For the Public

FINRA Data provides non-commercial use of data, specifically the ability to save data views and create and manage a Bond Watchlist.

For Industry Professionals

Registered representatives can fulfill Continuing Education requirements, view their industry CRD record and perform other compliance tasks.

- FINRA Gateway

For Member Firms

Firm compliance professionals can access filings and requests, run reports and submit support tickets.

For Case Participants

Arbitration and mediation case participants and FINRA neutrals can view case information and submit documents through this Dispute Resolution Portal.

Need Help? | Check Systems Status

Log In to other FINRA systems

- Frequently Asked Questions

- Interpretive Questions

- Rule Filings

- Rule Filing Status Report

- Requests for Comments

- Rulebook Consolidation

- National Adjudicatory Council (NAC)

- Office of Hearing Officers (OHO)

- Disciplinary Actions Online

- Monthly Disciplinary Actions

- Sanction Guidelines

- Individuals Barred by FINRA

- Broker Dealers

- Capital Acquisition Brokers

- Funding Portals

- Individuals

- Securities Industry Essentials Exam (SIE)

- Continuing Education (CE)

- Classic CRD

- Financial Professional Gateway (FinPro)

- Financial Industry Networking Directory (FIND)

- Conferences & Events

- FINRA Institute at Georgetown

- Financial Learning Experience (FLEX)

- Small Firm Conference Call

- Systems Status

- Entitlement Program

- Market Transparency Reporting Tools

- Regulatory Filing Systems

- Data Transfer Tools

- Cybersecurity Checklist

- Compliance Calendar

- Weekly Update Email Archive

- Peer-2-Peer Compliance Library

- Investor Insights

- Tools & Calculators

- Credit Scores

- Emergency Funds

- Investing Basics

- Investment Products

- Investment Accounts

- Working With an Investment Professional

- Investor Alerts

- Ask and Check

- Avoid Fraud

- Protect Your Identity

- For the Military

- File a Complaint

- FINRA Securities Helpline for Seniors

- Dispute Resolution

- Avenues for Recovery of Losses

Trading Options: Understanding Assignment

The options market can seem to have a language of its own. To the average investor, there are likely a number of unfamiliar terms, but for an individual with a short options position—someone who has sold call or put options—there is perhaps no term more important than " assignment "—the fulfilling of the requirements of an options contract.

Options trading carries risk and requires specific approval from an investor's brokerage firm. For information about the inherent risks and characteristics of the options market, refer to the Characteristics and Risks of Standardized Options also known as the Options Disclosure Document (ODD).

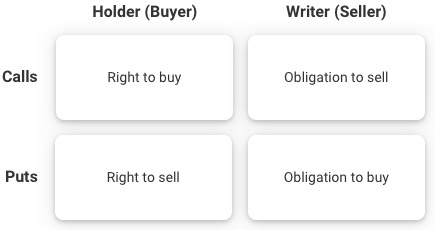

When someone buys options to open a new position ("Buy to Open"), they are buying a right —either the right to buy the underlying security at a specified price (the strike price) in the case of a call option, or the right to sell the underlying security in the case of a put option.

On the flip side, when an individual sells, or writes, an option to open a new position ("Sell to Open"), they are accepting an obligation —either an obligation to sell the underlying security at the strike price in the case of a call option or the obligation to buy that security in the case of a put option. When an individual sells options to open a new position, they are said to be "short" those options. The seller does this in exchange for receiving the option's premium from the buyer.

Learn more about options from FINRA or access free courses like Options 101 at OCC Learning .

American-style options allow the buyer of a contract to exercise at any time during the life of the contract, whereas European-style options can be exercised only during a specified period just prior to expiration. For an investor selling American-style options, one of the risks is that the investor may be called upon at any time during the contract's term to fulfill its obligations. That is, as long as a short options position remains open, the seller may be subject to "assignment" on any day equity markets are open.

What is assignment?

An option assignment represents the seller's obligation to fulfill the terms of the contract by either selling or buying the underlying security at the exercise price. This obligation is triggered when the buyer of an option contract exercises their right to buy or sell the underlying security.

To ensure fairness in the distribution of American-style and European-style option assignments, the Options Clearing Corporation (OCC), which is the options industry clearing house, has an established process to randomly assign exercise notices to firms with an account that has a short option position. Once a firm receives an assignment, it then assigns this notice to one of its customers who has a short option contract of the same series. This short option contract is selected from a pool of such customers, either at random or by some other procedure specific to the brokerage firm.

How does an investor know if an option position will be assigned?

While an option seller will always have some level of uncertainty, being assigned may be a somewhat predictable event. Only about 7% of options positions are typically exercised, but that does not imply that investors can expect to be assigned on only 7% of their short positions. Investors may have some, all or none of their short positions assigned.

And while the majority of American-style options exercises (and assignments) happen on or near the contract's expiration, a long options holder can exercise their right at any time, even if the underlying security is halted for trading. Someone may exercise their options early based upon a significant price movement in the underlying security or if shares become difficult to borrow as the result of a pending corporate action such as a buyout or takeover.

Note: European-style options can only be exercised during a specified period just prior to expiration. In U.S. markets, the majority of options on commodity and index futures are European-style, while options on stocks and exchange-traded funds (ETF) are American-style. So, while SPDR S&P 500, or SPY options, which are options tied to an ETF that tracks the S&P 500, are American-style options, S&P 500 Index options, or SPX options, which are tied to S&P 500 futures contracts, are European-style options.

What happens after an option is assigned?

An investor who is assigned on a short option position is required to meet the terms of the written option contract upon receiving notification of the assignment. In the case of a short equity call, the seller of the option must deliver stock at the strike price and in return receives cash. An investor who doesn't already own the shares will need to acquire and deliver shares in return for cash in the amount of the strike price, multiplied by 100, since each contract represents 100 shares. In the case of a short equity put, the seller of the option is required to purchase the stock at the strike price.

How might an investor's account balance fluctuate after opening a short options position?

It is normal to see an account balance fluctuate after opening a short option position. Investors who have questions or concerns or who do not understand reported trade balances and assets valuations should contact their brokerage firm immediately for an explanation. Please keep in mind that short option positions can incur substantial risk in certain situations.

For example, say XYZ stock is trading at $40 and an investor sells 10 contracts for XYZ July 50 calls at $1.00, collecting a premium of $1,000, since each contract represents 100 shares ($1.00 premium x 10 contracts x 100 shares). Consider what happens if XYZ stock increases to $60, the call is exercised by the option holder and the investor is assigned. Should the investor not own the stock, they must now acquire and deliver 1,000 shares of XYZ at a price of $50 per share. Given the current stock price of $60, the investor's short stock position would result in an unrealized loss of $9,000 (a $10,000 loss from delivering shares $10 below current stock price minus the $1,000 premium collected earlier).

Note: Even if the investor's short call position had not been assigned, the investor's account balance in this example would still be negatively affected—at least until the options expire if they are not exercised. The investor's account position would be updated to reflect the investor's unrealized loss—what they could lose if an option is exercised (and they are assigned) at the current market price. This update does not represent an actual loss (or gain) until the option is actually exercised and the investor is assigned.

What happens if an investor opened a multi-leg strategy, but one leg is assigned?

American-style option holders have the right to exercise their options position prior to expiration regardless of whether the options are in-, at- or out-of-the-money. Investors can be assigned if any market participant holding calls or puts of the same series submits an exercise notice to their brokerage firm. When one leg is assigned, subsequent action may be required, which could include closing or adjusting the remaining position to avoid potential capital or margin implications resulting from the assignment. These actions may not be attractive and may result in a loss or a less-than-ideal gain.

If an investor's short option is assigned, the investor will be required to perform in accordance with their obligation to purchase or deliver the underlying security, regardless of the overall risk of their position when taking into account other options that may be owned as part of the overall multi-leg strategy. If the investor owns an option that serves to limit the risk of the overall spread position, it is up to the investor to exercise that option or to take other action to limit risk.

Below are a couple of examples that underscore how important it is for every investor to understand the risks associated with potential assignment during market hours and potentially adverse price movements in afterhours trading.

Example #1: An investor is short March 50 XYZ puts and long March 55 XYZ puts. At the close of business on March expiration, XYZ is priced at $56 per share, and both puts are out of the money, which means they have no intrinsic value. However, due to an unexpected news announcement shortly after the closing bell, the price of XYZ drops to $40 in after-hours trading. This could result in an assignment of the short March 50 puts, requiring the investor to purchase shares of XYZ at $50 per share. The investor would have needed to exercise the long March 55 puts in order to realize the gain on the initial multi-leg position. If the investor did not exercise the March 55 puts, those puts may expire and the investor may be exposed to the loss on the XYZ purchase at $50, a $10 per share loss with XYZ now trading at $40 per share, without receiving the benefit of selling XYZ at $55.

Example #2: An investor is short March 50 XYZ puts and long April 50 XYZ puts. At the close of business on March expiration, XYZ is priced at $45 per share, and the investor is assigned XYZ stock at $50. The investor will now own shares of XYZ at $50, along with the April 50 XYZ puts, which may be exercised at the investor's discretion. If the investor chooses not to exercise the April 50 puts, they will be required to pay for the shares that were assigned to them on the short March 50 XYZ puts until the April 50 puts are exercised or shares are otherwise disposed of.

Note: In either example, the short put position may be assigned prior to expiration at the discretion of the option holder. Investors can check with their brokerage firm regarding their option exercise procedures and cut-off times.

For options-specific questions, you may contact OCC's Investor Education team at [email protected] , via chat on OptionsEducation.org or subscribe to the OIC newsletter . If you have questions about options trading in your brokerage account, we encourage you to contact your brokerage firm. If after doing so you have not resolved the issue or have additional concerns, you can contact FINRA .

Tips for Managing a Financial Windfall

Trading Terms: Time Parameters and Qualifiers on Stock Orders

It Can Be Hard to Recover from ‘Recovery’ Scams

Spread the Word: What You Need to Know About Bond Spreads

How to Prepare for and Survive Financial Hardship

Options Assignment: Navigating the Rights and Obligations

By Tyler Corvin

Ever been blindsided by an unexpected traffic ticket in the mail?

You knew driving came with its set of potential consequences, yet you took to the road regardless. Suddenly, you’re left with a tangible obligation to pay. This unforeseen shift, where what was once a mere possibility becomes an immediate reality, captures the spirit of options assignment within the vast realm of options trading.

Diving into the details, option assignment serves as the bridge between the abstract realm of rights and the concrete world of duties in this field. It’s that unassuming piece in the machinery that can, without warning, change the entire game – often carrying notable financial repercussions. In a domain where every move has implications, truly grasping option assignment is foundational, ensuring not just survival but genuine success.

Join us in this comprehensive exploration of option assignment, arming traders of all experience levels with the knowledge to sail these intricate seas with assuredness and accuracy.

What you’ll learn

What is Options Assignment?

How options assignment works, identifying option assignment , examples of option assignment, managing and mitigating assignment risks, what option assignment means for individual traders.

- Conclusion

Dive into the realm of options trading and you’ll find a tapestry of processes and potential. “Options assignment” is one pivotal cog in this intricate machine. To a newcomer, this term might seem a tad daunting. But a step-by-step walk-through can demystify its core.

In its simplest form, options assignment means carrying out the rights specified in an option contract. Holding an option allows a trader the choice to buy or sell a particular asset, but there’s no compulsion. The moment they opt to use this right, that’s when options assignment kicks in.

Think of it this way: You’ve got a ticket (option) to a show (buy or sell an asset). You decide if and when to attend. When you make the move, that transition is the options assignment.

There are two main types of option assignments:

- Call Option Assignment : Triggered when a call option holder exercises their right. The seller of the option then steps into the spotlight, bound to sell the asset at the agreed-upon price.

- Put Option Assignment : Conversely, if a put option holder steps forward, the seller of the put takes the stage. Their role? To buy the asset at the specified rate.

To truly grasp options assignment, one must understand the dance between rights and obligations in options trading.

When a trader buys an option, they’re essentially reserving a right, a possible move. On the other hand, selling an option translates to accepting a duty if the option’s holder chooses to play their card.

Rights with Call Options: Buying a call option grants you a special privilege. You can procure the underlying asset at a set price before the option expires. If you choose to exercise this right, the one who sold you the call gets assigned. Their task? Handing over the asset at that set price.

Obligations with Put Options: Securing a put option empowers you to sell the underlying at a pre-decided rate. Should you exercise this, the put’s seller steps up, committed to buying the asset at the given rate.

Several factors steer the course of options assignment, including intrinsic value, looming expiration dates, and current market vibes. To stay ahead of these influences, many traders utilize option trade alerts for timely insights. And remember, while many options might find buyers, not all see execution. Hence, not every seller will get assigned. For traders, understanding this rhythm is vital, shaping many strategies in options trading.

In the multifaceted world of options trading, discerning option assignment straddles the line between art and science. While no technique guarantees surefire results, several pointers and signals can wave a flag, hinting at an impending assignment.

In-the-Money Options : A robust sign of a looming assignment is the option’s stance relative to its strike price. “In-the-money” refers to an option’s moneyness , and plays a pivotal role in the behavior of option holders. Deeply in-the-money (ITM) options amplify the odds of assignment. An ITM call option, where the market price of the asset towers above the strike price, encourages the holder to exercise and swiftly offload the asset on the market. Conversely, an ITM put option, where the market price trails significantly behind the strike price, incentivizes the holder to scoop up the asset in the market and then exercise the option to vend it at the loftier strike price.

Expiration’s Shadow: The ticking clock of an expiring option raises the assignment stakes, especially if it remains ITM. Many traders make their move just before the eleventh hour to capitalize on their gains.

Dividend Dates in Focus: Call options inching toward expiry ahead of a dividend date, especially if they’re ITM, stand at an elevated assignment crosshair. Option aficionados might play their call options to pocket the dividend, which they’d bag if they possess the core shares.

Extrinsic Value’s Decline : A diminishing time or extrinsic value of an option elevates its exercise odds. When intrinsic value dominates an option’s worth, a holder might be inclined to cash in on this value.

Volume & Open Interest Dynamics : A sudden surge in trading or a dip in open interest can be telltale signs. Understanding volume’s role is crucial as such fluctuations might hint at traders either hopping in or out, suggesting possible exercises and assignments.

Navigating the Post-Assignment Terrain

Grasping the ripple effects of option assignment is vital, highlighting the immediate responsibilities and potential paths for both the buyer and seller.

For the Option Seller:

- Call Option Assignment : For a trader who’s sold a call option, assignment means they’re on the hook to hand over the underlying shares at the strike price. If they’re short on shares, a market purchase is in order—potentially at a loss if market prices overshoot the strike.

- Put Option Assignment: Assignment on a peddled put option necessitates the trader to buy the shares at the strike price . If this price overshadows the market rate, losses loom.

For the Option Buyer:

- Call Option Play : Exercising a call lets the buyer snap up shares at the strike price. They can either nestle with them or trade them off.

- Put Option Play: Exercising a put gives the buyer the reins to sell their shares at the strike price. This play often pays off when the market rate is dwarfed by the strike, ensuring a tidy profit on the dispensed shares.

Post-assignment, all involved must be on their toes, knowing what triggers margin calls , especially if caught off-guard by the assignment. Tax implications may also hover, influenced by the trade’s nature and the tenure of the position.

Being savvy about these subtleties and gearing up for possible turns of events can drastically refine one’s journey through the options trading maze.

Call Option Assignment Scenario

Imagine an investor purchases an Nvidia ( NVDA ) call option at a strike price of $435, hoping that the price of the stock will ascend after finding out that they may be forced to move out of some countries . The option is set to expire in a month. Soon after, not only did NVDA rebound from the news, but they reported very strong quarterly earnings, propelling the stock to $455.

Spotting the favorable trend, the investor opts to wield their right to purchase the stock at the agreed strike price of $435, despite its $455 market value. This initiates the option assignment.

The other investor, having sold the option, must now part with their NVDA shares at $435 apiece. If they’re short on stocks, they’d have to fetch them at the going rate of $455 and let them go at a deficit. The first investor, however, stands at a crossroads: retain the shares in hopes of further gains or swiftly trade them at $455, reaping a neat sum.

Put Option Assignment Scenario

Let’s visualize an investor who speculates a dip in the share price of V.F. Corporation ( VFC ) after seeing news about an activist investor causing shares to jump almost 14% in a day . To hedge their bets, they secures a put option from another investor at a strike price of $18.50, set to lapse in a month.

Fast forward a week, let’s say VFC divulges lackluster quarterly figures, causing the stock to dive to $10. The first investor, seizing the moment, employs their put option, electing to sell their shares at the $18.50 strike price.

When the assignment bell tolls, the other investor finds himself bound to buy the shares from the first investor at the agreed $18.50, a rate that overshadows the current $10 market value. The first investor thus sidesteps the market slump, securing a favorable sale. The other investor, however, absorbs a loss, acquiring stocks at a premium to their market worth.

The realm of options trading is akin to navigating a dynamic river, demanding a sharp comprehension of the risks that lie beneath its surface. A predominant risk that traders often encounter is assignment risk. When one assumes the role of an option seller, they inherit the duty to honor the contract if the buyer opts to exercise. Grasping the gravity of this can make the difference, underscoring the necessity of adept risk management.

A savvy approach to temper assignment risk is by keeping a vigilant eye on the extrinsic value of options. Generally, options rich in extrinsic value tend to resist early assignment. This resistance emerges as the extrinsic value dwindles when the option dives deeper in-the-money, thereby tempting the holder to exercise.

Furthermore, economic currents, ranging from niche corporate updates to sweeping market tides, can be triggers for option assignments. Staying attuned to these economic ripples equips traders with the vision needed to either tweak or maintain their positions. For example, traders may opt to sidestep selling options that are deeply in-the-money, given their higher susceptibility to assignments due to their shrinking extrinsic value.

Incorporating spread tactics, like vertical spreads or iron condors, furnishes an added shield. These strategies can dampen the risk of assignment since one part of the spread frequently balances the risk of its counterpart. Should the specter of a short option assignment hover, traders might contemplate ‘rolling out’ their stance. This move entails repurchasing the short option and subsequently selling another, possibly at a varied strike rate or a more distant expiry.

Yet, despite these protective layers, it remains pivotal for traders to brace for possible assignments. Maintaining ample liquidity, be it in capital or necessary shares, can avert unfavorable scenarios like hasty liquidations or stiff margin charges. Engaging regularly with brokers can also shed light, occasionally offering a heads-up on looming assignments.

In conclusion, the bedrock of risk management in options trading is rooted in perpetual learning. As traders hone their craft, their adeptness at forecasting and navigating assignment risks sharpens.

In the intricate world of options trading, option assignments aren’t just nuanced details; they’re pivotal moments with deep-seated implications for individual traders and the health of their portfolios. Beyond the immediate financial aftermath, assignments can reshape trading plans, risk dynamics, and the overarching path of an investor’s journey.

At its core, option assignments can transform a trader’s asset landscape. Consider a trader who’s short on a call option. If they’re assigned, they might be compelled to supply the underlying stock. This can result in a rapid stock outflow from their portfolio or, if they don’t possess the stock, birth a short stock stance. On the flip side, a trader short on a put option who faces assignment may find themselves buying the stock at the strike price, thereby dipping into their cash reserves.

These immediate shifts can generate broader portfolio ripples. An unexpected gain or shedding of stocks can jostle a trader’s asset distribution, veering it off their envisioned path. If, for instance, a trader had charted a particular stock-to-cash distribution or a meticulous diversification blueprint, an option assignment might throw a spanner in the works.

Additionally, assignments can serve as a real-world litmus test for a trader’s risk-handling prowess . A surprise assignment might spark margin calls for those not sufficiently fortified with capital. It stands as a poignant nudge about the essence of ensuring liquidity and safeguarding against the unpredictable whims of the market.

Strategically speaking, recurrent assignments might signal it’s time for traders to recalibrate. Are the options they’re offloading too submerged in-the-money? Have they factored in pivotal market shifts that might heighten early exercise odds? Such reflective moments can pave the way for refining and elevating trading methods.

In the multifaceted world of options trading, option assignment stands out as both a potential boon and a challenge. Far from being a simple checkbox in the process, its ramifications can mold the contours of a trader’s portfolio and steer long-term tactics. The importance of comprehending and adeptly managing option assignment resonates, whether you’re dipping your toes into options for the first time or weaving through intricate trades with seasoned expertise.

Furthermore, mastering options trading is about integrating its myriad concepts into a cohesive playbook. Whether it’s differentiating trading strategies like the iron condor from the iron butterfly strategy or delving deep into the nuances of option assignments, each component enriches the narrative of a trader’s odyssey. As markets shift and new hurdles arise, a solid grasp of foundational principles remains an invaluable asset. In this perpetual dance of learning and evolution, may your trading maneuvers always be well-informed, proactive, and adept.

Understanding Options Assignment: FAQs

What factors influence the likelihood of an option being assigned.

Several factors come into play, including the option’s intrinsic value , the time remaining until expiration, and upcoming dividend announcements. Options that are deep in the money or nearing their expiration date are more likely to be assigned.

Are Some Option Styles More Prone to Assignment than Others?

Absolutely. When considering different option styles , it’s essential to note that American-style options can be exercised at any point before their expiration, which means they face a higher risk of early assignment. In contrast, European-style options can only be exercised at expiration.

How Do Current Market Trends Impact Assignment Risk?

Factors like market volatility, notable price shifts, and external economic happenings can amplify the chances of an option being assigned. For example, an option might be assigned before a company’s ex-dividend date if the expected dividend outweighs the weakening of theta decay .

Can Traders Reverse or Counter the Effects of an Option Assignment?

Once an option has been assigned, it’s set in stone. However, traders can maneuver within the market to balance out the implications of the assignment, such as procuring or selling the underlying asset.

Are There Any Fees Tied to Option Assignments?

Indeed, brokers usually impose a fee for both assignments and exercises. The specific fee can differ depending on the broker, making it essential for traders to understand their brokerage’s charging scheme.

Ex Ante vs Ex Post: Comparison Guide

Spot Market: Definition, Mechanics

What Are Illiquid Assets?

What is a Liquid Asset?

Follow-on Offering: Explained to Traders

Please upgrade your browser

E*TRADE uses features that may not be supported by your current browser and might not work as intended. For the best user experience, please use an updated browser .

Understanding assignment risk in Level 3 and 4 options strategies

E*TRADE from Morgan Stanley

With all options strategies that contain a short option position, an investor or trader needs to keep in mind the consequences of having that option assigned , either at expiration or early (i.e., prior to expiration). Remember that, in principle, with American-style options a short position can be assigned to you at any time. On this page, we’ll run through the results and possible responses for various scenarios where a trader may be left with a short position following an assignment.

Before we look at specifics, here’s an important note about risk related to out-of-the-money options: Normally, you would not receive an assignment on an option that expires out of the money. However, even if a short position appears to be out of the money, it might still be assigned to you if the stock were to move against you just prior to expiration or in extended aftermarket or weekend trading hours. The only way to eliminate this risk is to buy-to-close the short option.

- Short (naked) calls

Credit call spreads

Credit put spreads, debit call spreads, debit put spreads.

- When all legs are in-the-money or all are out-of-the-money at expiration

Another important note : In any case where you close out an options position, the standard contract fee (commission) will be charged unless the trade qualifies for the E*TRADE Dime Buyback Program . There is no contract fee or commission when an option is assigned to you.

Short (naked) call

| If it's at expiration | If it's at expiration |

|---|---|

| This means your account must be able to deliver shares of the underlying—i.e., sell them at the strike price. If your account doesn't have the buying power to cover the sale of shares, you may receive a margin call. Actions you can take: If you don’t want to sell your shares or you don’t own any, you can buy the call option before it expires, closing out the position and eliminating the risk of assignment. |

If you experience an early assignment

An early assignment is most likely to happen if the call option is deep in the money and the stock’s ex-dividend date is close to the option expiration date.

If your account does not hold the shares needed to cover the obligation, an early assignment would create a short stock position in your account. This may incur borrowing fees and make you responsible for any dividend payments.

Also note that if you hold a short call on a stock that has a dividend payment coming in the near future, you may be responsible for paying the dividend even if you close the position before it expires.

| If it's at expiration | If it's at expiration |

|---|---|

| This means your account must have enough money to buy the shares of the underlying at the strike price or you may incur a margin call. Actions you can take: If you don’t have the money to pay for the shares, you can buy the put option before it expires, closing out the position and eliminating the risk of assignment and the risk of a margin call. |

An early assignment generally happens when the put option is deep in the money and the underlying stock does not have an ex-dividend date between the current time and the expiration of the option.

Short call + long call

(The same principles apply to both two-leg and four-leg strategies)

| If the and the at expiration |

|---|

| This means your account will deliver shares of the underlying—i.e., sell them at the strike price. Actions you can take: If you don’t have the shares to sell, or don’t want to establish a short stock position, you can buy the short call before expiration, closing out the position. If the short leg is closed before expiration, the long leg may also be closed, but it will likely not have any value and can expire worthless. |

This would leave your account short the shares you’ve been assigned, but the risk of the position would not change . The long call still functions to cover the short share position. Typically, you would buy shares to cover the short and simultaneously sell the long leg of the spread.

Pay attention to short in-the-money call legs on the day prior to the stock’s ex-dividend date, because an assignment that evening would put you in a short stock position where you are responsible for paying the dividend. If there’s a risk of early assignment, consider closing the spread.

Short put + long put

| If the and the at expiration |

|---|

| This means your account will buy shares of the underlying at the strike price. Actions you can take: If you don’t have the money to pay for the shares, or don’t want to, you can buy the put option before it expires, closing out the position and eliminating the risk of assignment. Once the short leg is closed, you can try to sell the long leg if it has any value, or let it expire worthless if it doesn’t. |

Early assignment would leave your account long the shares you’ve been assigned. If your account does not have enough buying power to purchase the shares when they are assigned, this may create a Fed call in your account.

However, the long put still functions to cover the position because it gives you the right to sell shares at the long put strike price. Typically, you would sell the shares in the market and close out the long put simultaneously.

Here's a call example

- Let’s say that you’re short a 100 call and long a 110 call on XYZ stock; both legs are in-the-money.

- You receive an assignment notification on your short 100 call, meaning you sell 100 shares of XYZ stock at 100. Now, you have $10,000 in short stock proceeds, your account is short 100 shares of stock, and you still hold the long 110 call.

- Exercise your long 110 call, which would cover the short stock position in your account.

- Or, buy 100 shares of XYZ stock (to cover your short stock position) and sell to close the long 110 call.

Here's a put example:

- Let’s say that you’re short a 105 put and long a 95 put on XYZ stock; the short leg is in-the-money.

- You receive an assignment notification on your short 105 put, meaning you buy 100 shares of XYZ stock at 105. Now, your account has been debited $10,500 for the stock purchase, you hold 100 shares of stock, and you still hold the long 95 put.

- The debit in your account may be subject to margin charges or even a Fed call, but your risk profile has not changed.

- You can sell to close 100 shares of stock and sell to close the long 95 put.

Long call + short call

| If the and the at expiration |

|---|

| This means your account will buy shares at the long call’s strike price. Actions you can take: If you don’t have enough money in your account to pay for the shares, or you don’t want to, you can simply sell the long call option before it expires, closing out the position. However, unless you are approved for Level 4 options trading, you must close out the short leg first (or simultaneously). The easiest way to do this is to use the spread order ticket to buy to close the short leg and sell to close the long leg. Assuming the short leg is worth less than $0.10, the E*TRADE Dime Buyback program would apply, and you’ll pay no commission to close that leg. |

Debit spreads have the same early assignment risk as credit spreads only if the short leg is in-the-money.

An early assignment would leave your account short the shares you’ve been assigned, but the risk of the position would not change . The long call still functions to cover the short share position. Typically, you would buy shares to cover the short share position and simultaneously sell the remaining long leg of the spread.

Long put + short put

| If the and the at expiration |

|---|

| This means your account will buy shares at the long call’s strike price. Actions you can take: If you don’t have the shares, the automatic exercise would create a short position in your account. To avoid this, you can simply sell the put option before it expires, closing out the position. However, you may not have the buying power to close out the long leg unless you close out the short leg first (or simultaneously). The easiest way to do this is to use the spread order ticket to buy to close the short leg and sell to close the long leg. Assuming the short leg is worth less than $0.10, the E*TRADE Dime Buyback program would apply, and you’ll pay no commission to close that leg. |

An early assignment would leave your account long the shares you’ve been assigned. If your account does not have enough buying power to purchase the shares when they are assigned, this may create a Fed call in your account.

All spreads that have a short leg

(when all legs are in-the-money or all are out-of-the-money)

| If all legs are at expiration | If all legs are at expiration |

|---|---|

| For call spreads, this will buy shares at the long call’s strike price and sell shares at the short call’s strike price. For put spreads, this will sell shares at the long put strike price and buy shares at the short put strike price. In either case, this will happen in the account after expiration, usually overnight, and is called . Your account does not need to have money available to buy shares for the long call or short put because the sale of shares from the short call or long put will cover the cost. There will be no Fed call or margin call. |

Pay attention to short in-the-money call legs on the day prior to the stock’s ex-dividend date because an assignment that evening would put you in a short stock position where you are responsible for paying the dividend. If there’s a risk of early assignment, consider closing the spread.

However, the long put still functions to cover the long stock position because it gives you the right to sell shares at the long put strike price. Typically, you would sell the shares in the market and close out the long put simultaneously.

What to read next...

How to buy call options, how to buy put options, potentially protect a stock position against a market drop, looking to expand your financial knowledge.

- Find a Branch

- Schwab Brokerage 800-435-4000

- Schwab Password Reset 800-780-2755

- Schwab Bank 888-403-9000

- Schwab Intelligent Portfolios® 855-694-5208

- Schwab Trading Services 888-245-6864

- Workplace Retirement Plans 800-724-7526

... More ways to contact Schwab

Chat

- Schwab International

- Schwab Advisor Services™

- Schwab Intelligent Portfolios®

- Schwab Alliance

- Schwab Charitable™

- Retirement Plan Center

- Equity Awards Center®

- Learning Quest® 529

- Mortgage & HELOC

- Charles Schwab Investment Management (CSIM)

- Portfolio Management Services

- Open an Account

The Risks of Options Assignment

Any trader holding a short option position should understand the risks of early assignment. An early assignment occurs when a trader is forced to buy or sell stock when the short option is exercised by the long option holder. Understanding how assignment works can help a trader take steps to reduce their potential losses.

Understanding the basics of assignment

An option gives the owner the right but not the obligation to buy or sell stock at a set price. An assignment forces the short options seller to take action. Here are the main actions that can result from an assignment notice:

- Short call assignment: The option seller must sell shares of the underlying stock at the strike price.

- Short put assignment: The option seller must buy shares of the underlying stock at the strike price.

For traders with long options positions, it's possible to choose to exercise the option, buying or selling according to the contract before it expires. With a long call exercise, shares of the underlying stock are bought at the strike price while a long put exercise results in selling shares of the underlying stock at the strike price.

When a trader might get assigned

There are two components to the price of an option: intrinsic 1 and extrinsic 2 value. In the case of exercising an in-the-money 3 (ITM) long call, a trader would buy the stock at the strike price, which is lower than its prevailing price. In the case of a long put that isn't being used as a hedge for a long stock position, the trader shorts the stock for a price higher than its prevailing price. A trader only captures an ITM option's intrinsic value if they sell the stock (after exercising a long call) or buy the stock (after exercising a long put) immediately upon exercise.

Without taking these actions, a trader takes on the risks associated with holding a long or short stock position. The question of whether a short option might be assigned depends on if there's a perceived benefit to a trader exercising a long option that another trader has short. One way to attempt to gauge if an option could be potentially assigned is to consider the associated dividend. An options seller might be more likely to get assigned on a short call for an upcoming ex-dividend if its time value is less than the dividend. It's more likely to get assigned holding a short put if the time value has mostly decayed or if the put is deep ITM and close to expiration with a wide bid/ask spread on the stock.

It's possible to view this information on the Trade page of the thinkorswim ® trading platform. Review past dividends, the price of the short call, and the price of the put at the call's strike price. While past performance cannot be relied upon to continue, this information can help a trader determine whether assignment is more or less likely.

Reducing the risk associated with assignment

If a trader has a covered call that's ITM and it's assigned, the trader will deliver the long stock out of their account to cover the assignment.

A trader with a call vertical spread 4 where both options are ITM and the ex-dividend date is approaching may want to exercise the long option component before the ex-dividend date to have long stock to deliver against the potential assignment of the short call. The trader could also close the ITM call vertical spread before the ex-dividend date. It might be cheaper to pay the fees to close the trade.

Another scenario is a call vertical spread where the ITM option is short and the out-of-the-money (OTM) option is long. In this case, the trader may consider closing the position or rolling it to a further expiration before the ex-dividend date. This move can possibly help the trader avoid having short stock on the ex-dividend date and being liable for the dividend.

Depending on the situation, a trader long an ITM call might decide it's better to close the trade ahead of the ex-dividend date. On the ex-dividend date, the price of the stock drops by the amount of the dividend. The drop in the stock price offsets what a trader would've earned on the dividend and there would still be fees on top of the price of the put.

Assess the risk

When an option is converted to stock through exercise or assignment, the position's risk profile changes. This change could increase the margin requirements, or subject a trader to a margin call, 5 or both. This can happen at or before expiration during early assignment. The exercise of a long option position can be more likely to trigger a margin call since naked short option trades typically carry substantial margin requirements.

Even with early exercise, a trader can still be assigned on a short option any time prior to the option's expiration.

1 The intrinsic value of an options contract is determined based on whether it's in the money if it were to be exercised immediately. It is a measure of the strike price as compared to the underlying security's market price. For a call option, the strike price should be lower than the underlying's market price to have intrinsic value. For a put option the strike price should be higher than underlying's market price to have intrinsic value.

2 The extrinsic value of an options contract is determined by factors other than the price of the underlying security, such as the dividend rate of the underlying, time remaining on the contract, and the volatility of the underlying. Sometimes it's referred to as the time value or premium value.

3 Describes an option with intrinsic value (not just time value). A call option is in the money (ITM) if the underlying asset's price is above the strike price. A put option is ITM if the underlying asset's price is below the strike price. For calls, it's any strike lower than the price of the underlying asset. For puts, it's any strike that's higher.

4 The simultaneous purchase of one call option and sale of another call option at a different strike price, in the same underlying, in the same expiration month.

5 A margin call is issued when the account value drops below the maintenance requirements on a security or securities due to a drop in the market value of a security or when buying power is exceeded. Margin calls may be met by depositing funds, selling stock, or depositing securities. A broker may forcibly liquidate all or part of the account without prior notice, regardless of intent to satisfy a margin call, in the interests of both parties.

Just getting started with options?

More from charles schwab.

Today's Options Market Update

What to Know About Zero-Days-to-Expiration Options

Income-Generating ETFs: Covered-Call vs. Dividend?

Related topics.

Options carry a high level of risk and are not suitable for all investors. Certain requirements must be met to trade options through Schwab. Please read the options disclosure document titled Characteristics and Risks of Standardized Options before considering any options transaction. Supporting documentation for any claims or statistical information is available upon request.

With long options, investors may lose 100% of funds invested.

Spread trading must be done in a margin account.

Multiple leg options strategies will involve multiple commissions.

Commissions, taxes and transaction costs are not included in this discussion, but can affect final outcome and should be considered. Please contact a tax advisor for the tax implications involved in these strategies.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

- Why Merrill

- Open An Account

- Pricing & Fees

- BofA Preferred Rewards

- Investing & Banking Connected

- Mobile Investing

- Sustainable Investing

- Awards & Accolades

888.637.3343

To find the small business retirement plan that works for you, contact:

Learn more about an advisor's background on FINRA's BrokerCheck

- Merrill Edge ® Self-Directed

- Merrill Guided Investing

- Invest with an Advisor

- Compare All

- General Investing

- Education Accounts

- Mutual Funds

- Fixed Income & Bonds

- Margin Trading

- Order Execution Quality

- Idea Builder

- Merrill Edge MarketPro ®

- Personal Retirement Calculator

- College Cost Calculator

- Retirement Account Selector

- 401(k) Rollover Calculator

- 529 Plan State Tax Calculator

- View All Tools

- New to Investing

- Plan for College

- Tax Planning

- Investing by Life Stages

- Traditional IRA

- Income in Retirement

- Plan for Retirement

- Retirement Tools

- Small Business 401(k)

- Individual 401(k)

- View All Plans

- Get Started Investing

- Investing Basics

- Market & Investing Insights

- Individual Investing Account

- Joint Investing Account

- Custodial Investing Account

- Traditional Inherited IRA

- Roth Inherited IRA

- 529 College Savings Plans

- Custodial UGMA/UTMA Accounts

- Business Investor Account

- lnvesting Costs & Fees

- Pricing & Fees

- Investing & Banking Connected

- Awards & Accolades

- Merrill Edge ® Self-Directed

- Investing with an Advisor

- Compare all

- Fixed Income & Bonds

- Merrill Edge MarketPro ®

- 401(k) Rollover Tool

- View all tools

- Tax Plannning

- View all plans

- Market & Investing Insights

- Help When You Want It Find answers to common questions at Merrill Schedule an appointment with Merrill To find the small business retirement plan that works for you, contact: [email protected]

Exercising Options

Submitting exercise or do-not-exercise instructions:.

- All Instructions must be called in and are only applicable to long positions

- Do-Not-Exercise instructions can only be submitted the day of expiration up through market close

- Exercise instructions can be submitted at any time until expiration

- Merrill may take action at any time to close out positions that may not be able to be supported if exercised/assigned. It is extremely important to monitor your open options positions and be aware of your risk exposure.

What's the Net?

Automatic exercise/ assignment, early exercise/assignment, without the jargon, what are options, what are the types of options, what are the greeks, similar articles, options pricing, equity option basics, equity index options.

This material is not intended as a recommendation, offer or solicitation for the purchase or sale of any security or investment strategy. Merrill offers a broad range of brokerage, investment advisory (including financial planning) and other services. Additional information is available in our Client Relationship Summary (PDF) .

| Are Not FDIC Insured | Are Not Bank Guaranteed | May Lose Value |

| Are Not Deposits | Are Not Insured by Any Federal Government Agency | Are Not a Condition to Any Banking Service or Activity |

I'd Like to

- Create an Emergency Fund

- Create an Investment Strategy

- Open an Account with Merrill

Discover Merrill

- Bank of America Preferred Rewards

- Online Trading

- Awards & Recognition

Representatives are available 24/7

Unlimited $0 Trades

Investing in securities involves risks, and there is always the potential of losing money when you invest in securities.

The performance data contained herein represents past performance which does not guarantee future results. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. For performance information current to the most recent month end, please contact us.

Net Asset Value (NAV) returns are based on the prior-day closing NAV value at 4 p.m. ET. NAV returns assume the reinvestment of all dividend and capital gain distributions at NAV when paid.

Market price returns are based on the prior-day closing market price, which is the average of the midpoint bid-ask prices at 4 p.m. ET. Market price returns do not represent the returns an investor would receive if shares were traded at other times.

Returns include fees and applicable loads. Since Inception returns are provided for funds with less than 10 years of history and are as of the fund's inception date. 10 year returns are provided for funds with greater than 10 years of history.

Before investing consider carefully the investment objectives, risks, and charges and expenses of the fund, including management fees, other expenses and special risks. This and other information may be found in each fund's prospectus or summary prospectus, if available. Always read the prospectus or summary prospectus carefully before you invest or send money. Prospectuses can be obtained by contacting us.

Expense Ratio – Gross Expense Ratio is the total annual operating expense (before waivers or reimbursements) from the fund's most recent prospectus. You should also review the fund's detailed annual fund operating expenses which are provided in the fund's prospectus.

This material is not intended as a recommendation, offer or solicitation for the purchase or sale of any security or investment strategy. Merrill offers a broad range of brokerage, investment advisory (including financial planning) and other services. Additional information is available in our Client Relationship Summary (Form CRS) (PDF) .

Banking products are provided by Bank of America, N.A. and affiliated banks, Members FDIC and wholly owned subsidiaries of Bank of America Corporation ("BofA Corp.").

Merrill Lynch Life Agency Inc. (MLLA) is a licensed insurance agency and wholly owned subsidiary of BofA Corp.

| Are Not FDIC Insured | Are Not Bank Guaranteed | May Lose Value |

| Are Not Deposits | Are Not Insured by Any Federal Government Agency | Are Not a Condition to Any Banking Service or Activity |

© 2024 Bank of America Corporation. All rights reserved.

5676695-05112024

You're reading a free article with opinions that may differ from The Motley Fool's Premium Investing Services. Become a Motley Fool member today to get instant access to our top analyst recommendations, in-depth research, investing resources, and more. Learn More

Ready for Options Trading? Make Sure You Understand Assignment First

Your first assignment: decoding this important options term before you start trading.

The options market can seem to have a language of its own. To the average investor, there are likely a number of unfamiliar terms, but for an individual with a short options position—someone who has sold call or put options—there is perhaps no term more important than " assignment "—the fulfilling of the requirements of an options contract.

When someone buys options to open a new position ("Buy to Open"), they are buying a right —either the right to buy the underlying security at a specified price (the strike price) in the case of a call option, or the right to sell the underlying security in the case of a put option.

Image source: Getty Images

On the flip side, when an individual sells, or writes, an option to open a new position ("Sell to Open"), they are accepting an obligation —either an obligation to sell the underlying security at the strike price in the case of a call option or the obligation to buy that security in the case of a put option. When an individual sells options to open a new position, they are said to be "short" those options. The seller does this in exchange for receiving the option's premium from the buyer.

American-style options allow the buyer of a contract to exercise at any time during the life of the contract, whereas European-style options can be exercised only during a specified period just prior to expiration. For an investor selling American-style options, one of the risks is that the investor may be called upon at any time during the contract's term to fulfill its obligations. That is, as long as a short options position remains open, the seller may be subject to "assignment" on any day equity markets are open.

What is assignment?

An option assignment represents the seller's obligation to fulfill the terms of the contract by either selling or buying the underlying security at the exercise price. This obligation is triggered when the buyer of an option contract exercises their right to buy or sell the underlying security.

To ensure fairness in the distribution of American-style and European-style option assignments, the Options Clearing Corporation (OCC), which is the options industry clearing house, has an established process to randomly assign exercise notices to firms with an account that has a short option position. Once a firm receives an assignment, it then assigns this notice to one of its customers who has a short option contract of the same series. This short option contract is selected from a pool of such customers, either at random or by some other procedure specific to the brokerage firm.

How does an investor know if an option position will be assigned?

While an option seller will always have some level of uncertainty, being assigned may be a somewhat predictable event. Only about 7% of options positions are typically exercised, but that does not imply that investors can expect to be assigned on only 7% of their short positions. Investors may have some, all or none of their short positions assigned.

And while the majority of American-style options exercises (and assignments) happen on or near the contract's expiration, a long options holder can exercise their right at any time, even if the underlying security is halted for trading. Someone may exercise their options early based upon a significant price movement in the underlying security or if shares become difficult to borrow as the result of a pending corporate action such as a buyout or takeover.

Note: European-style options can only be exercised during a specified period just prior to expiration. In U.S. markets, the majority of options on commodity and index futures are European-style, while options on stocks and exchange-traded funds (ETF) are American-style. So, while SPDR S&P 500 , or SPY options, which are options tied to an ETF that tracks the S&P 500, are American-style options, S&P 500 Index options, or SPX options, which are tied to S&P 500 futures contracts, are European-style options.

What happens after an option is assigned?

An investor who is assigned on a short option position is required to meet the terms of the written option contract upon receiving notification of the assignment. In the case of a short equity call, the seller of the option must deliver stock at the strike price and in return receives cash. An investor who doesn't already own the shares will need to acquire and deliver shares in return for cash in the amount of the strike price, multiplied by 100, since each contract represents 100 shares. In the case of a short equity put, the seller of the option is required to purchase the stock at the strike price.

How might an investor's account balance fluctuate after opening a short options position?

It is normal to see an account balance fluctuate after opening a short option position. Investors who have questions or concerns or who do not understand reported trade balances and assets valuations should contact their brokerage firm immediately for an explanation. Please keep in mind that short option positions can incur substantial risk in certain situations.

What does "XYZ July 50" mean? XYZ = the ticker symbol of the security July = the month when the option will expire 50 = $50, the strike price on the option

For example, say XYZ stock is trading at $40 and an investor sells 10 contracts for XYZ July 50 calls at $1.00, collecting a premium of $1,000, since each contract represents 100 shares ($1.00 premium x 10 contracts x 100 shares). Consider what happens if XYZ stock increases to $60, the call is exercised by the option holder and the investor is assigned. Should the investor not own the stock, they must now acquire and deliver 1,000 shares of XYZ at a price of $50 per share. Given the current stock price of $60, the investor's short stock position would result in an unrealized loss of $9,000 (a $10,000 loss from delivering shares $10 below current stock price minus the $1,000 premium collected earlier).

Note: Even if the investor's short call position had not been assigned, the investor's account balance in this example would still be negatively affected—at least until the options expire if they are not exercised. The investor's account position would be updated to reflect the investor's unrealized loss—what they could lose if an option is exercised (and they are assigned) at the current market price. This update does not represent an actual loss (or gain) until the option is actually exercised and the investor is assigned.

What happens if an investor opened a multi-leg strategy, but one leg is assigned?

American-style option holders have the right to exercise their options position prior to expiration regardless of whether the options are in-, at- or out-of-the-money. Investors can be assigned if any market participant holding calls or puts of the same series submits an exercise notice to their brokerage firm. When one leg is assigned, subsequent action may be required, which could include closing or adjusting the remaining position to avoid potential capital or margin implications resulting from the assignment. These actions may not be attractive and may result in a loss or a less-than-ideal gain.

If an investor's short option is assigned, the investor will be required to perform in accordance with their obligation to purchase or deliver the underlying security, regardless of the overall risk of their position when taking into account other options that may be owned as part of the overall multi-leg strategy. If the investor owns an option that serves to limit the risk of the overall spread position, it is up to the investor to exercise that option or to take other action to limit risk.

Below are a couple of examples that underscore how important it is for every investor to understand the risks associated with potential assignment during market hours and potentially adverse price movements in afterhours trading.

Example #1: An investor is short March 50 XYZ puts and long March 55 XYZ puts. At the close of business on March expiration, XYZ is priced at $56 per share, and both puts are out of the money, which means they have no intrinsic value. However, due to an unexpected news announcement shortly after the closing bell, the price of XYZ drops to $40 in after-hours trading. This could result in an assignment of the short March 50 puts, requiring the investor to purchase shares of XYZ at $50 per share. The investor would have needed to exercise the long March 55 puts in order to realize the gain on the initial multi-leg position. If the investor did not exercise the March 55 puts, those puts may expire and the investor may be exposed to the loss on the XYZ purchase at $50, a $10 per share loss with XYZ now trading at $40 per share, without receiving the benefit of selling XYZ at $55.

Example #2: An investor is short March 50 XYZ puts and long April 50 XYZ puts. At the close of business on March expiration, XYZ is priced at $45 per share, and the investor is assigned XYZ stock at $50. The investor will now own shares of XYZ at $50, along with the April 50 XYZ puts, which may be exercised at the investor's discretion. If the investor chooses not to exercise the April 50 puts, they will be required to pay for the shares that were assigned to them on the short March 50 XYZ puts until the April 50 puts are exercised or shares are otherwise disposed of.

Note: In either example, the short put position may be assigned prior to expiration at the discretion of the option holder. Investors can check with their brokerage firm regarding their option exercise procedures and cut-off times.

For options-specific questions, you may contact OCC's Investor Education team at [email protected] , via chat on OptionsEducation.org or subscribe to the OIC newsletter . If you have questions about options trading in your brokerage account, we encourage you to contact your brokerage firm. If after doing so you have not resolved the issue or have additional concerns, you can contact FINRA .

Subscribe to FINRA's newsletter for more information about saving and investing.

FINRA Staff has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy .

Related Articles

Premium Investing Services

Invest better with The Motley Fool. Get stock recommendations, portfolio guidance, and more from The Motley Fool's premium services.

Will I Be Assigned?

by Mike Scanlin

As the market nears closing time on expiration Friday, covered call writers want to know if they will be assigned or not for tax reasons, margin reasons, and portfolio optimization reasons. Let's look at the issue from the point of view of both people involved in the trade: the option holder who is long the call option, and the covered call writer who is short the same call option.

Option Assignment

"Assignment" means the call option you sold short as part of your covered call trade is now being exercised. That means some option holder somewhere wants his stock and you have been chosen by the OCC (Options Clearing Corp) to receive the assignment. It's a random process; each time the OCC gets an exercise notice they randomly choose from among all the short calls (in the same series) who will receive the assignment.

If you are chosen by OCC your broker will be notified and your broker will, in turn, notify you. You will need to make good on your promise to deliver the shares of stock and, in exchange, receive the strike-price-per-share in cash, as per the option agreement.

What determines if the option holder exercises?

It's really up to them. It's their option and they can do what they want with it. They can even exercise it if the stock price is below the strike price of the option (i.e. it's out of the money). It wouldn't make any economic sense to do so, but it is allowed. The option holder has the right to exercise at any time for any reason.

Normal circumstances when call options are exercised by rational people

(1) The stock closes above the strike price on the option's expiration day.

This is the typical case for exercise. The option holder exercises his in-the-money option to acquire the stock for less than the current price. He only has to pay the strike price. If the stock closes at $43 and the strike price is 40, he only pays $40/share to acquire the stock.

(2) For in-the-money options, the day before ex-dividend day when there is zero time premium remaining in the option.

This is called "early exercise" and normally only happens when there is no time premium left in the option because the option holder forfeits any remaining time premium when he exercises. It doesn't make economic sense for him to exercise when there is still time premium remaining in the option; he's better off just selling the option in that case. But if there is zero time premium and he knows the stock is likely to open lower the next morning by the amount of the dividend that is about to be paid, he will do an early exercise to capture the dividend.

What about the day before earnings?

That's not a good time to exercise an option. There will be lots of time premium in the option (which will be forfeited if exercised) because of earnings uncertainty. If the option holder wants out of the position (maybe he's worried about volatility decreasing after earnings come out which could lower the value of his option) then he's better off just selling the option instead of exercising it.

What if the stock closes very near the strike price?

This one is tricky.

For starters, stocks continue to trade for several hours in the aftermarket after the regular market closes. The stock's closing price Friday at 4pm Eastern Time (regular market hours closing) may not represent the closing price during extended hours trading. And option holders have until Saturday (when options technically expire) to give their brokers exercise notices. So it's possible for a stock to close just below the strike price during regular hours on expiration Friday but then close above the strike price in extended hours. In that case the option would likely be exercised.

But not always.

It depends on several factors: (1) What are the transaction costs of the person doing the exercising? (2) What is the personal opinion of the option holder for the stock at Monday morning's open? It's possible the option could finish slightly in the money during extended trading hours and still not be exercised because the option holder believes the stock will open lower (below the strike price) on Monday morning. Maybe there's some event happening over the weekend that he believes will cause the stock (or the whole market) to open lower on Monday.

Imagine a covered call that has been written at a strike of 50. On expiration Friday at the close the stock's price was within a few pennies of 50 (above or below; it doesn't matter). Will it be exercised?

It depends on what the option holder believes will happen Monday morning. And not all option holders believe the same thing, causing less than 100% of all 50-strike options to be exercised. And since option assignment is random, you can't be sure if you'll be assigned or not. The purple oval here is a mystery and subject to personal opinion:

The decision to exercise (or not) is the option holder's right but not his obligation . He can let in-the-money options expire unexercised if he so chooses, based on his beliefs of where the stock will open on the next trading day.

My stock is within a few cents of the strike price and it's almost closing time on expiration day. What should I do?

This is the most common question. The answer is "it depends", "do you feel lucky?", and "you can never tell for sure." If you don't want the stock called away for whatever reason (taxes, margin, etc) then buy the call option back before the option market closes. It may cost you a nickel or two (plus an option trade commission) but that's the only certain way to avoid assignment.

Remember, stocks trade for a few more hours after the regular market closes so if your stock closes 10 cents below the strike during regular hours but then rises 25 cents above the strike during extended hours then you are probably out of luck. It will likely be called away (unlike stocks, options don't trade after hours, so you can't buy the option back during extended trading hours).

If you are in a situation where you don't want something called away then the best plan is to monitor the amount of time premium remaining in the option. Most option holders won't exercise if the time premium is greater than zero. If your time premium is getting small (5 to 10 cents, depends on the bid-ask spread of the underlying stock) then it's a good time to roll the option to something that has more time premium in it. The greater the time premium the smaller chance of exercise.

How do I calculate time premium?

The short answer for in-the-money options is (strike price + call price) minus stock price. So if the stock is 53 and you've sold a 50-strike call currently trading at 4 then the time premium is (50 + 4) - 53 = 1. There is 1 point of time premium in the option.

The longer answer is that stocks and options have bid prices and ask prices. So which to use? Or should you use the last trade price? We'll cover that in a future article . In the mean time, check out the tutorial on time premium .

Like covered calls? Check out our Covered Call Screener

Mike Scanlin is the founder of Born To Sell and has been writing covered calls for a long time.

- Covered Call Newsletter

- Covered Call Blog

- Search Search Please fill out this field.

- Assets & Markets

What Is an Option Assignment?

:max_bytes(150000):strip_icc():format(webp)/image0-MichaelBoyle-30f78c37d3174fe298f9407f0b5413e2.jpeg "stock assignment call option")

Definition and Examples of Assignment

How does assignment work, what it means for individual investors.

Morsa Images / Getty Images

An option assignment represents the seller of an option’s obligation to fulfill the terms of the contract by either selling or purchasing the underlying security at the exercise price. Let’s explain what that means in more detail.

Key Takeaways

- An assignment represents the seller of an option’s obligation to fulfill the terms of the contract by either selling or purchasing the underlying security at the exercise price.

- If you sell an option and get assigned, you have to fulfill the transaction outlined in the option.

- You can only get assigned if you sell options, not if you buy them.

- Assignment is relatively rare, with only 7% of options ultimately getting assigned.

An assignment represents the seller of an option’s obligation to fulfill the terms of the contract by either selling or purchasing the underlying security at the exercise price. Let’s explain what that means in more detail.

When you sell an option to someone, you’re selling them the right to make you engage in a future transaction. For example, if you sell someone a put option , you’re promising to buy a stock at a set price any time between when the transaction happens and the expiration date of the option.

If the holder of the option doesn’t do anything with the option by the expiration date, the option expires. However, if they decide that they want to go through with the transaction, they will exercise the option.

If the holder of an option chooses to exercise it, the seller will receive a notification, called an assignment, letting them know that the option holder is exercising their right to complete the transaction. The seller is legally obligated to fulfill the terms of the options contract.

For example, if you sell a call option on XYZ with a strike price of $40 and the buyer chooses to exercise the option, you’ll be assigned the obligation to fulfill that contract. You’ll have to buy 100 shares of XYZ at whatever the market price is, or take the shares from your own portfolio and sell them to the option holder for $40 each.

Options traders only have to worry about assignment if they sell options contracts. Those who buy options don’t have to worry about assignment because in this case, they have the power to exercise a contract, or choose not to.

The options market is huge, in that options are traded on large exchanges and you likely do not know who you’re buying contracts from or selling them to. It’s not like you sell an option to someone you know and they send you an email if they choose to exercise the contract, rather it is an organized process.

In the U.S., the Options Clearing Corporation (OCC), which is considered the options industry clearinghouse, helps to facilitate the exchange of options contracts. It guarantees a fair process of option assignments, ensuring that the obligations in the contract are fulfilled.

When an investor chooses to exercise a contract, the OCC randomly assigns the obligation to someone who sold the option being exercised. For example, if 100 people sold XYZ calls with a strike of $40, and one of those options gets exercised, the OCC will randomly assign that obligation to one of the 100 sellers.

In general, assignments are uncommon. About 7% of options get exercised, with the remaining 93% expiring. Assignment also tends to grow more common as the expiration date nears.

If you are assigned the obligation to fulfill an options contract you sold, it means you have to accept the related loss and fulfill the contract. Usually, your broker will handle the transaction on your behalf automatically.

If you’re an individual investor, you only have to worry about assignment if you’re involved in selling options. Even then, assignments aren't incredibly common. Less than 7% of options get assigned and they tend to get assigned as the option’s expiration date gets closer.

Having an option assigned does mean that you are forced to lock in a loss on an option, which can hurt. However, if you’re truly worried about assignment, you can plan to close your position at some point before the expiration date or use options strategies that don’t involve selling options that could get exercised.

The Options Industry Council. " Options Assignment FAQ: How Can I Tell When I Will Be Assigned? " Accessed Oct. 18, 2021.

- Search Search Please fill out this field.

- Options and Derivatives

- Strategy & Education

Should an Investor Hold or Exercise an Option?

Gordon Scott has been an active investor and technical analyst or 20+ years. He is a Chartered Market Technician (CMT).

:max_bytes(150000):strip_icc():format(webp)/gordonscottphoto-5bfc26c446e0fb00265b0ed4.jpg "stock assignment call option")

Yarilet Perez is an experienced multimedia journalist and fact-checker with a Master of Science in Journalism. She has worked in multiple cities covering breaking news, politics, education, and more. Her expertise is in personal finance and investing, and real estate.

:max_bytes(150000):strip_icc():format(webp)/YariletPerez-d2289cb01c3c4f2aabf79ce6057e5078.jpg "stock assignment call option")

When is it time to exercise an option contract? That's a question that investors sometimes struggle with because it's not always clear if it's the optimal time to call (buy) the shares or put (sell) the stock when holding a long call option or a long put option.