- What Is TAB

- Advisory Boards

- Business Coaching

- StratPro Leadership Transformation Program

- Strategic Leadership Tools

- Our Members

- Case Studies

- White Papers

- Business Diagnostic

The Alternative Board Blog

What is a business assessment, and when do you need one.

We’ve already explained the 5 steps in TAB’s strategic business leadership process:

- Vision - Personal and business

- SWOT analysis - Strengths, weaknesses, opportunities, threats

- Plan - Personal and business

- Make it happen - Communication, review, accountability, planning team

- Turn the wheel - continuous review and revision as needed

And we’ve already discussed the importance of having a strategic plan for your business , the kind of plan that will make you remember the big picture: why you started your business in the first place.

But while having a vision for your business and having a strategic business plan to grow it are both keys to success, how do you get from A to B? How do you even know you need a strategic plan?

That’s when a business assessment comes in handy. Business assessments are a crucial aspect of understanding what your business plan should look like, what’s working the way it should, and what isn’t.

Think of your business as a car, and a business assessment as the blueprint for its design. While you might know your vehicle’s exact make, model, and mileage, you probably can’t remember all the details about its construction, such as the exact diameter of each of its hoses. The same goes for small businesses. If you install a hose that’s not the exact fit, the car will come screeching to a halt - and in this particular analogy, there are hundreds of hoses in varying sizes.

So much happens and so many decisions are made on a monthly basis -- without a business assessment it can be incredibly difficult for business owners to remember all of the details that can make huge differences in their operations and bottom line.

We recently interviewed hundreds of small business owners about what they wish they could do differently, if they could build their companies all over again. Out of all the aspects of running a business, the entrepreneurs wish they would’ve spent more time on strategic planning. Only 2% of respondents thought that a better product would have helped their business more than a better strategy.

Want additional insight? Read 4 Step Guide to Strategic Planning now to learn more

That’s why a business assessment is so important. If you have a vision for your business but don’t know where to start when it comes to figuring out a strategic plan for growth, it’s probably time for a business assessment. From there, you can build out your strategic plan and outline specific goals, as well as outline how you’re going to achieve them.

What does “SWOT” stand for?

Different firms offer different business assessments, each with their distinct advantages, but all business assessments are fundamentally lead to a balanced SWOT analysis of the organization.

A SWOT analysis looks at internal and external factors that are helpful or harmful to your business and the way it’s run. This type of assessment is particularly interested in identifying factors in the following 4 categories:

- The strongest parts of your business model and your best selling points. The core competencies of your team and your investments.

W eaknesses

- The weakest parts of your business model and weak spots in the sales funnel. What’s lacking in your team and missing from your investments.

O pportunities

- Potential leads, investors, events, and even new target markets.

- Potential competitors, reasons investors would cut funding, or negative market developments.

At a glance, it’s easy to see where most small business owners (and most business owners in general) like to spend their time - among the tropical shade and white sands of their company’s Strengths and Opportunities.

Rare is the business owner who takes the time to sit down and honestly assess weaknesses in his business model as well as potential threats (which can be difficult to see without another pair of eyes). This is why many small businesses fail -- entrepreneurs often have a vision, but no strategic plan for growth. And they have no strategic plan because they never conducted an honest business assessment.

They thought they were doing just fine when, in reality, weaknesses were eating away at their business model and threats were looming large in their market.

When’s the right time to get a business assessment?

That’s why we offer TAB Business Diagnostic. Our tool that we developed over years of research working with thousands of business owners that lets you comprehensively identify your competitive strengths but also key gaps in your business. Think of it as an MRI for your business that compares your business to others in the same industry. Not only does it identify the gaps but it also helps you prioritize, so you’ll know what challenges and opportunities you need to focus on first.

A business assessment does not take a lot of time but the results are invaluable. The output of the assessment is fed into the SWOT process. This helps identify the key areas of the strategic plan. Taking the first step in this process will put you on a path to running your business more strategically.

No matter of the economic conditions thrown at you and your business, there are steps to help safeguard your business so that you not only survive, but thrive. Download the whitepaper to learn more here

Read our 19 Reasons You Need a Business Owner Advisory Board

Written by The Alternative Board

Subscribe to our blog.

- Sales and marketing (140)

- Strategic Planning (135)

- Business operations (128)

- People management (69)

- Time Management (52)

- tabboards (39)

- Technology (38)

- Customer Service (37)

- Entrepreneurship (35)

- company culture (27)

- Business Coaching and Peer Boards (24)

- Money management (24)

- businessleadership (23)

- employee retention (23)

- Work life balance (22)

- Family business (17)

- leadership (15)

- business strategy (14)

- communication (12)

- human resources (12)

- employee engagement (11)

- employment (11)

- strategy (8)

- businesscoaching (7)

- innovation (7)

- productivity (7)

- remote teams (7)

- adaptability (6)

- cybersecurity (6)

- professional development (6)

- salesstrategy (6)

- strategic planning (6)

- businessethics (5)

- leadership styles (5)

- marketing (5)

- peeradvisoryboards (5)

- socialmedia (5)

- branding (4)

- employeedevelopment (4)

- hiring practices (4)

- networking (4)

- supplychain (4)

- Mentorship (3)

- business vision (3)

- collaboration (3)

- culture (3)

- environment (3)

- future proof (3)

- newnormal (3)

- remote work (3)

- sustainability (3)

- work from home (3)

- worklifebalance (3)

- workplacewellness (3)

- Planning (2)

- ecofriendly (2)

- globalization (2)

- recession management (2)

- salescycle (2)

- salesprocess (2)

- #contentisking (1)

- #customerloyalty (1)

- accountability partners (1)

- artificial intelligence (1)

- blindspots (1)

- building trust (1)

- business owner (1)

- businesstrends (1)

- customer appreciation (1)

- customerengagement (1)

- data analysis (1)

- digitalpersona (1)

- financials (1)

- globaleconomy (1)

- greenmarketing (1)

- greenwashing (1)

- onlinepresence (1)

- post-covid (1)

- risk management (1)

- riskassessment (1)

- social media (1)

- talent optimization (1)

- team building (1)

- transparency (1)

Do you want additional insight?

Download our 19 Reasons Why You Need a Business Advisory Board Now!

TAB helps forward-thinking business owners grow their businesses, increase profitability and improve their lives by leveraging local business advisory boards, private business coaching and proprietary strategic services.

Quick Links

- Find a Local Board

- My TAB Login

keep in touch

- Privacy Policy

- Terms & Conditions

How to make a business plan

Table of Contents

How to make a good business plan: step-by-step guide.

A business plan is a strategic roadmap used to navigate the challenging journey of entrepreneurship. It's the foundation upon which you build a successful business.

A well-crafted business plan can help you define your vision, clarify your goals, and identify potential problems before they arise.

But where do you start? How do you create a business plan that sets you up for success?

This article will explore the step-by-step process of creating a comprehensive business plan.

What is a business plan?

A business plan is a formal document that outlines a business's objectives, strategies, and operational procedures. It typically includes the following information about a company:

Products or services

Target market

Competitors

Marketing and sales strategies

Financial plan

Management team

A business plan serves as a roadmap for a company's success and provides a blueprint for its growth and development. It helps entrepreneurs and business owners organize their ideas, evaluate the feasibility, and identify potential challenges and opportunities.

As well as serving as a guide for business owners, a business plan can attract investors and secure funding. It demonstrates the company's understanding of the market, its ability to generate revenue and profits, and its strategy for managing risks and achieving success.

Business plan vs. business model canvas

A business plan may seem similar to a business model canvas, but each document serves a different purpose.

A business model canvas is a high-level overview that helps entrepreneurs and business owners quickly test and iterate their ideas. It is often a one-page document that briefly outlines the following:

Key partnerships

Key activities

Key propositions

Customer relationships

Customer segments

Key resources

Cost structure

Revenue streams

On the other hand, a Business Plan Template provides a more in-depth analysis of a company's strategy and operations. It is typically a lengthy document and requires significant time and effort to develop.

A business model shouldn’t replace a business plan, and vice versa. Business owners should lay the foundations and visually capture the most important information with a Business Model Canvas Template . Because this is a fast and efficient way to communicate a business idea, a business model canvas is a good starting point before developing a more comprehensive business plan.

A business plan can aim to secure funding from investors or lenders, while a business model canvas communicates a business idea to potential customers or partners.

Why is a business plan important?

A business plan is crucial for any entrepreneur or business owner wanting to increase their chances of success.

Here are some of the many benefits of having a thorough business plan.

Helps to define the business goals and objectives

A business plan encourages you to think critically about your goals and objectives. Doing so lets you clearly understand what you want to achieve and how you plan to get there.

A well-defined set of goals, objectives, and key results also provides a sense of direction and purpose, which helps keep business owners focused and motivated.

Guides decision-making

A business plan requires you to consider different scenarios and potential problems that may arise in your business. This awareness allows you to devise strategies to deal with these issues and avoid pitfalls.

With a clear plan, entrepreneurs can make informed decisions aligning with their overall business goals and objectives. This helps reduce the risk of making costly mistakes and ensures they make decisions with long-term success in mind.

Attracts investors and secures funding

Investors and lenders often require a business plan before considering investing in your business. A document that outlines the company's goals, objectives, and financial forecasts can help instill confidence in potential investors and lenders.

A well-written business plan demonstrates that you have thoroughly thought through your business idea and have a solid plan for success.

Identifies potential challenges and risks

A business plan requires entrepreneurs to consider potential challenges and risks that could impact their business. For example:

Is there enough demand for my product or service?

Will I have enough capital to start my business?

Is the market oversaturated with too many competitors?

What will happen if my marketing strategy is ineffective?

By identifying these potential challenges, entrepreneurs can develop strategies to mitigate risks and overcome challenges. This can reduce the likelihood of costly mistakes and ensure the business is well-positioned to take on any challenges.

Provides a basis for measuring success

A business plan serves as a framework for measuring success by providing clear goals and financial projections . Entrepreneurs can regularly refer to the original business plan as a benchmark to measure progress. By comparing the current business position to initial forecasts, business owners can answer questions such as:

Are we where we want to be at this point?

Did we achieve our goals?

If not, why not, and what do we need to do?

After assessing whether the business is meeting its objectives or falling short, business owners can adjust their strategies as needed.

How to make a business plan step by step

The steps below will guide you through the process of creating a business plan and what key components you need to include.

1. Create an executive summary

Start with a brief overview of your entire plan. The executive summary should cover your business plan's main points and key takeaways.

Keep your executive summary concise and clear with the Executive Summary Template . The simple design helps readers understand the crux of your business plan without reading the entire document.

2. Write your company description

Provide a detailed explanation of your company. Include information on what your company does, the mission statement, and your vision for the future.

Provide additional background information on the history of your company, the founders, and any notable achievements or milestones.

3. Conduct a market analysis

Conduct an in-depth analysis of your industry, competitors, and target market. This is best done with a SWOT analysis to identify your strengths, weaknesses, opportunities, and threats. Next, identify your target market's needs, demographics, and behaviors.

Use the Competitive Analysis Template to brainstorm answers to simple questions like:

What does the current market look like?

Who are your competitors?

What are they offering?

What will give you a competitive advantage?

Who is your target market?

What are they looking for and why?

How will your product or service satisfy a need?

These questions should give you valuable insights into the current market and where your business stands.

4. Describe your products and services

Provide detailed information about your products and services. This includes pricing information, product features, and any unique selling points.

Use the Product/Market Fit Template to explain how your products meet the needs of your target market. Describe what sets them apart from the competition.

5. Design a marketing and sales strategy

Outline how you plan to promote and sell your products. Your marketing strategy and sales strategy should include information about your:

Pricing strategy

Advertising and promotional tactics

Sales channels

The Go to Market Strategy Template is a great way to visually map how you plan to launch your product or service in a new or existing market.

6. Determine budget and financial projections

Document detailed information on your business’ finances. Describe the current financial position of the company and how you expect the finances to play out.

Some details to include in this section are:

Startup costs

Revenue projections

Profit and loss statement

Funding you have received or plan to receive

Strategy for raising funds

7. Set the organization and management structure

Define how your company is structured and who will be responsible for each aspect of the business. Use the Business Organizational Chart Template to visually map the company’s teams, roles, and hierarchy.

As well as the organization and management structure, discuss the legal structure of your business. Clarify whether your business is a corporation, partnership, sole proprietorship, or LLC.

8. Make an action plan

At this point in your business plan, you’ve described what you’re aiming for. But how are you going to get there? The Action Plan Template describes the following steps to move your business plan forward. Outline the next steps you plan to take to bring your business plan to fruition.

Types of business plans

Several types of business plans cater to different purposes and stages of a company's lifecycle. Here are some of the most common types of business plans.

Startup business plan

A startup business plan is typically an entrepreneur's first business plan. This document helps entrepreneurs articulate their business idea when starting a new business.

Not sure how to make a business plan for a startup? It’s pretty similar to a regular business plan, except the primary purpose of a startup business plan is to convince investors to provide funding for the business. A startup business plan also outlines the potential target market, product/service offering, marketing plan, and financial projections.

Strategic business plan

A strategic business plan is a long-term plan that outlines a company's overall strategy, objectives, and tactics. This type of strategic plan focuses on the big picture and helps business owners set goals and priorities and measure progress.

The primary purpose of a strategic business plan is to provide direction and guidance to the company's management team and stakeholders. The plan typically covers a period of three to five years.

Operational business plan

An operational business plan is a detailed document that outlines the day-to-day operations of a business. It focuses on the specific activities and processes required to run the business, such as:

Organizational structure

Staffing plan

Production plan

Quality control

Inventory management

Supply chain

The primary purpose of an operational business plan is to ensure that the business runs efficiently and effectively. It helps business owners manage their resources, track their performance, and identify areas for improvement.

Growth-business plan

A growth-business plan is a strategic plan that outlines how a company plans to expand its business. It helps business owners identify new market opportunities and increase revenue and profitability. The primary purpose of a growth-business plan is to provide a roadmap for the company's expansion and growth.

The 3 Horizons of Growth Template is a great tool to identify new areas of growth. This framework categorizes growth opportunities into three categories: Horizon 1 (core business), Horizon 2 (emerging business), and Horizon 3 (potential business).

One-page business plan

A one-page business plan is a condensed version of a full business plan that focuses on the most critical aspects of a business. It’s a great tool for entrepreneurs who want to quickly communicate their business idea to potential investors, partners, or employees.

A one-page business plan typically includes sections such as business concept, value proposition, revenue streams, and cost structure.

Best practices for how to make a good business plan

Here are some additional tips for creating a business plan:

Use a template

A template can help you organize your thoughts and effectively communicate your business ideas and strategies. Starting with a template can also save you time and effort when formatting your plan.

Miro’s extensive library of customizable templates includes all the necessary sections for a comprehensive business plan. With our templates, you can confidently present your business plans to stakeholders and investors.

Be practical

Avoid overestimating revenue projections or underestimating expenses. Your business plan should be grounded in practical realities like your budget, resources, and capabilities.

Be specific

Provide as much detail as possible in your business plan. A specific plan is easier to execute because it provides clear guidance on what needs to be done and how. Without specific details, your plan may be too broad or vague, making it difficult to know where to start or how to measure success.

Be thorough with your research

Conduct thorough research to fully understand the market, your competitors, and your target audience . By conducting thorough research, you can identify potential risks and challenges your business may face and develop strategies to mitigate them.

Get input from others

It can be easy to become overly focused on your vision and ideas, leading to tunnel vision and a lack of objectivity. By seeking input from others, you can identify potential opportunities you may have overlooked.

Review and revise regularly

A business plan is a living document. You should update it regularly to reflect market, industry, and business changes. Set aside time for regular reviews and revisions to ensure your plan remains relevant and effective.

Create a winning business plan to chart your path to success

Starting or growing a business can be challenging, but it doesn't have to be. Whether you're a seasoned entrepreneur or just starting, a well-written business plan can make or break your business’ success.

The purpose of a business plan is more than just to secure funding and attract investors. It also serves as a roadmap for achieving your business goals and realizing your vision. With the right mindset, tools, and strategies, you can develop a visually appealing, persuasive business plan.

Ready to make an effective business plan that works for you? Check out our library of ready-made strategy and planning templates and chart your path to success.

Get on board in seconds

Join thousands of teams using Miro to do their best work yet.

Small Business Trends

How to create a business plan: examples & free template.

Whether you’re a seasoned entrepreneur or launching your very first startup, the guide will give you the insights, tools, and confidence you need to create a solid foundation for your business.

Table of Contents

How to Write a Business Plan

Executive summary.

It’s crucial to include a clear mission statement, a brief description of your primary products or services, an overview of your target market, and key financial projections or achievements.

Our target market includes environmentally conscious consumers and businesses seeking to reduce their carbon footprint. We project a 200% increase in revenue within the first three years of operation.

Overview and Business Objectives

Example: EcoTech’s primary objective is to become a market leader in sustainable technology products within the next five years. Our key objectives include:

Company Description

Example: EcoTech is committed to developing cutting-edge sustainable technology products that benefit both the environment and our customers. Our unique combination of innovative solutions and eco-friendly design sets us apart from the competition. We envision a future where technology and sustainability go hand in hand, leading to a greener planet.

Define Your Target Market

Market analysis.

The Market Analysis section requires thorough research and a keen understanding of the industry. It involves examining the current trends within your industry, understanding the needs and preferences of your customers, and analyzing the strengths and weaknesses of your competitors.

Our research indicates a gap in the market for high-quality, innovative eco-friendly technology products that cater to both individual and business clients.

SWOT Analysis

Including a SWOT analysis demonstrates to stakeholders that you have a balanced and realistic understanding of your business in its operational context.

Competitive Analysis

Organization and management team.

Provide an overview of your company’s organizational structure, including key roles and responsibilities. Introduce your management team, highlighting their expertise and experience to demonstrate that your team is capable of executing the business plan successfully.

Products and Services Offered

This section should emphasize the value you provide to customers, demonstrating that your business has a deep understanding of customer needs and is well-positioned to deliver innovative solutions that address those needs and set your company apart from competitors.

Marketing and Sales Strategy

Discuss how these marketing and sales efforts will work together to attract and retain customers, generate leads, and ultimately contribute to achieving your business’s revenue goals.

Logistics and Operations Plan

Inventory control is another crucial aspect, where you explain strategies for inventory management to ensure efficiency and reduce wastage. The section should also describe your production processes, emphasizing scalability and adaptability to meet changing market demands.

We also prioritize efficient distribution through various channels, including online platforms and retail partners, to deliver products to our customers in a timely manner.

Financial Projections Plan

This forward-looking financial plan is crucial for demonstrating that you have a firm grasp of the financial nuances of your business and are prepared to manage its financial health effectively.

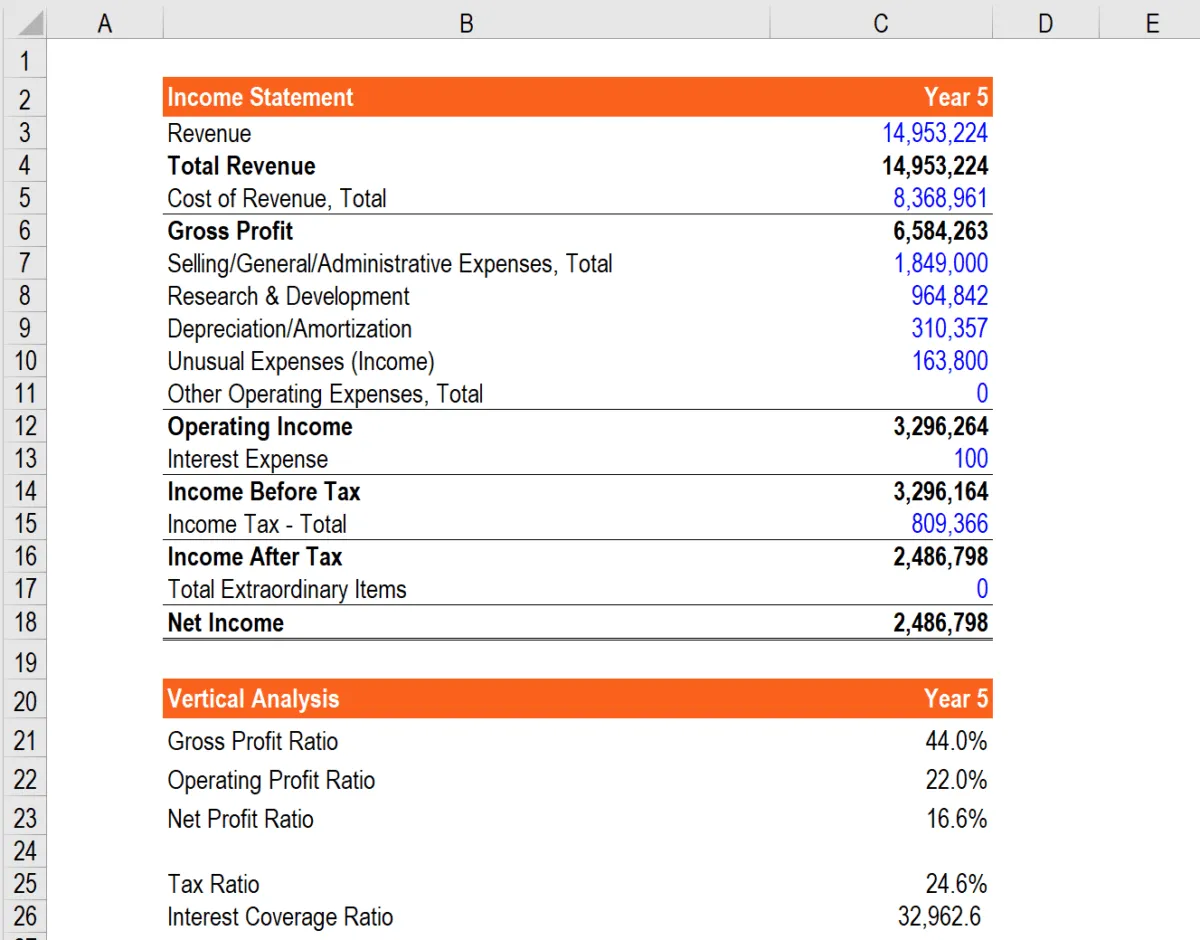

Income Statement

Cash flow statement.

A cash flow statement is a crucial part of a financial business plan that shows the inflows and outflows of cash within your business. It helps you monitor your company’s liquidity, ensuring you have enough cash on hand to cover operating expenses, pay debts, and invest in growth opportunities.

| Section | Description | Example |

|---|---|---|

| Executive Summary | Brief overview of the business plan | Overview of EcoTech and its mission |

| Overview & Objectives | Outline of company's goals and strategies | Market leadership in sustainable technology |

| Company Description | Detailed explanation of the company and its unique selling proposition | EcoTech's history, mission, and vision |

| Target Market | Description of ideal customers and their needs | Environmentally conscious consumers and businesses |

| Market Analysis | Examination of industry trends, customer needs, and competitors | Trends in eco-friendly technology market |

| SWOT Analysis | Evaluation of Strengths, Weaknesses, Opportunities, and Threats | Strengths and weaknesses of EcoTech |

| Competitive Analysis | In-depth analysis of competitors and their strategies | Analysis of GreenTech and EarthSolutions |

| Organization & Management | Overview of the company's structure and management team | Key roles and team members at EcoTech |

| Products & Services | Description of offerings and their unique features | Energy-efficient lighting solutions, solar chargers |

| Marketing & Sales | Outline of marketing channels and sales strategies | Digital advertising, content marketing, influencer partnerships |

| Logistics & Operations | Details about daily operations, supply chain, inventory, and quality control | Partnerships with manufacturers, quality control |

| Financial Projections | Forecast of revenue, expenses, and profit for the next 3-5 years | Projected growth in revenue and net profit |

| Income Statement | Summary of company's revenues and expenses over a specified period | Revenue, Cost of Goods Sold, Gross Profit, Net Income |

| Cash Flow Statement | Overview of cash inflows and outflows within the business | Net Cash from Operating Activities, Investing Activities, Financing Activities |

Tips on Writing a Business Plan

4. Focus on your unique selling proposition (USP): Clearly articulate what sets your business apart from the competition. Emphasize your USP throughout your business plan to showcase your company’s value and potential for success.

FREE Business Plan Template

To help you get started on your business plan, we have created a template that includes all the essential components discussed in the “How to Write a Business Plan” section. This easy-to-use template will guide you through each step of the process, ensuring you don’t miss any critical details.

What is a Business Plan?

Why you should write a business plan.

Understanding the importance of a business plan in today’s competitive environment is crucial for entrepreneurs and business owners. Here are five compelling reasons to write a business plan:

What are the Different Types of Business Plans?

| Type of Business Plan | Purpose | Key Components | Target Audience |

|---|---|---|---|

| Startup Business Plan | Outlines the company's mission, objectives, target market, competition, marketing strategies, and financial projections. | Mission Statement, Company Description, Market Analysis, Competitive Analysis, Organizational Structure, Marketing and Sales Strategy, Financial Projections. | Entrepreneurs, Investors |

| Internal Business Plan | Serves as a management tool for guiding the company's growth, evaluating its progress, and ensuring that all departments are aligned with the overall vision. | Strategies, Milestones, Deadlines, Resource Allocation. | Internal Team Members |

| Strategic Business Plan | Outlines long-term goals and the steps to achieve them. | SWOT Analysis, Market Research, Competitive Analysis, Long-Term Goals. | Executives, Managers, Investors |

| Feasibility Business Plan | Assesses the viability of a business idea. | Market Demand, Competition, Financial Projections, Potential Obstacles. | Entrepreneurs, Investors |

| Growth Business Plan | Focuses on strategies for scaling up an existing business. | Market Analysis, New Product/Service Offerings, Financial Projections. | Business Owners, Investors |

| Operational Business Plan | Outlines the company's day-to-day operations. | Processes, Procedures, Organizational Structure. | Managers, Employees |

| Lean Business Plan | A simplified, agile version of a traditional plan, focusing on key elements. | Value Proposition, Customer Segments, Revenue Streams, Cost Structure. | Entrepreneurs, Startups |

| One-Page Business Plan | A concise summary of your company's key objectives, strategies, and milestones. | Key Objectives, Strategies, Milestones. | Entrepreneurs, Investors, Partners |

| Nonprofit Business Plan | Outlines the mission, goals, target audience, fundraising strategies, and budget allocation for nonprofit organizations. | Mission Statement, Goals, Target Audience, Fundraising Strategies, Budget. | Nonprofit Leaders, Board Members, Donors |

| Franchise Business Plan | Focuses on the franchisor's requirements, as well as the franchisee's goals, strategies, and financial projections. | Franchise Agreement, Brand Standards, Marketing Efforts, Operational Procedures, Financial Projections. | Franchisors, Franchisees, Investors |

Using Business Plan Software

Upmetrics provides a simple and intuitive platform for creating a well-structured business plan. It features customizable templates, financial forecasting tools, and collaboration capabilities, allowing you to work with team members and advisors. Upmetrics also offers a library of resources to guide you through the business planning process.

| Software | Key Features | User Interface | Additional Features |

|---|---|---|---|

| LivePlan | Over 500 sample plans, financial forecasting tools, progress tracking against KPIs | User-friendly, visually appealing | Allows creation of professional-looking business plans |

| Upmetrics | Customizable templates, financial forecasting tools, collaboration capabilities | Simple and intuitive | Provides a resource library for business planning |

| Bizplan | Drag-and-drop builder, modular sections, financial forecasting tools, progress tracking | Simple, visually engaging | Designed to simplify the business planning process |

| Enloop | Industry-specific templates, financial forecasting tools, automatic business plan generation, unique performance score | Robust, user-friendly | Offers a free version, making it accessible for businesses on a budget |

| Tarkenton GoSmallBiz | Guided business plan builder, customizable templates, financial projection tools | User-friendly | Offers CRM tools, legal document templates, and additional resources for small businesses |

Business Plan FAQs

What is a good business plan.

A good business plan is a well-researched, clear, and concise document that outlines a company’s goals, strategies, target market, competitive advantages, and financial projections. It should be adaptable to change and provide a roadmap for achieving success.

What are the 3 main purposes of a business plan?

Can i write a business plan by myself, is it possible to create a one-page business plan.

Yes, a one-page business plan is a condensed version that highlights the most essential elements, including the company’s mission, target market, unique selling proposition, and financial goals.

How long should a business plan be?

What is a business plan outline, what are the 5 most common business plan mistakes, what questions should be asked in a business plan.

A business plan should address questions such as: What problem does the business solve? Who is the specific target market ? What is the unique selling proposition? What are the company’s objectives? How will it achieve those objectives?

What’s the difference between a business plan and a strategic plan?

How is business planning for a nonprofit different.

Want to create or adapt books like this? Learn more about how Pressbooks supports open publishing practices.

2 Developing a Business Plan

Learning Objectives

After completing this chapter, you will be able to

- Describe the purposes for business planning

- Describe common business planning principles

- Explain common business plan development guidelines and tools

- List and explain the elements of the business plan development process

- Explain the purposes of each element of the business plan development process

- Explain how applying the business plan development process can aid in developing a business plan that will meet entrepreneurs’ goals

This chapter describes the purposes, principles, and the general concepts and tools for business planning, and the process for developing a business plan.

Purposes for Developing Business Plans

Business plans are developed for both internal and external purposes. Internally, entrepreneurs develop business plans to help put the pieces of their business together. Externally, the most common purpose is to raise capital.

Internal Purposes

As the road map for a business’s development, the business plan

- Defines the vision for the company

- Establishes the company’s strategy

- Describes how the strategy will be implemented

- Provides a framework for analysis of key issues

- Provides a plan for the development of the business

- Helps the entrepreneur develop and measure critical success factors

- Helps the entrepreneur to be realistic and test theories

External Purposes

The business plan provides the most complete source of information for valuation of the business. Thus, it is often the main method of describing a company to external audiences such as potential sources for financing and key personnel being recruited. It should assist outside parties to understand the current status of the company, its opportunities, and its needs for resources such as capital and personnel.

Business Plan Development Principles [1]

Hindle and Mainprize suggested that business plan writers must strive to effectively communicate their expectations about the nature of an uncertain future and to project credibility. The liabilities of newness make communicating the expected future of new ventures much more difficult than for existing businesses. Consequently, business plan writers should adhere to five specific communication principles .

First, business plans must be written to meet the expectations of targeted readers in terms of what they need to know to support the proposed business. They should also lay out the milestones that investors or other targeted readers need to know. Finally, writers must clearly outline the opportunity , the context within the proposed venture will operate (internal and external environment), and the business model.

There are also five business plan credibility principles that writers should consider. Business plan writers should build and establish their credibility by highlighting important and relevant information about the venture team . Writers need to elaborate on the plans they outline in their document so that targeted readers have the information they need to assess the plan’s credibility. To build and establish credibility, they must integrate scenarios to show that the entrepreneur has made realistic assumptions and has effectively anticipated what the future holds for their proposed venture. Writers need to provide comprehensive and realistic financial links between all relevant components of the plan. Finally, they must outline the deal , or the value that targeted readers should expect to derive from their involvement with the venture. [2]

General Guidelines for Developing Business Plans

Many businesses must have a business plan to achieve their goals. Using a standard format helps the reader understand that the you have thought everything through, and that the returns justify the risk. The following are some basic guidelines for business plan development.

As You Write Your Business Plan

- If appropriate, include nice, catchy, professional graphics on your title page to make it appealing to targeted readers, but don’t go overboard.

- Bind your document so readers can go through it easily without it falling apart. You might use a three-ring binder, coil binding, or a similar method. Make sure the binding method you use does not obscure the information next to where it is bound.

- Make certain all of your pages are ordered and numbered correctly.

- The usual business plan convention is to number all major sections and subsections within your plan using the format as follows:

1. First main heading

1.1 First subheading under the first main heading

1.1.1. First sub-subheading under the first subheading

2. Second main heading

2.1 First subheading under the second main heading

Use the styles and references features in Word to automatically number and format your section titles and to generate your table of contents. Be sure that the last thing you do before printing your document is update your automatic numbering and automatically generated tables. If you fail to do this, your numbering may be incorrect.

5. Prior to submitting your plan, be 100% certain each of the following requirements are met:

- Everything must be completely integrated. The written part must say exactly the same thing as the financial part.

- All financial statements must be completely linked and valid. Make sure all of your balance sheets balance.

- Everything must be correct. There should be NO spelling, grammar, sentence structure, referencing, or calculation errors.

- Your document must be well organized and formatted. The layout you choose should make the document easy to read and comprehend. All of your diagrams, charts, statements, and other additions should be easy to find and be located in the parts of the plan best suited to them.

- In some cases it can strengthen your business plan to show some information in both text and table or figure formats. You should avoid unnecessary repetition , however, as it is usually unnecessary—and even damaging—to state the same thing more than once.

- You should include all the information necessary for readers to understand everything in your document.

- The terms you use in your plan should be clear and consistent. For example, the following statement in a business plan would leave a reader completely confused: “There is a shortage of 100,000 units with competitors currently producing 25,000. We can help fill this huge gap in demand with our capacity to produce 5,000 units.” This statement might mean there is a total shortage of 100,000 units, but competitors are filling this gap by producing 25,000 per year; in which case there will only be a shortage for four years. However, it could mean that the annual shortage is 100,000 units and only 25,000 are produced each year, in which case the total shortage is very high and is growing each year.

- You must always provide the complete perspective by indicating the appropriate time frame, currency, size, or other measurement.

- If you use a percentage figure, you must indicate to what it refers—otherwise the number is meaningless to a reader.

- If your plan includes an international element, you must indicate in which currency or currencies the costs, revenues, prices, or other values are quoted. This can be solved by indicating up-front in the document in which currency all values will be quoted. Another option is to indicate each time which currency is being used, and sometimes you might want to indicate the value in more than one currency. Of course, you will need to assess the exchange rate risk to which you will be exposed and describe this in your document.

6. Ensure credibility is both established and maintained. [3]

- If a statement presents something as a fact when this fact is not generally known, always indicate the source. Unsupported statements damage credibility.

- Be specific. A business plan is simply not of value if it uses vague references to high demand, carefully set prices, and other weak phrasing. It must show hard numbers (properly referenced, of course), actual prices, and real data acquired through proper research. This is the only way to ensure your plan is considered credible.

- Your strategies must be integrated. For example, your pricing strategy must complement and mesh perfectly with your product/service strategy, distribution strategy, and promotions strategy. For example, you probably shouldn’t promote your product as a premium product if you plan to charge lower-than-market prices for it.

7. Before finalizing your business plan, re-read each section to evaluate whether it will appeal to your targeted readers.

Useful Resources for Business Planning

- Financial Performance Data : Innovation, Science and Economic Development Canada

- BizPal for accessing licensing and other needs

- Canada Revenue Agency for CRA asset classifications

- Canadian Company Capabilities database to use to find suppliers and buyers

- Merx for finding possible Canadian Government contracts

- The Conference Board of Canada

- Bank of Canada

- Scotia Bank

- Bank of Montreal

- Business Loan Calculator

Library Resources

NSCC Library – Business Databases [journals and other resources]

Employee compensation calculators

- Salary Data & Career Research Center – Canada

Existing business plans

The Word and Excel templates in this book

- Business Plan Template (Word)

- Business Plan Template (Excel)

Business Plan Development Tools

Credibility and communication.

According to Hindle and Mainprize, strong business plans effectively communicate the necessary information to the targeted readers while also establishing the credibility of the plan and the entrepreneur. [4] The Credibility and Communication Meter icon is used throughout this book to highlight where and how business plan writers can improve the quality of the information and enhance their and their plan’s credibility.

| Credibility and Communication Meter |

Use the following tools to improve the information in and credibility of your plans:

The Ratchet Effect

A ratchet is a tool that most of us are familiar with. It is useful because it helps its user accomplish something with each effort expended while guarding against losing past advancements.

With each word, sentence, paragraph, heading, chart, figure, and table you include in your final business plan, the ratchet should move ahead a notch because you achieve two important things.

First, only needed and relevant information is included.

Second, your additions build credibility in a relevant way.

Apply the ratchet effect by making sure that each and every sentence and paragraph conveys needed and relevant information that adds to your and your plan’s credibility. Use the following principles: Rarely—and only if it truly needs to be said again—repeat something that you have already said in your plan.

Avoid using killer phrases, like “there is no competition for our product” or “our product will sell itself, so we will not need to advertise it.” Any savvy reader will understand that these kinds of statements are naive and demonstrate a lack of understanding about how the market and other real-life factors actually work.

Avoid contradicting yourself. Make sure that what is said in the written part of your plan completely syncs with what is said in the other parts of your plan. Likewise, ensure that what you include in the financial parts of your plan is completely in sync with what is said the written part.

The Magic Formula

Apply the following magic formula throughout your write your plan.

- …consideration X affects my business because…

- …consideration X is subject to this trend into the future…

- …which means that we have decided to do this…(or) will implement this strategy…in response to how the expected trends for consideration X will affect my business

Here is an example of how you can use the magic formula to develop part of the pricing strategy in the marketing plan part of your business plan: We expect that our expenses to run our business will rise with the rate of inflation, which means that we must plan to increase the prices on our products to establish and maintain our profitability. The Bank of Canada (201x) has projected that the general inflation rate in <the city in which my business will operate> will be 3.0% in 201x, 3.5% in 201y, and 4.0% in 201z. In our projected financial statements, therefore, we have inflated both our expenses and our prices by those rates in those years.

Context and Framing

You must provide the right context when you describe situations, strategies, and other components of your plan. Business plan readers should never be left to guess why you indicate in a business plan that you will do something. Proper context is needed to help you frame the information you present.

When you frame the stories you tell correctly, the ratchet effect will happen and your plan will be stronger. One example of effective framing is when you, as the writer of the plan and the entrepreneur, clearly indicate how your education, expertise, relevant experiences, and network of contacts will make up for any lack of direct experience you have in running this particular kind of business. An example of ineffective framing is when you indicate that you lack experience with this type of business, or when you fail to specify how and why your levels of experience will affect the business’s development.

Prioritizing Problems

Don’t get hung up on something that doesn’t need an immediate solution. Instead, flag it for future consideration and move on. When you return to re-address the issue, it might no longer be a problem or you might have by then figured out a solution.

Process for Developing Business Plans

The business plan development process described next has been extensively tested with entrepreneurship students and has proven to provide the guidance entrepreneurs need to develop a business plan appropriate for their needs: a high power business plan .

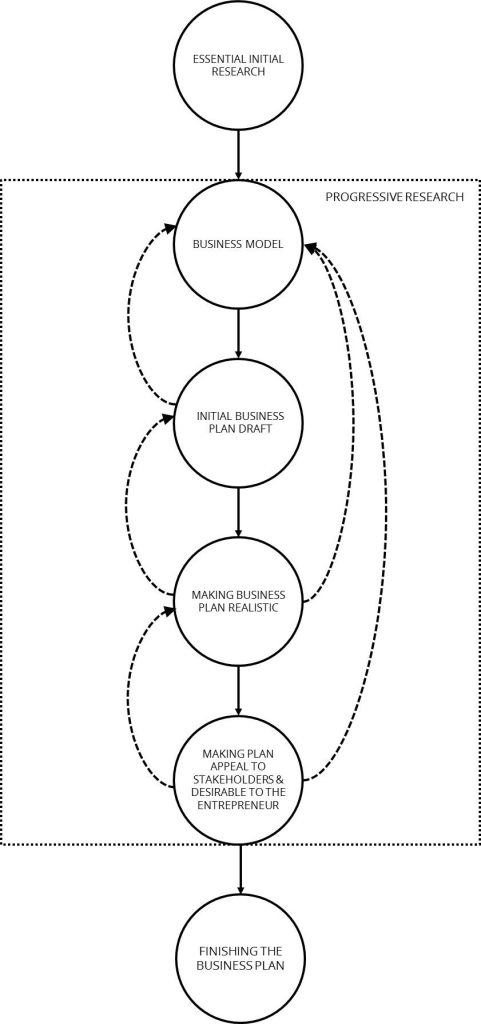

Developing a high power business plan has six stages, which can be compared to a process for hosting a dinner for a few friends. A host hoping to make a good impression with their anticipated guests might analyze the situation at multiple levels to collect data on new alternatives for healthy ingredients, what ingredients have the best prices and are most readily available at certain times of year, the new trends in party appetizers, what food allergies the expected guests might have, possible party themes, and so on. This analysis is the Essential Initial Research stage.

In the Business Model stage, the host might construct a menu of items to include with the meal along with a list of decorations to order, music to play, and costume themes to suggest to the guests. The mix of these kinds of elements chosen by the host will aid in the success of the party.

The Initial Business Plan Draft stage is where the host rolls up their sleeves and begins to make some of the food items, puts up some of the decorations, and generally gets everything started for the party.

During this stage, the host will begin to realize that some plans are not feasible and that changes are needed. The required changes might be substantial, like the need to postpone the entire party and ultimately start over in a few months, and others might be less drastic, like the need to change the menu when an invited guest indicates that they can’t eat food containing gluten. These changes are incorporated into the plan during the Making the Business Plan Realistic stage to make it realistic and feasible.

The Making the Plan Appeal to Stakeholders and Desirable to the Entrepreneur stage involves further changes to the party plan to make it more appealing to both the invited guests and to make it a fun experience for the host. For example, the host might learn that some of the single guests would like to bring dates and others might need to be able to bring their children to be able to attend. The host might be able to accommodate those desires or needs in ways that will also make the party more fun for them—maybe by accepting some guests’ offers to bring food or games, or maybe hiring a babysitter to entertain and look after the children.

The final stage— Finishing the Business Plan— involves the host putting all of the final touches in place for the party in preparation for the arrival of the guests.

Essential Initial Research

A business plan writer should analyze the environment in which they anticipate operating at each of the levels of analysis: Societal , Industry , Market , and Firm . This stage of planning is called the Essential Initial Research stage, and it is a necessary first step to better understand the trends that will affect their business and the decisions they must make to lay the groundwork for, which will improve their potential for success.

In some cases, much of this research should be included in the developing business plan as its own separate section to help show readers that there is a market need for the business being considered and that it stands a good chance of being successful.

In other cases, a business plan will be stronger when the components of the research are distributed throughout the business plan to provide support for the outlined plans and strategies outlined. For example, the industry- or market-level research might outline the pricing strategies used by identified competitors, which might be best placed in the Pricing Strategy part of the business plan to support the decision made to employ a particular pricing strategy.

Business Model

Inherent in any business plan is a description of the Business Model chosen by the entrepreneur as the one that they feel will best ensure success. Based upon their analysis from the Essential Initial Research stage, an entrepreneur should determine how each element of their business model—including their revenue streams, cost structure, customer segments, value propositions, key activities, key partners, and so on—might fit together to improve the potential success of their business venture (see Chapter 3 – Business Models ).

For some types of ventures, at this stage an entrepreneur might launch a lean start-up (see the “Lean Start-up” section in Chapter 2 – Essential Initial Research ) and grow their business by continually pivoting, or constantly adjusting their business model in response to the real-time signals they get from the markets’ reactions to their business operations. In many cases, however, an entrepreneur will require a business plan. In those cases, their initial business model will provide the basis for that plan.

Of course, throughout this and all of the stages in this process, the entrepreneur should seek to continually gather information and adjust the plans in response to the new knowledge they gather. As shown in Figure 1 by its enclosure in the Progressive Research box, the business plan developer might need to conduct further research before finishing the business model and moving on to the initial business plan draft.

Initial Business Plan Draft

The Initial Business Plan Draft stage involves taking the knowledge and ideas developed during the first two stages and organizing them into a business plan format. Many entrepreneurs prefer to create a full draft of the business plan with all of the sections, including the front part with the business description, vision, mission, values, value proposition statement, preliminary set of goals, and possibly even a table of contents and lists of tables and figures all set up using the software features enabling their automatic generation. Writing all of the operations, human resources, marketing, and financial plans as part of the first draft ensures that all of these parts can be appropriately and necessarily integrated. The business plan will tell the story of a planned business startup in two ways: 1) by using primarily words along with some charts and graphs in the operations, human resources, and marketing plans and 2) through the financial plan. Both must tell the same story.

The feedback loop shown in Figure 1 demonstrates that the business developer may need to review the business model. Additionally, as shown by its enclosure in the Progressive Research box, the business plan developer might need to conduct further research before finishing the Initial Business Plan Draft stage and moving on to the Making Business Plan Realistic stage.

Making Business Plan Realistic

The first draft of a business plan will almost never be realistic. As the entrepreneur writes the plan, it will necessarily change as new information is gathered. Another factor that usually renders the first draft unrealistic is the difficulty in making certain that the written part—in the front part of the plan along with the operations, human resources, and marketing plans—tells the exact same story as the financial part does. This stage of work involves making the necessary adjustments to the plan to make it as realistic as possible.

The Making Business Plan Realistic stage has two possible feedback loops. The first means going back to the Initial Business Plan Draft stage if the initial business plan needs to be significantly changed before it is possible to adjust it so that it is realistic. The second feedback loop circles back to the Business Model stage if the business developer needs to rethink the business model. As shown in Figure 1 by its enclosure in the Progressive Research box, the business plan developer might need to conduct further research before finishing the Making Business Plan Realistic stage and moving on to the Making Plan Appeal to Stakeholders stage.

Making Plan Appeal to Stakeholders and Desirable to the Entrepreneur

A business plan can be realistic without appealing to potential investors and other external stakeholders, like employees, suppliers, and needed business partners. It might also be realistic (and possibly appealing to stakeholders) without being desirable to the entrepreneur. During this stage, the entrepreneur will keep the business plan realistic as they adjust plans to appeal to potential investors, stakeholders, and themselves.

If, for example, investors will be required to finance the business’s start, some adjustments might need to be relatively extensive to appeal to potential investors’ needs for an exit strategy from the business, to accommodate the rate of return they expect from their investments, and to convince them that the entrepreneur can accomplish all that is promised in the plan. In this case, and in others, the entrepreneur will also need to get what they want out of the business to make it worthwhile for them to start and run it. So, this stage of adjustments to the developing business plan might be fairly extensive, and they must be informed by a superior knowledge of what targeted investors need from a business proposal before they will invest. They also need to be informed by a clear set of goals that will make the venture worthwhile for the entrepreneur to pursue.

The caution with this stage is to balance the need to make realistic plans with the desire to meet the entrepreneur’s goals while avoiding becoming discouraged enough to drop the idea of pursuing the business idea . If an entrepreneur is convinced that the proposed venture will satisfy a valid market need, there is often a way to assemble the financing required to start and operate the business while also meeting the entrepreneur’s most important goals. To do so, however, might require significant changes to the business model.

One of the feedback loops shown in Figure 1 indicates that the business plan writer might need to adjust the draft business plan while ensuring that it is still realistic before it can be made appealing to the targeted stakeholders and desirable to the entrepreneur. The second feedback loop indicates that it might be necessary to go all the way back to the Business Model stage to re-establish the framework and plans needed to develop a realistic, appealing, and desirable business plan. Additionally, this stage’s enclosure in the Progressive Research box suggests that the business plan developer might need to conduct further research.

Finishing the Business Plan

The final stage involves putting the important finishing touches on the business plan so that it will present well to potential investors and others. This involves making sure that the math and links between the written and financial parts are accurate. It involves ensuring that all the needed corrections are made to the spelling, grammar, and formatting. The final set of goals should be written to appeal to the target readers and to reflect what the business plan says. An executive summary should be written and included as a final step.

Chapter Summary

This chapter described the internal and external purposes for business planning. It also explained how business plans must effectively communicate while establishing and building credibility for both the entrepreneur and the venture. The general guidelines for business planning were covered as were some important business planning tools. The chapter concluded with descriptions of the stages of the business development process for effective business planning.

- Hindle, K., & Mainprize, B. (2006). A systematic approach to writing and rating entrepreneurial business plans. The Journal of Private Equity, 9(3), 7-23. ↵

- Ibid. ↵

Business Plan Development Guide Copyright © 2023 by Lee A. Swanson is licensed under a Creative Commons Attribution-ShareAlike 4.0 International License , except where otherwise noted.

Share This Book

Do This One Thing Before You Write Your Business Plan

Noah Parsons

6 min. read

Updated May 10, 2024

So, you’ve been asked to write a business plan. It’s likely that your mind is filled with images of long documents, bad memories of writing term papers, and worries about doing market research and creating financial forecasts.

Take a deep breath.

It doesn’t have to be that way. Today, I’m going to walk you through an easier way to get your business plan started, and show you how to develop a winning strategy.

Start with why you’re writing a business plan

But first, let’s talk about why you’re writing a business plan .

There are a lot of reasons why writing a business plan is important . Most businesses start the planning process because they are applying for a loan or seeking funding from investors .

But, beyond needing to develop a plan that will impress the bank or your investors, you want to build a solid company. You want to develop a sound strategy that will help your business grow and be successful.

Unfortunately, while traditional business plans will help you develop strategy, they have several drawbacks.

Traditional business plans take too long to write, they’re rarely updated, and they are time-consuming to read.

Now, there may be a point in your business career that you will need to deliver a formal business plan to a bank, investors, or other business partners. But, until that point, I recommend that you start your planning with a simpler process— a one-page plan —that will help you develop your business strategy.

Building a one-page plan takes less than 20 minutes . You can even build several of them in an afternoon to try out different business ideas.

A Lean Plan forces you to distill your ideas for your business into the core of your strategy. As planning expert Tim Berry says, “a good strategy is about what you’re not doing.”

And, once you have nailed down your business strategy, you can expand on it with a longer business plan document that fleshes out the details of your plan.

What to include:

Your one-page plan is a very high-level overview of your business. Each section should only be a few bullet points, so you should be able to complete an initial draft of your plan in 20 minutes or less.

Brought to you by

Create a professional business plan

Using ai and step-by-step instructions.

Secure funding

Validate ideas

Build a strategy

- 1. Your identity

What sets your business apart from others? What’s your focus? For example, a bike shop’s identity might be, “High-quality biking gear for families and regular people, not just for gearheads.” With this identity, this bike shop has focus. It describes who they are and what they are trying to do. Ideally, you should be able to describe your identity in one or two short sentences.

- 2. The problem you are solving

How are you helping your customers? What problem will they go to you to solve? Don’t think that your business doesn’t solve a problem; for example, a new restaurant would fill a need for a particular type of cuisine or a certain atmosphere that is not currently available in a certain neighborhood.

- 3. Your solution to the problem

How does your business solve a customer’s problem? What is your product or service? Make sure your product or service is addressing your customer’s needs.

- 4. Your customer

Who is your ideal customer? A great exercise is to create a buyer persona, but you can just jot down some notes at this stage about who your customer is. Focus on a specific type of customer or certain groups. Focusing on “everyone” is not a sound business strategy.

- 5. The competition

Who is your competition , and what sets you apart? How are you better or different than other options available to your customers?

- 6. Sales channels

How will you reach your target customers ? Do you have a single storefront? Are you selling online? Do you rely on distributors to get your products onto store shelves?

- 7. Marketing activities

How will you let your customers know about your product or service? Do you need to go to trade shows? Will you buy online advertising?

- 8. Your team

Probably the single key to a successful business is a great group of people to turn an idea into reality. Do you have the right people? If you need additional key team members to help you build the business, identify them here.

- 9. Your business model

“ Business model ” sounds like a confusing term, but really it’s just a fancy way of talking about how you will make money. In the early stages of fleshing out your business idea, you can just write down a few bullet points about how you will make money and what your key expenses will be.

As you refine your business idea, you will want to turn these initial notes into a sales forecast and an expense budget . But for your initial 20-minute plan, just write down a short list of the things you will charge for and the important expenses that you will have as you run the business.

- 10. Milestones

Ideas are nothing without execution—you need to turn your idea into a real business. Use the “ Milestones ” section of your one-page plan to list the critical things that need to be accomplished to start your business. Do you need to find a location? Maybe you need to get FDA approval for a new medical device. List the key milestones you need to accomplish here. Ideally, add approximate dates and list who will accomplish each task.

- 11. Partners and resources

If you need to work with other companies or business partners to get your idea off the ground, list those partners and resources here. Do you need a manufacturer or supplier for your products? Do you need a distributor to get your product on store shelves?

That’s it! A first pass at creating a one-page plan should only take 20 minutes or so. Set a timer and jump right in. Just getting everything down on paper is a great first step. The beauty of the one-page format is that you can come back and revise as you go.

- How to use your one-page plan

Now that you have the first draft of your Lean Plan, or maybe even several different mini-plans, you need to put it to use.

First, you’ll want to use your plan to identify the key assumptions about your business. Typically, those assumptions are around what famous entrepreneur and investor Marc Andreessen calls “product/market fit.” What that really means is that you’ve found a group of potential customers who have the problem you say they have, and who are willing to spend money on your solution.

Your Lean Plan includes assumptions about who your customer is, what problem they have, and what kind of solution they want.

As a next step, you’ll want to go out and talk to potential customers and verify that they do indeed have the problem you’ve assumed they have and that they’re willing to spend money on your solution.

As you gather feedback from potential customers, you’ll refine your plan . This is where you’ll be glad that you started with a one-page plan instead of a detailed business plan. It’s easy to update and revise as you go. You can quickly update it with new information as needed.

Now, if you don’t need to present a plan to outsiders, this may be all the business plan that you need. But, if you do need to create that formal business plan document, you can use your one-page plan as the key outline for that document. The business plan may also document more details about your marketing plan, product plan, or hiring plans, but ultimately, your business plan will just expand on and provide additional detail for each section of your one-page plan.

Noah is the COO at Palo Alto Software, makers of the online business plan app LivePlan. He started his career at Yahoo! and then helped start the user review site Epinions.com. From there he started a software distribution business in the UK before coming to Palo Alto Software to run the marketing and product teams.

Table of Contents

Related Articles

1 Min. Read

10 Questions to Ask Before Hiring a Business Plan Writer

14 Min. Read

15 Ways to Use and Get Incredible Value From a Business Plan

5 Min. Read

Create a Compelling Message With Your Business Plan to Sell Your Idea

6 Min. Read

11 Common Business Plan Mistakes You Should Avoid

The Bplans Newsletter

The Bplans Weekly

Subscribe now for weekly advice and free downloadable resources to help start and grow your business.

We care about your privacy. See our privacy policy .

The quickest way to turn a business idea into a business plan

Fill-in-the-blanks and automatic financials make it easy.

No thanks, I prefer writing 40-page documents.

Discover the world’s #1 plan building software

- SUGGESTED TOPICS

- The Magazine

- Newsletters

- Managing Yourself

- Managing Teams

- Work-life Balance

- The Big Idea

- Data & Visuals

- Reading Lists

- Case Selections

- HBR Learning

- Topic Feeds

- Account Settings

- Email Preferences

How to Write a Great Business Plan

- William A. Sahlman

Every seasoned investor knows that detailed financial projections for a new company are an act of imagination. Nevertheless, most business plans pour far too much ink on the numbers–and far too little on the information that really matters. Why? William Sahlman suggests that a great business plan is one that focuses on a series of questions. These questions relate to the four factors critical to the success of every new venture: the people, the opportunity, the context, and the possibilities for both risk and reward. The questions about people revolve around three issues: What do they know? Whom do they know? and How well are they known? As for opportunity, the plan should focus on two questions: Is the market for the venture’s product or service large or rapidly growing (or preferably both)? and Is the industry structurally attractive? Then, in addition to demonstrating an understanding of the context in which their venture will operate, entrepreneurs should make clear how they will respond when that context inevitably changes. Finally, the plan should look unflinchingly at the risks the new venture faces, giving would-be backers a realistic idea of what magnitude of reward they can expect and when they can expect it. A great business plan is not easy to compose, Sahlman acknowledges, largely because most entrepreneurs are wild-eyed optimists. But one that asks the right questions is a powerful tool. A better deal, not to mention a better shot at success, awaits entrepreneurs who use it.

Which information belongs—and which doesn’t—may surprise you.

Few areas of business attract as much attention as new ventures, and few aspects of new-venture creation attract as much attention as the business plan. Countless books and articles in the popular press dissect the topic. A growing number of annual business-plan contests are springing up across the United States and, increasingly, in other countries. Both graduate and undergraduate schools devote entire courses to the subject. Indeed, judging by all the hoopla surrounding business plans, you would think that the only things standing between a would-be entrepreneur and spectacular success are glossy five-color charts, a bundle of meticulous-looking spreadsheets, and a decade of month-by-month financial projections.

- William A. Sahlman is the Dimitri V. D’Arbeloff-MBA Class of 1955 Professor of Business Administration at the Harvard Business School.

Partner Center

- Search Search Please fill out this field.

What Is a Business Plan?

Understanding business plans, how to write a business plan, common elements of a business plan, the bottom line, business plan: what it is, what's included, and how to write one.

Adam Hayes, Ph.D., CFA, is a financial writer with 15+ years Wall Street experience as a derivatives trader. Besides his extensive derivative trading expertise, Adam is an expert in economics and behavioral finance. Adam received his master's in economics from The New School for Social Research and his Ph.D. from the University of Wisconsin-Madison in sociology. He is a CFA charterholder as well as holding FINRA Series 7, 55 & 63 licenses. He currently researches and teaches economic sociology and the social studies of finance at the Hebrew University in Jerusalem.

:max_bytes(150000):strip_icc():format(webp)/adam_hayes-5bfc262a46e0fb005118b414.jpg "initial assessment in business plan")

- How to Start a Business: A Comprehensive Guide and Essential Steps

- How to Do Market Research, Types, and Example

- Marketing Strategy: What It Is, How It Works, How To Create One

- Marketing in Business: Strategies and Types Explained

- What Is a Marketing Plan? Types and How to Write One

- Business Development: Definition, Strategies, Steps & Skills

- Business Plan: What It Is, What's Included, and How to Write One CURRENT ARTICLE

- Small Business Development Center (SBDC): Meaning, Types, Impact

- How to Write a Business Plan for a Loan

- Business Startup Costs: It’s in the Details

- Startup Capital Definition, Types, and Risks

- Bootstrapping Definition, Strategies, and Pros/Cons

- Crowdfunding: What It Is, How It Works, and Popular Websites

- Starting a Business with No Money: How to Begin

- A Comprehensive Guide to Establishing Business Credit

- Equity Financing: What It Is, How It Works, Pros and Cons

- Best Startup Business Loans

- Sole Proprietorship: What It Is, Pros & Cons, and Differences From an LLC

- Partnership: Definition, How It Works, Taxation, and Types

- What is an LLC? Limited Liability Company Structure and Benefits Defined

- Corporation: What It Is and How to Form One

- Starting a Small Business: Your Complete How-to Guide

- Starting an Online Business: A Step-by-Step Guide

- How to Start Your Own Bookkeeping Business: Essential Tips

- How to Start a Successful Dropshipping Business: A Comprehensive Guide

A business plan is a document that outlines a company's goals and the strategies to achieve them. It's valuable for both startups and established companies. For startups, a well-crafted business plan is crucial for attracting potential lenders and investors. Established businesses use business plans to stay on track and aligned with their growth objectives. This article will explain the key components of an effective business plan and guidance on how to write one.

Key Takeaways

- A business plan is a document detailing a company's business activities and strategies for achieving its goals.

- Startup companies use business plans to launch their venture and to attract outside investors.

- For established companies, a business plan helps keep the executive team focused on short- and long-term objectives.

- There's no single required format for a business plan, but certain key elements are essential for most companies.

Investopedia / Ryan Oakley

Any new business should have a business plan in place before beginning operations. Banks and venture capital firms often want to see a business plan before considering making a loan or providing capital to new businesses.

Even if a company doesn't need additional funding, having a business plan helps it stay focused on its goals. Research from the University of Oregon shows that businesses with a plan are significantly more likely to secure funding than those without one. Moreover, companies with a business plan grow 30% faster than those that don't plan. According to a Harvard Business Review article, entrepreneurs who write formal plans are 16% more likely to achieve viability than those who don't.

A business plan should ideally be reviewed and updated periodically to reflect achieved goals or changes in direction. An established business moving in a new direction might even create an entirely new plan.

There are numerous benefits to creating (and sticking to) a well-conceived business plan. It allows for careful consideration of ideas before significant investment, highlights potential obstacles to success, and provides a tool for seeking objective feedback from trusted outsiders. A business plan may also help ensure that a company’s executive team remains aligned on strategic action items and priorities.

While business plans vary widely, even among competitors in the same industry, they often share basic elements detailed below.

A well-crafted business plan is essential for attracting investors and guiding a company's strategic growth. It should address market needs and investor requirements and provide clear financial projections.

While there are any number of templates that you can use to write a business plan, it's best to try to avoid producing a generic-looking one. Let your plan reflect the unique personality of your business.

Many business plans use some combination of the sections below, with varying levels of detail, depending on the company.