUD.gov. 2017-12: Home Equity Conversion Mortgage (HECM) Program: Mortgage Insurance Premium Rates and Principal Limit Factors. 2016-10: Home Equity Conversion Mortgage (HECM ...

Under ML 2016-05, HUD states mortgagees may now request an extension of 30 days to the 120-day assignment requirement provided the sole reason a mortgagee is unable to submit the assignment ...

March 19, 2024, 5:03 pm By Chris Clow. The U.S. Department of Housing and Urban Development (HUD) Office of Housing Counseling (OHC) has made a series of updates to its Housing Counseling Program ...

The current policy offers reverse mortgage lenders the option of assigning a HECM loan to the U.S. Department of Housing and Urban Development (HUD) under a series of specific conditions ...

The requirements for a reverse mortgage specify a certain eligible age group (62 and over) and property standards outlined by the U.S Department of Housing and Urban Development (HUD). Some homeowners must also be prepared to set aside a portion of their reverse mortgage funds for ongoing property costs, depending on the results of the required ...

4. You risk default or foreclosure. Failing to adhere to the terms of a reverse mortgage could leave you in default on your loan. And from there, you risk foreclosure on your property. If you don ...

HUD created a March 21st deadline for reverse mortgage servicers to assign the reverse mortgage to HUD without financial penalty in order to protect certain surviving non-borrower spouses from foreclosure. This article explains the meaning of the deadline and what actions non-borrowing surviving spouses should take so that they can remain in their homes.

The Federal Housing Administration (FHA) published Mortgagee Letter (ML) 2023-10 in May that was designed to expedite the processing of assignment claims for HECM loans. It also allows for earlier ...

Key Points. You might be disqualified from getting a reverse mortgage if you don't meet age requirements, are behind on other loans and payments, or don't have enough equity in the home. Homes ...

HUD No. 24-115 HUD Public Affairs (202) 708-0685 FOR RELEASE Thursday May 16, 2024 Biden-Harris Administration Awards Nearly $40 Million to Expand Housing Counseling for Underserved Communities Vice ... Helping seniors determine whether a Home Equity Conversion Mortgage or other reverse mortgage makes sense for them. Working with Minority ...

A reverse mortgage foreclosure occurs only in specific instances per the conditions of the loan, such as the borrower's death. When one of the qualifying events transpires, the lender is owed the reverse mortgage loan balance. The owners of the home or the heirs of the former homeowner are responsible for paying back the lender.

After assignment, HUD will be responsible to making all future loan advances. The second Note and Deed make this assignment possible. ... the reason for the larger loan amount on the loan docs is that due do the fact that there is no maturity date with a reverse mortgage, HUD has designed a calculation by increasing the amount on the deed of ...

Proprietary (Non-HUD insured reverse mortgages) can also require two appraisals, but only when the home is at or above $2 million. Q. ... Larger homes, larger lot sizes, and rural properties have higher appraisal fees due to the complexity of the assignment. To determine the approximate cost for an appraisal of your home, you would need to ...

There will be 2 Notes and 2 Deeds of Trust (or Mortgages). They do not secure a First and Second Lien. The second Note and Deed only secure any advances HUD may have to make to you after the lender stops and HUD begins. The loan amount on the documents will either be blank, total 150% of your property value or 150% of the HUD Lending Limit ...

For FHA-approved reverse mortgages, you must be at least age 62, but some lenders grant jumbo reverse mortgages to those aged 55 and up. It's common to require you to have at least 50% equity in ...

Reverse Mortgage tax and title is one of our specialties. We provide the title work for Claim 22 Reverse Mortgage Assignments to HUD, running diligence that's specific for reverse mortgage servicers. We can conduct a HUD-specific Title Exam and Curative Review with an issue-remedy report generation. Reverse Mortgage Specific Title Search.

May 16, 2024, 4:46 pm By Chris Clow. The White House and the U.S. Department of Housing and Urban Development (HUD) announced on Thursday the awarding of $40 million to expand housing counseling ...

Led by SoCal locals, we provide lending, realty, and educational tools to ensure homes are wealth-building assets - not liabilities. If you're interested in learning more about reverse mortgages, we're here to help. Connect with Anthony Trinh (DRE #01420656 NMLS #334888) at (714) 408-9323 or [email protected] for more information.

The 10-year CMT weekly average (used for calculating expected rates) increased 39 bps over the last month. However, the trend is lower after last week's jobs report. The current weekly average 4 ...