.png "business plan for startup incubator")

- Become an Advisor

- Get started

A Comprehensive Guide to the Startup Incubator Business Model

Discover the ins and outs of the startup incubator business model with our comprehensive guide.

Are you an aspiring entrepreneur looking for the perfect environment to grow your business idea? Look no further than the startup incubator. In this comprehensive guide, we'll cover everything you need to know about the business model, including what exactly a startup incubator is, the key components of the model, and the benefits of joining, as well as types of incubators and the application and selection process.

Understanding the Startup Incubator Business Model

Starting a business can be a daunting task, especially for first-time entrepreneurs. There are countless decisions to be made, from the initial concept to the final product, and everything in between. This is where startup incubators come in.

Definition and Purpose of Startup Incubators

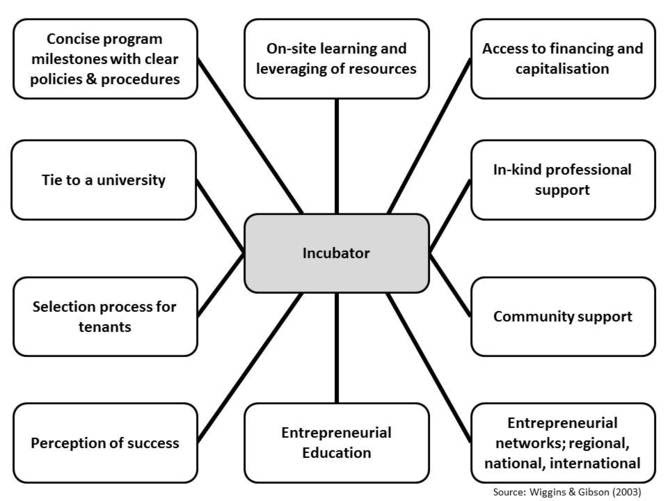

A startup incubator is a program that provides mentorship, resources, and support to early-stage startups to help them grow and succeed. The primary goal of incubators is to help startups reach a point where they can stand on their own two feet and become profitable.

Incubators typically provide startups with a physical space to work, access to a network of experts, and the opportunity to connect with other entrepreneurs who are going through similar challenges. They also offer educational workshops, seminars, and networking events to help entrepreneurs grow their businesses.

Startup incubators can be found in many different forms, from university-affiliated programs to privately funded initiatives. They are often run by experienced entrepreneurs, investors, or business professionals who have a passion for helping others succeed.

Key Components of the Incubator Model

The key components of the incubator model are mentorship, resources, and a community of like-minded individuals. Mentorship is perhaps the most important component of an incubator, as it provides entrepreneurs with access to experienced professionals who can offer guidance and advice. Resources may include office space, equipment, funding, or other resources needed to help startups grow. The community aspect of an incubator is also essential, as it allows entrepreneurs to connect with and learn from their peers.

One of the benefits of being part of an incubator is the ability to access a wide range of resources that may not be available to individual entrepreneurs. These resources can include legal and accounting services, marketing and branding support, and access to funding through venture capitalists or angel investors.

Another key component of the incubator model is the focus on education and training. Incubators often offer workshops and seminars on topics such as business planning, financial management, and marketing strategies. These educational opportunities can be invaluable for entrepreneurs who are just starting out and may not have a background in business.

Differences Between Incubators, Accelerators, and Co-working Spaces

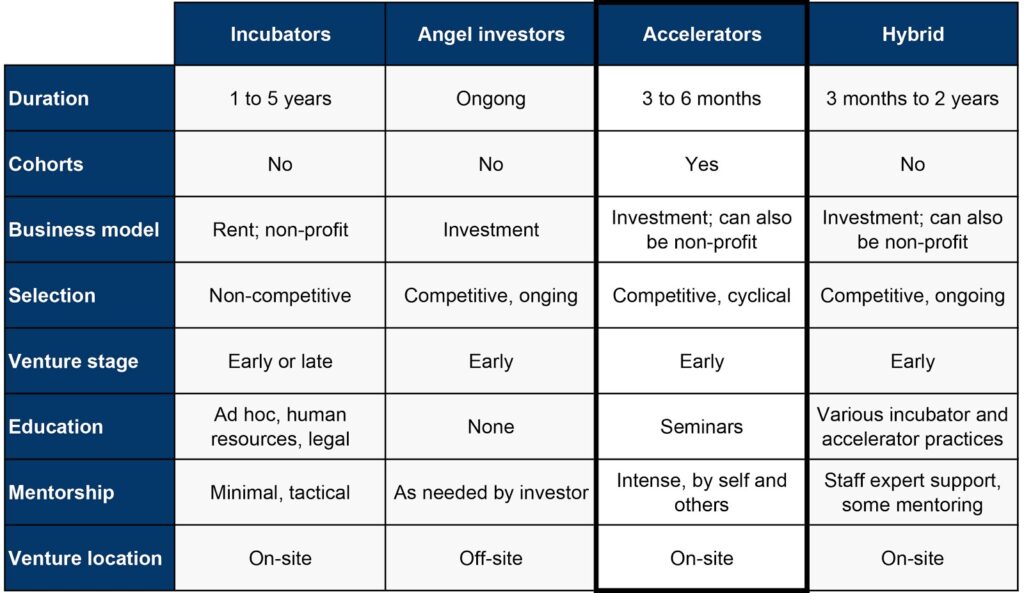

It's important to note the differences between incubators, accelerators, and co-working spaces. While all of these programs provide resources and support for entrepreneurs, incubators tend to focus on providing long-term support and mentorship, while accelerators offer a shorter-term program that focuses on fast-tracking startups to launch. Co-working spaces, on the other hand, simply provide a shared workspace and access to resources.

Incubators and accelerators are similar in many ways, but there are some key differences. Incubators tend to focus on providing support for early-stage startups, while accelerators are designed to help startups that are further along in the development process. Accelerators often provide funding, mentorship, and resources in exchange for equity in the company.

Co-working spaces are a popular option for entrepreneurs who are looking for a more flexible workspace. These spaces provide a shared office environment, which can be a great way to connect with other entrepreneurs and freelancers. However, co-working spaces may not offer the same level of support and resources as incubators or accelerators.

Overall, startup incubators are an important part of the entrepreneurial ecosystem. They provide a supportive environment for early-stage startups to grow and thrive, and offer a wide range of resources, mentorship, and educational opportunities to help entrepreneurs succeed.

The Benefits of Startup Incubators

Starting a business can be a daunting task, and many entrepreneurs struggle to get their ideas off the ground. Fortunately, startup incubators offer a range of benefits that can help early-stage startups succeed. In this article, we'll explore some of the most significant benefits of joining a startup incubator.

Access to Resources and Mentorship

One of the most significant benefits of joining a startup incubator is access to resources and mentorship. Entrepreneurs who are just starting out often lack experience and may not know where to turn for guidance. Incubators offer experienced mentors who can help entrepreneurs navigate challenges and make informed decisions. Additionally, startups may not have the resources they need to grow, such as office space or equipment. Incubators often provide these resources at a discounted rate or for free.

For example, some incubators provide access to co-working spaces, which can be a great way for startups to save money on rent and utilities. Others may offer access to specialized equipment or software that would be too expensive for startups to purchase on their own. By providing these resources, incubators can help startups grow and thrive.

Networking Opportunities

Another benefit of joining a startup incubator is the networking opportunities it provides. Incubators typically bring together a community of entrepreneurs, investors, and mentors, providing an excellent opportunity to meet potential partners, investors, or customers. Networking events and workshops can also help entrepreneurs gain valuable insights into their industry and learn from experts in their field.

Networking can be especially valuable for startups that are looking to raise capital. By connecting with investors and other entrepreneurs, startups can increase their chances of securing funding and growing their business.

Structured Support and Guidance

Incubators provide structured support and guidance to help entrepreneurs achieve their goals. They often have a curriculum in place to help entrepreneurs develop their business plan, build their team, and launch their product. They can also provide access to legal, accounting, and marketing services to help startups get off the ground.

For example, some incubators may offer workshops on how to pitch to investors or how to create a marketing plan. Others may provide one-on-one coaching sessions with experienced entrepreneurs or industry experts. By providing this structured support, incubators can help startups overcome common challenges and achieve their goals.

Increased Chances of Success

Perhaps the most significant benefit of joining a startup incubator is the increased chance of success. Incubators provide entrepreneurs with the support they need to grow their business and overcome challenges. They also provide access to resources that startups may not have been able to afford on their own. Overall, the resources, mentorship, and guidance provided by incubators can significantly increase the chances of success for early-stage startups.

In conclusion, joining a startup incubator can be an excellent way for entrepreneurs to get the support they need to succeed. From access to resources and mentorship to networking opportunities and structured support, incubators offer a range of benefits that can help startups grow and thrive.

Ready to join an advisory board?

Types of Startup Incubators

Startup incubators are organizations that provide resources, mentorship, and support to early-stage startups. They are designed to help entrepreneurs overcome the initial hurdles of starting a business and increase their chances of success. There are several types of startup incubators, each with its own unique focus and benefits.

Industry-Specific Incubators

Industry-specific incubators focus on providing support and resources to startups operating in a particular industry. For example, a biotech incubator may provide resources specifically designed to help biotech startups overcome unique challenges, such as regulatory hurdles and securing funding from investors. These incubators often have a network of industry experts and mentors who can provide guidance and advice to startups. They may also offer access to specialized equipment or facilities that are essential for startups in that industry.

University-Based Incubators

University-based incubators are run by colleges or universities and are often connected to the research or innovation departments. They typically provide mentoring, resources, and office space to startups, and may also offer educational programs or classes to help entrepreneurs develop their skills. These incubators are a great option for startups that are focused on developing new technologies or products, as they can provide access to cutting-edge research and development facilities. They also offer the opportunity to connect with academic experts and potential investors.

Corporate Incubators

Corporate incubators are run by corporations and are designed to foster innovation within a company. They often provide support and resources to both internal teams and external startups, with the goal of developing new products or services that can benefit the company. These incubators offer startups access to the resources and expertise of a large corporation, including funding, mentorship, and market insights. They also provide corporations with a way to stay competitive and innovative in their industry.

Non-Profit and Government-Sponsored Incubators

Non-profit and government-sponsored incubators are designed to support entrepreneurs who are working on social or environmental problems. They may provide access to funding, mentorship, resources, and events that focus on building a sustainable, socially responsible business. These incubators are a great option for startups that are focused on creating positive social or environmental impact, as they offer access to a network of like-minded individuals and organizations. They also provide startups with the opportunity to connect with potential investors who are interested in socially responsible investing.

Overall, startup incubators are a valuable resource for entrepreneurs who are looking to start and grow a successful business. By providing access to resources, mentorship, and support, these incubators can help startups overcome the initial challenges of starting a business and increase their chances of success.

The Application and Selection Process

Joining an incubator can be an exciting and transformative experience for startups. However, it can also be a competitive and rigorous process. To help you better understand what to expect, let's take a closer look at the application and selection process.

Eligibility Criteria for Startups

Each incubator has its own eligibility criteria for startups. While the criteria may vary from one incubator to another, there are some common factors that most incubators consider. In general, startups that are just getting started and have a high potential for growth are the most likely to be accepted. Some incubators may have specific industries or sectors that they focus on, while others may be open to startups working in any industry. Startups may also need to have a minimum viable product or a proof of concept to be considered.

Aside from these general requirements, some incubators may also have specific eligibility criteria. For example, some incubators may prefer startups that have a certain level of funding or revenue, while others may prioritize startups that have a strong social or environmental mission.

The Application Process

The application process for each incubator varies, but generally, startups are required to submit an application online. The application may include information about the product or service, the team, the business plan, and financial projections. Some incubators may require startups to go through an interview process or to give a pitch presentation to a panel of evaluators.

It's important to note that the application process can be very competitive, with many startups vying for a limited number of spots. Therefore, it's important to put your best foot forward and ensure that your application is as strong as possible.

Selection Criteria and Evaluation

The selection criteria and evaluation process also vary by incubator. Generally, startups are evaluated based on their potential for growth, the strength of their business plan, their team, and their market opportunity. Incubators may also consider factors like the level of innovation, the potential for social or environmental impact, and the compatibility of the startup with the incubator's mission and goals.

During the evaluation process, startups may be asked to provide additional information or to participate in interviews or pitch presentations. The evaluators may also conduct research on the industry and market to better understand the potential of the startup.

Ultimately, the goal of the selection process is to identify startups that have the highest potential for success and growth. Once a startup is accepted into an incubator, they can benefit from a range of resources and support, including mentorship, networking opportunities, and access to funding.

Startup incubators provide a valuable resource for entrepreneurs who are just getting started. By providing mentorship, resources, and a community of like-minded individuals, entrepreneurs can gain access to the guidance and support they need to grow their businesses. Whether you're operating in a specific industry, working on social or environmental problems, or simply looking to get your startup off the ground, there's an incubator out there that can help you succeed.

Join an Advisory Board

Connect with companies needing your expertise

See what boards you're qualified for

See what you qualify for with our 2-minute assessment

Similar Articles

Start an advisorycloud.

Join an advisory board

How to Get Your Startup Up and Running with a Business Incubator

Published: June 28, 2019

Starting a company can be a lonely process for the first-time entrepreneur. There’s a lot of hard work, self-discipline , limited feedback on priorities, and process fraught with potholes -- some critical to the success of the enterprise itself.

Over the last decade, founders and startups have turned to business incubators and accelerators to scale their business. The concept makes a lot of sense for entrepreneurs or early stage founding teams that want to leverage a defined process for success and transition to a sustainable enterprise. But what is a business incubator?

Business Incubator Definition

A business incubator is a company that helps startups and new businesses accelerate their growth and success. Incubators do this by providing support in a variety of areas including management training, office space, capital, mentorship, and networking connections.

Free Sales Plan Template

Outline your company's sales strategy in one simple, coherent sales plan.

- Target Market

- Prospecting Strategy

Download Free

All fields are required.

You're all set!

Click this link to access this resource at any time.

Incubators can be sponsored by different types of organizations including venture funds or private companies, municipal economic development organizations, and even colleges or universities.

Business Incubator Models

Some incubators are focused on different types of companies (i.e., fintech startups), vertical markets (i.e., the energy market), or geographic locations (i.e., companies in Arizona).

In fact, the National Business Incubation Association (NBIA) categorizes incubators into five models:

- Academic institutions

- Nonprofit development corporations

- For-profit property development ventures

- Venture capital firms

- A combination of the above

Companies usually spend one to two years in a business incubator -- a span determined by need and/or obligation. A benefit of the business incubator model is that it creates a shared learning experience and supports collaboration.

The ability to receive quick, accurate information from incubator executives, mentors, instructors, or fellow entrepreneurs can have a significant impact on your ability to focus on the right priorities and make the right decisions to grow your business.

What is a Small Business Incubator?

Many business incubators support small businesses or startups. So, if you're looking for a "small business incubator," you're likely simply looking for a "business incubator" that provides support for business infrastructure, training, and capital.

Note that business incubators are different than business accelerators. While incubators exist to nurture the growth of a new business, accelerators are generally geared towards helping entrepreneurs transform their ideas into products or services that are ready for market quickly -- in as little as a few months.

It's important to know the difference between these two models and to discern which is right for your company or idea.

What Does a Business Incubator Do?

An incubator should provide diverse benefits to startup entrepreneurs. These benefits can include:

- Office space - Some incubators offer office space for free or below-market rates to their portfolio companies. This solves several problems for startups. Mainly, it allows them to find a professional space for their employees to work without having to sign a lease -- especially helpful when the company is unsure how quickly they’ll scale production or headcount.

- Specialized equipment - Some incubators invest in specialized equipment, like modeling software, 3D printers, prototyping equipment, or software development labs. This is a huge advantage for scaling companies in their infancy. Access to costly equipment and simulation programs can be crucial.

- Experienced mentors - It’s important for startups to limit critical mistakes while scaling. Most incubators offer an experienced staff of savvy industry executives to help the core team stay focused and avoid mistakes. Incubators usually employ mentors with specific startup experience that can help explain process, planning, and decision criteria -- all while steering new entrepreneurs away from costly mistakes they made or witnessed.

- Group training and education - Many business incubators offer an array of important business training spanning from legal advice on startup documents, incorporation terms, or IP issues to general business challenges like how to ship a product, establish a quality culture, or establish sales and marketing processes.

- Software discounts - From accounting to project management, incubators typically offer business software that helps their startups scale. Pricing and education are typically vetted and negotiated for a standard rate allowing portfolio companies to get right to work. HubSpot offers this type of arrangement to more than 1000 startup partners worldwide .

- Shared business services - Much like leveraging software availability and selection, many incubators offer accounting, banking, marketing, and manufacturing services to help companies scale.

- Community - One of the best attributes of business incubators are the intangibles. Working with a group of like-minded entrepreneurs, using connections for connecting with prospects or customers, and learning from others in your cohort are invaluable parts of incubator life.

Is My Startup a Good Fit for a Business Incubator?

According to HubSpot for Startups’ Christian Mongillo, “The most important criteria is fit. Find a business incubator that works economically and allows you to expand as your team expands.

Look for one that has a selection process and is searching for similar types of companies. It’s not just a coworking space. The best incubators have a great mentor network and produce good results. They also have free wifi.”

Are all companies good fits for incubators? “Not necessarily,” says Mongillo. “If you’re a lifestyle company, a second-time entrepreneur, have access to office space, or want to build your own company culture, it might not be a good fit.

Some incubators require companies to give them an equity stake. So, if you don’t need the special services, you might be better off on your own.”

How Do I Get into a Business Incubator?

Being accepted into a business incubator can and should be a process. Most incubators have an admissions process and require companies to apply for acceptance.

Criteria for acceptance into an incubator varies, but most require you to present a feasible business idea and professional business plan. Here are a few steps to get started finding an incubator that’s right for your business.

- Review your options geographically or vertically - Because of the sheer volume of available incubators, you might have more than one option to choose from. By doing a quick regional search, you can understand and rank the incubators that might be a good fit. Always review the website and ask for references from successful companies they’ve helped as well as a few from companies that have dropped out to get an overall view of fit.

- Review criteria for admission - Most incubators have defined criteria for which types of companies they’re prepared to help. Some require certain milestones or criteria, like headcount, capital, entrepreneurial experience, background, revenue, or product fit. Others require contractual obligations from the accepted companies, so reviewing the application and understanding what’s is crucial to ascertaining fit.

- Prepare a business plan - A business plan might not be required during the application process, but it’s helpful in determining whether the incubator is a good match. I’m a big fan of the three-page business plan rather than an unabridged version. A simple overview of business name, team build, value proposition, competitive advantage, addressable market, go to market strategy, product or service, and a 12-month forecast can help you differentiate your company.

- Be prepared to work with a screening committee - In most cases, incubators will accept initial applications for companies meeting basic criteria. Some incubators require a video submission to explain the basic business model, vision, and mission of the company. The second stage is usually to meet and discuss your goals, plans, strengths, and weaknesses with a screening committee. This might take the form of an application, pitch or interview, and a series of meetings to set expectations for each side.

Best Startup Incubators

- Parallel 18

- Founder's Co-op

- DreamIt Ventures

- 500 Startups

- Y Combinator

- The Hatchery

- Excelerate Labs

- Capital Factory

- EnterpriseWorks

- New Venture Challenge

1. Parallel 18

2. founder’s co-op.

Helping new companies in the Pacific Northwest stack the deck in their favor.

3. DreamIt Ventures

Focused on startups with revenue or pilots ready to scale in the areas of healthtech, securetech, and urbantech.

4. Seedcamp

“Europe’s seed fund” invests in founders who attack large, global markets and solve real problems using technology.

5. 500 Startups

Diversity is a core value for this incubator. 44.5% of their portfolio belongs to racial minorities and they have scholarships available for underrepresented investors.

6. Alchemist

For founders whose revenue comes from enterprises, Alchemist offers funding, access to marquee customers, and highly rated mentors.

7. Amplify LA

Aims to help technology entrepreneurs grow their startups into successful companies. They like to invest early.

8. Y Combinator

Twice a year, they invest $120k into a large number of startups. These startups move to Silicon Valley for three months for intensive mentorship and support.

9. TechStars

A three-month program helping companies gain traction through mentorship, rapid iteration, and fundraising preparation.

10. The Hatchery

They’ll help you find customers, unite founders, and build your product. You might also receive funding from them.

11. Excelerate Labs

Mentor immersion, business acceleration, and finance and demo day preparation -- all based in Chicago.

12. Capital Factory

A Texas-based incubator that introduces startups to investors, employees, mentors, and customers.

13. EnterpriseWorks

A University of Illinois incubator focusing on biotechnology, chemical sciences, software development, and materials sciences.

14. AngelPad

With programs based in NYC and San Francisco, AngelPad spends three months working intensely with a small number of companies.

15. New Venture Challenge

Recently names the #1 University Accelerator Program in the Nation, New Venture has helped more than 200 companies successfully.

Choosing the right business incubator is a big decision. Use the criteria in this article and our Ultimate Guide to Entrepreneurship to jumpstart your journey and your success.

Need a little funding to help get your idea off the ground? Check out our list of the best crowdfunding sites to launch your business or product .

Don't forget to share this post!

Related articles.

![The Straightforward Guide to Value Chain Analysis [+ Templates]](https://www.hubspot.com/hubfs/ft-value-chain-analysis.webp "business plan for startup incubator")

The Straightforward Guide to Value Chain Analysis [+ Templates]

The 11 Best Crowdfunding Sites for Businesses (& Key Tips From Successfully Crowdfunded Entrepreneurs)

![How to Write a Business Proposal [Examples + Template]](https://www.hubspot.com/hubfs/how-to-write-business-proposal%20%281%29.webp "business plan for startup incubator")

How to Write a Business Proposal [Examples + Template]

Amazon Affiliate Program: How to Become an Amazon Associate to Boost Income

A Complete Guide to Successful Brand Positioning

70 Small Business Ideas for Anyone Who Wants to Run Their Own Business

![How to Start a Business: A Startup Guide for Entrepreneurs [Template]](https://www.hubspot.com/hubfs/How-to-Start-a-Business-Aug-11-2023-10-39-02-4844-PM.jpg "business plan for startup incubator")

How to Start a Business: A Startup Guide for Entrepreneurs [Template]

Door-to-Door Sales: The Complete Guide

Product Differentiation and What it Means for Your Brand

The 25 Best PayPal Alternatives of 2023

Outline your company's sales strategy in one simple, coherent plan.

Powerful and easy-to-use sales software that drives productivity, enables customer connection, and supports growing sales orgs

What Is an Incubator? A Complete Guide for Startups

If you’re an entrepreneur looking to get your startup off the ground, you have probably heard the word “incubator” thrown around. More than just a buzzword, incubators can be a vital tool in a startup's rise to stardom. But what is an incubator in business and how does it work?

Startup incubators are specialized hubs that can help early-stage ventures and startups navigate some of the most challenging aspects of running a business.

By the end of this comprehensive guide, you will know all about the different types of incubators, how they can help your business, and how you can get your business into an incubator.

In this article:

How does a startup incubator work?

The pros and cons of a startup incubator.

- What are the different types of startup incubators?

Could an incubator help my business?

- What do incubators want from a business?

How can I get my business into an incubator?

Startup incubators are unique organizations that function as a springboard for early-stage businesses and startups with the goal of providing specialized tools needed for startups to grow and innovate.

The resources and services they offer can vary, but often include access to office space, mentorship opportunities, business education classes, and community networking events. The structure of an incubator is much like a corporate office space and can include mandatory meetings, strict deadlines, and even a direct supervisor.

The idea for incubators began just over 60 years ago in Batavia, New York. With a family-owned factory at his disposal, Joseph Mancuso, an emerging entrepreneur, saw an opportunity to help other like-minded individuals get their small businesses off the ground. From there, he began recruiting emerging enterprises to operate in the low-cost office space located in his massive factory.

Today, there are over 7,000 incubators across the world , according to the International Business Incubation Association. This means that there’s an incubator for every type of business in practically every corner of the globe. All you need to do is find one that fits your needs and apply.

Startup incubator examples

Incubators can come in all shapes and sizes and meet all types of different needs a particular startup may have. Whether you’re looking for seed funding, networking opportunities, or mentorship, there is a startup incubator that can help.

Some examples of incubators you may or may not be familiar with include:

- Founder Institute is a global network that helps companies at every level, from startups at the idea stage to developed companies with a product and customer.

- Entrepreneurs' Organization is a peer-to-peer network of founders and builders from more than 60 countries.

- Harvard Innovation Labs is Harvard’s own entrepreneurial ecosystem of support for its students and alumni.

- Endeavor is a global organization that focuses on businesses and startups in emerging and underserved economies.

- LaunchVic’s The Good Incubator is a Melbourne-based nonprofit incubator helping people with disabilities create or grow their businesses.

- Communitech Hyperdrive is a Canadian incubator focused on technology, with a network of 28 regional innovation hubs across the country.

- MaRS is a Toronto-based hub that provides office space, advisory support, and even access to investors.

- Plug and Play is a global platform that connects blue-chip companies with startups to promote innovation.

- Station F is a Paris-based hub offering a number of perks, services, events and workshops.

- Capital Factory is an Austin-based co-working and event space dedicated to entrepreneurs, providing local founders access to mentoring and accelerator programs.

Are incubators and accelerators the same?

While they have a lot in common, incubators and accelerators have some key differences to be aware of before committing to a program.

The primary differences between incubators and accelerators are:

- Venture stage : Startup incubators generally cater to very early-stage businesses, often without a product or team. Accelerators, on the other hand, look for companies that are more built out. They generally require a business to have a minimum viable product and a team of their own.

- Funding : Incubators come with a lot of perks, but they don't always invest directly into a business. For accelerators, however, seed funding is their bread and butter.

- Time frame : Incubators offer fairly flexible timelines, typically ending only once a company has a product pitch ready for investors. Accelerators operate on a much shorter timeline. The entire goal of an accelerator is rapid growth and a fast turnaround on their investment in a company.

Did you know that only 51% of businesses survive past the fifth year ? That’s a pretty surprising statistic and can be a jarring realization for many ambitious entrepreneurs.

Businesses fail for a number of reasons. Whether they’re lacking funding, struggling to keep up with rising costs, or the managers lack the necessary experience, keeping the doors open can be a tricky feat. But this is exactly the kind of help startup incubators provide.

There are many benefits that come with joining a startup incubator, though there are some downsides as well. Let’s have a look.

What are the benefits of a startup incubator?

Startup incubators can provide startups with a number of valuable tools, from workspaces to seed funding and more.

Here is a quick look at some of the tools a startup incubator can provide and how they can help your business:

- Office space can help small companies save on rent and create unique networking opportunities with other enterprises.

- Seed funding can assist startups in tackling bigger goals and taking their businesses to the next level.

- Mentors can guide owners and managers to become more confident and efficient leaders.

- Equipment and software vouchers can provide some extra financial relief for tech startups in particular.

What are the downsides of a startup incubator?

While the benefits of startup incubators are plenty, there are some downsides to consider before committing to an incubator.

Top startup incubators can be extremely selective. Incubators can provide great financial benefits, so making sure their investments are going to pay off is a top priority.

It’s estimated that there are as many as 305 million startups created every year , while there are only 7,000 incubators. That means you’re going to have a lot of competition.

Some incubators may require a commitment of up to two years, or even until you have a product that is ready to launch.

When joining a startup incubator, you’re committing to more than just the perks — you’re committing to a culture and way of doing things with which your company may or may not align.

What are the types of startup incubators?

There are a number of different types of startup incubators all specializing in different fields, offering different perks, and with different funding models. Rest assured, however, knowing that no matter what kind of incubator you choose, they all have one common goal: to help you grow your business.

Whether you’re looking for a nonprofit organization or a VC-run incubator, it's important to understand what each type of incubator does and what they might expect from you to ensure you’re choosing the right hub for your project.

The most common categories for incubators include:

University startup incubators

Nonprofit startup incubators, corporate startup incubators.

Now, more than any other time in history, students no longer have to decide between pursuing higher education and kick-starting a business. University startup incubators (UBIs) can help with both.

University incubators are usually university- or student-run and can receive funding from donations or venture capital support. They may also invest in students’ projects and use the proceeds to fund new endeavors. These programs can provide pupils with all types of assistance and mentorship, from access to costly technology to logistical solutions.

UBIs provide students with an opportunity to chase their dreams in a financially secure and safe environment. These startup incubators are rethinking the businesses of the future.

One of the top academic incubators in the world, University of California, Berkeley’s Berkeley SkyDeck , offers students’ companies up to $200,000 after being accepted. It also provides support with logistics, customer development, and even marketing and advertising.

Some startups set out to change the world without taking a profit. For this reason, nonprofit startup incubators are just as valuable as other incubators.

Nonprofit incubators are programs and work spaces that cater exclusively to — you guessed it — nonprofit businesses. These incubators leverage their networks, know-how, and resources to provide nonprofit startups with the tools they need to grow and accomplish their goals.

Resources can include things like office space or technology, which can prove to be a major benefit for nonprofit businesses that often struggle to secure these costly tools.

An example of a top nonprofit startup incubator is MassChallenge , a global organization helping early-stage companies solve some of the world’s most pressing challenges. Their program covers industries such as health and financial tech, sustainable food, and even space commercialization, just to name a few.

Corporate incubators are typically in-house programs or independent business units built to curate and develop ideas within their own company. These incubators, like others, focus on early-stage ideas, sometimes with the goal of creating an entirely new business or product. Corporate startup incubators have the advantage of leveraging business assets to create brand-new revenue streams and create a hub for innovation within their own company, all while helping employees feel like they’re part of something bigger. One of the most notable corporate incubators is Google’s Area 120 —a radical idea built to help employees pursue their own radical ideas. Google’s in-house incubator features over 120 teams working on all kinds of projects, from AI customer support agents to a new tool that helps creators easily dub their content to expand their audience.

Starting a business is hard work and incubators come with a lot of perks, though it is important to remember that not all incubators are the same and not all businesses are a good fit for an incubator. Determining if an incubator is good for a startup can be a tricky task. Before diving headfirst into a time-consuming and competitive incubator application process, you may want to ask yourself a few questions:

- Am I ready to give up equity in my business?

- Does the incubator I’ve chosen align with my business’s core values?

- Can I commit to a rigorous schedule set by someone else?

- Do I really want to answer to someone else?

By asking yourself these questions, you make a more informed decision as to whether or not the perks of a startup incubator are worth the cost.

No first-time entrepreneur has the business network of contacts needed to succeed. An incubator should be well integrated into the local business community and have a steady source of contacts and introductions.

It should come as no surprise that the resources startup incubators provide are highly sought after, and that entry to a startup incubator is a complicated and competitive process. But that doesn’t mean you can’t be prepared.

Here are a few tips that can help you in your application process:

- Explore your options . The world is a big place, and with over 7,000 incubators scattered across the globe, it’s worth checking out different options.

- Find the right fit . Think about your goals and what exactly you’d like from an incubator. Every incubator is different and finding the right match is imperative.

- Be aware of the required milestones . Incubators typically help individuals create something from the ground up, but that doesn’t mean you’re applying to a program empty-handed. You should have an idea of what milestones you hope to achieve and a time frame in which you plan to meet your goals.

- Create a killer business plan . Doing a deep dive into your business, your value proposition, and your projections will help you better understand what you’re looking for from an incubator. Additionally, it will help an incubator better understand exactly why they should accept your business.

- Brace yourself for a grueling application process . Patience is the name of the game when applying for a startup incubator. The interview can be exhausting and time-consuming, so it’s important to remember why you’re there in the first place.

Startup incubators are some of the most sought-after programs in the startup universe. They can help build a business from the ground up, offering a number of huge benefits, especially for early-stage ventures.

Deciding which startup incubator is best suited for your startup can be a difficult task, but now you’ve got a better understanding of some of the ins and outs of the process.

It’s on you to make the next move, but we’re here to help. Building a business is a daunting task, and your tech stack shouldn’t make it harder. Apply to HubSpot for Startups today and gain access to all the tools you need to increase leads, accelerate sales, and streamline your startup.

Header image by Brooke Cagle on Unsplash

Your go-to destination for education, inspiration, and resources for startup founders.

Startup Resources

What Is a Business Accelerator? Everything You Need To Know - HubSpot for Startups

How to Conduct Market Research for Startups

6 Steps to Managing Remote Teams: A Guide for Startups

28 Startup Trends to Watch in 2023 - HubSpot for Startups

Advisory boards aren’t only for executives. Join the LogRocket Content Advisory Board today →

- Product Management

- Solve User-Reported Issues

- Find Issues Faster

- Optimize Conversion and Adoption

Business incubators: A guide for startups

Startups begin with an idea that founders can then formulate into a business plan. However, building and growing a viable business is difficult and requires help from others. To address this, entrepreneurs often look to incubators to help fill the gap between ideas and a real product.

To decide if a business incubator is right for you, let’s dive into what it is and how it helps startup development. The article also covers how to choose the best one for your startup needs.

What is a business incubator?

A business incubator is a workspace designed to give a startup company the resources it needs to succeed. The perks of a business incubator vary from each program, but it often includes mentorship and other professional services. The goal of a business incubator is to turn a promising idea into a developing startup with a strong chance of success.

What is the role of an incubator?

Business incubators are often sponsored by universities or non-profit organizations. Private ventures may also fund incubator programs. Startups can spend a few months or a few years in an incubator before they “graduate.”

Incubators play many roles in startup development. They aim to nurture early-stage companies into sustainable businesses. Incubators provide a range of support, depending on the program. They may help your startup company with:

- Office space — Incubators are frequently housed in a shared workspace with other startups in the program. The office space and equipment are either included or offered at below-market rates. Utilities like internet services are also part of the incubator

- Mentorship — One of the key benefits of an incubator is having top mentors available to you. They can provide guidance and share their expertise to help you navigate challenges

- Education and training — Incubators offer workshops and other programs to help a startup develop the skills it needs to succeed

- Access to investors — Some incubators may arrange pitch meetings with investors to help companies secure funding. Other incubators may offer funding in exchange for equity in the company. Some incubators are prestigious with a high reputation which can gain your company favor from investors

- Networking — Incubators provide a space for startups to meet potential partners, mentors, and investors. Through networking, startups gain a wider network of support and potential business opportunities

- Revenue growth — Achieving revenue growth is easier when your company participates in an incubator. It can lower overhead costs and help you connect with investors

- Professional services — Many incubators provide professional services like legal counseling or accounting. These services can help your company get started on a positive note

- Support from other entrepreneurs — Sharing your incubator experience with other startup companies means you can learn from each other. The inspiration may help you launch your company quicker and more smoothly

Why do startups need incubators?

As you begin to take the first steps to developing your business idea, you may wonder if applying for an incubator is the right choice. Your startup could indeed develop into a successful venture without an incubator. However, a business incubator can provide many opportunities that you wouldn’t get otherwise.

For starters, an incubator can provide tailored support for your startup. As your business plan evolves, your mentors are right there with you to provide guidance and structure. They can also provide advice on how to avoid common pitfalls in your industry. Mentorship is a valuable tool, and you shouldn’t overlook it.

What is the difference between incubators and accelerators?

Incubators and accelerators are often used interchangeably. To be fair, they both provide support to companies, but incubators and accelerators have different key characteristics. If you’re not sure if you should join an incubator or an accelerator, evaluate these factors:

- Venture stage — If you have a minimal viable product (MVP) and a business model, then an accelerator is a better fit for you. If you have an idea and a detailed business plan, then an incubator is ideal

- Founding team — Accelerators prefer a fully functioning team when evaluating companies. Meanwhile, an incubator is more willing to work with solo entrepreneurs or minimal team members

- Funding and equity — Accelerators often provide funding in exchange for capital. Incubators are less likely to have this arrangement and charge a fee instead

- Timeline — Accelerators are often intense programs that take a few months to complete. Incubators have longer timelines and it’s not uncommon for startups to stay for a couple of years or more. However, the timeline will vary from program to program

- Application process — Both incubator and accelerator programs need proof that your idea or product has high potential. For an incubator, you’ll need a strong business plan. An accelerator application will need you to prove product-market fit and a developed business model

The biggest difference between an incubator and an accelerator is the venture stage. Incubators are more willing to work with early-stage startups, even if all they have is an idea and a business plan. Meanwhile, accelerators expect you to have an MVP and already be operational on some level.

Successful startups from incubators

Incubators often give startups the resources they need to succeed. Here are some examples of startups that went through an incubator and are successful today:

Don’t think you need a fully developed product and business model to have success. Popular startup program Y Combinator says on average, 40 percent of the companies it funds are just an idea.

How to choose the right incubator

There are many incubators available to startups. The International Business Innovation Association (INBIA) estimates that 1,400 incubators are running in the U.S.

It’s not hard to find an incubator, but it’s difficult to get accepted. Top-tier competitive programs can have an acceptance rate of 1-2 percent . For comparison, the Harvard University acceptance rate for the Class of 2027 is 3.4 percent.

Beyond creating a competitive application, a startup needs to choose an incubator that fits its needs. Not all incubator programs are alike, so it’s essential to evaluate a program’s value before applying. Here are a few things to consider:

- Do extensive research — Make sure you have looked at an incubator’s resources, structure, and services. Is it what you need to succeed? If you are willing to relocate, you may also want to consider incubators in other areas. You’ll also want to consider the experience of the mentors and the weekly time commitment of the program

- Consult alumni — No one knows the value of an incubator better than the alumni. You may want to consider contacting companies that the incubator has helped

- Assemble your team — While incubators may consider a solo applicant, you may also want to consider finding a co-founder or other team members. It’s essential to prove to incubators that you have the skills necessary to build your idea

- Prepare a pitch — Incubators want to know why you think you can succeed. Prepare a well-researched pitch that shows why you are different and how you are a match for the program

Key takeaways

Incubators are a valuable resource for startups with a developed idea that need guidance on what to do next. You don’t need an MVP to apply for an incubator, but you should prepare a strong business plan and a solid pitch. Your goal is to show that your idea has potential.

Choose an incubator that has the resources that are best fit for your needs. The lessons, personalized feedback, and networking opportunities are crucial for building your company.

Featured image source: IconScout

LogRocket generates product insights that lead to meaningful action

Get your teams on the same page — try LogRocket today.

Share this:

- Click to share on Twitter (Opens in new window)

- Click to share on Reddit (Opens in new window)

- Click to share on LinkedIn (Opens in new window)

- Click to share on Facebook (Opens in new window)

- #collaboration and communication

- #project management

Stop guessing about your digital experience with LogRocket

Recent posts:.

5 lessons from helping 9 startups move to outcome-driven work

Learn five essential lessons from guiding nine startups to an outcome-driven, product-led approach, including niche focus, flexible frameworks, and decisive action.

Leader Spotlight: Slowing things down to run really fast, with Brian Bates

Brian Bates, Senior Vice President of Business Development at Lively Root, talks about how he works to scale small startups.

Building and scaling product teams in startups vs. large enterprises

When a product team is scaled correctly, it is well-equipped to meet unique challenges and opportunities in an ever-changing product landscape. Discover how to build and scale product teams effectively, no matter the size of your organization.

Crafting meaningful core values for your company

Core values provide all individuals within an organization a framework to make their own decisions on a day-to-day basis.

Leave a Reply Cancel reply

How to Apply and Get Accepted to a Startup Incubator

Learn to define your goals, create a compelling application, and secure your place in a supportive ecosystem that can accelerate your entrepreneurial journey.

In the fast-paced and competitive realm of startups, securing a coveted spot in a startup incubator can be a game-changer. It’s like finding the treasure map to entrepreneurial success. In this comprehensive guide, we’ll take you on a journey on how to apply for startup incubator , unpacking the entire process, from understanding the profound benefits of joining a startup incubator to mastering the art of crafting an application that stands head and shoulders above the rest. Moreover, we’ll introduce you to PitchBob , an invaluable resource that can help you navigate the intricacies of the application process with finesse.

A startup incubator, often simply referred to as an "incubator," is more than just a place where startups are nurtured. It’s a comprehensive program designed to offer invaluable support to early-stage startups, turning them into thriving businesses. The incubator provides a structured and supportive environment that empowers entrepreneurs with the tools they need to succeed.

It’s a program designed to offer these fledgling ventures the guidance, resources, and collaborative ecosystem they need to evolve and thrive. Here are the core benefits:

- Mentorship: You gain access to experienced entrepreneurs and industry experts who selflessly share their wisdom and insights.

- Resources: The incubator provides crucial resources, including office space, financial support, and invaluable networking opportunities.

- Collaborative Environment: It’s an environment where you rub shoulders with like-minded entrepreneurs, offering fertile ground for exchanging ideas, experiences, and even partnerships.

Why Join a Startup Incubator?

Timing is everything in the world of startups, and being part of a startup incubator can make or break your entrepreneurial journey. The earlier you secure a spot, the better your chances of success. The numbers don’t lie; startup failures are alarmingly high. In fact, according to According to Exploding Topics , a reputable source for startup insights and trends, the startup landscape is indeed a challenging terrain. Let’s explore some key statistics:

90% of Startups Fail: It’s an alarming statistic, but one that we cannot ignore. Approximately 90% of startups ultimately do not survive the tumultuous journey to success. This demonstrates just how crucial it is for entrepreneurs to seek the support and guidance of incubators.

Top Reasons for Failure: The statistics also shed light on the primary causes behind these failures. Among the top reasons are a lack of market need for the product or service, running out of capital, and not having the right team in place. These are challenges that startup incubators are specifically designed to help you address.

The Role of Incubators: The statistics reveal that startups that are a part of incubators have a significantly higher survival rate. The structured support, mentorship, and resources provided by incubators contribute to this enhanced chance of success.

The Power of Timing: 22% of failed businesses didn’t implement the correct marketing strategies. Startups that join an incubator in their early stages tend to perform better and have a higher likelihood of success. This emphasizes the importance of applying for an incubator as early as possible.

Types of Startup Incubators

Now that we have a comprehensive understanding of what a startup incubator is and the compelling benefits it offers, let’s explore the rich and diverse tapestry of incubators available to budding entrepreneurs. Each type of incubator is meticulously designed to cater to specific entrepreneurial needs, and this diversity is an important aspect of the startup ecosystem.

Industry-Specific Incubators

Industry-specific incubators are precisely what the name suggests — they are incubators that are laser-focused on startups within a particular sector or niche. These specialized incubators provide targeted support and expertise tailored to the unique challenges and opportunities within that specific industry. Whether you’re venturing into the world of biotechnology, artificial intelligence, e-commerce, or any other field, there’s likely an industry-specific incubator designed to meet your needs.

University Incubators

Nestled within the academic realm, university incubators offer a unique blend of resources and opportunities. These incubators are typically located within educational institutions, allowing startups to tap into the vast knowledge and research capabilities of universities. University incubators offer an array of benefits, including access to cutting-edge research, collaboration with academics and researchers, and, often, a pool of potential talent.

Corporate Incubators

Corporate incubators are an interesting facet of the startup landscape. These are incubators initiated and run by established companies, often industry giants. The primary motivation behind corporate incubators is to identify innovative ideas that align with their core business and to invest in or collaborate with these startups. By joining a corporate incubator, startups can access a treasure trove of resources and support, including funding, infrastructure, and industry expertise.

How Can You Apply for a Startup Incubator

With a clear understanding of what startup incubators are and the benefits they offer, let’s take a deep dive into the meticulous art of preparing and submitting your application.

Step 1: Defining Your Goals

Aimlessly wandering into the application process is like setting sail without a destination. To align your application with the incubator’s mission, you must first define your goals and objectives. Why do you want to be part of an incubator, and what do you hope to achieve? This clarity not only guides your application but also demonstrates your commitment and purpose.

Step 2: The Art of Researching Incubators

In your quest to find the ideal incubator, research is your most potent weapon. Explore the wide array of startup incubators available in the market. Take into account factors like location, industry focus, program duration, and the specific resources they offer. Ensure that the incubator aligns harmoniously with your startup’s objectives and values.

Step 3: Crafting a Killer Business Plan

Now, let’s get down to the nitty-gritty — your business plan. Your business plan is the cornerstone of your application. A well-structured and comprehensive business plan is essential. It should leave no room for doubt regarding your business concept, your target market, your revenue model, and the growth strategy you intend to employ. This plan should paint a vivid picture of your startup’s journey and potential. You can use PitchBob’s AI Business Plan Generator tool.

Step 4: The Art of Developing a Pitch Deck

A pitch deck is your visual narrative — a compelling story that mirrors the essence of your startup. It is your chance to highlight your startup’s value proposition, and it must be nothing short of captivating. A well-crafted pitch deck is not just an accessory; it’s a pivotal piece of your application puzzle.

Step 5: The Application Process Unveiled

With your goals, research, business plan, and pitch deck in hand, it’s time to fill out the application form. This step demands meticulous attention to detail. Provide all requested information with precision, conciseness, and clarity. Ensure that your responses reflect your passion, vision, and commitment.

Step 6: Crafting a Convincing Personal Statement

Your personal statement is your opportunity to present the human side of your entrepreneurial journey. It should be a testament to your unwavering passion for your startup and your unwavering commitment to its success. Use this space to share your journey, your motivations, and your personal investment in your vision.

Step 7: Gathering References

References can serve as the golden ticket that seals the deal. Collect references that genuinely vouch for your skills, character, and the value of your startup idea. Strong references can significantly boost the credibility of your application.

Step 8: The Fine Art of Pitch Practice

A winning pitch is not born; it is made. Practice your pitch relentlessly until it gleams with confidence, clarity, and conviction. The ability to articulate your vision effectively is paramount during the presentation.

Step 9: Be Prepared for Interviews

If your application shines and you find yourself on the shortlist, be prepared for interviews. Anticipate questions about your startup, your aspirations, and your ability to collaborate. A well-prepared interview can be the cherry on top of your application.

Securing Your Place at the Table: Strategies for a Winning Application

All startup ideas are not created equal, and it’s imperative to understand the kind of concepts that incubators seek:

- Groundbreaking Concepts: These are the transformative ideas that have the potential to revolutionize entire industries upon market introduction. They are the diamonds in the rough.

- Progressive Concepts: Progressive concepts involve enhancements to existing products or services, ensuring they reach the next level of excellence. They represent the next step in evolutionary innovation.

- Conventional Concepts: While conventional concepts might have profit potential, they often don’t align with what incubators typically seek. Incubators primarily gravitate toward groundbreaking and progressive ideas, as they promise substantial market disruption and innovation.

How PitchBob Can Be Your Navigator on This Journey

At PitchBob , we empathize with the challenges you face as a startup entrepreneur, and we’re here to provide you with the tools and support on how to apply for startup incubator . Generate your pitch deck with ai as our aim is to ensure that you shine brightly in the fiercely competitive world of startup incubators.

In conclusion, the world of startup incubators offers a rich tapestry of options, each finely tuned to address the specific needs and aspirations of entrepreneurs. Industry-specific incubators provide a deep dive into the intricacies of particular sectors, offering specialized guidance and connections. University incubators bridge the gap between academia and entrepreneurship, harnessing the intellectual power of educational institutions to fuel innovation. Meanwhile, corporate incubators, backed by industry leaders, bring substantial resources and investment opportunities to the table. Whether you’re driven by niche expertise, academic collaboration, or corporate support, the diverse incubator landscape promises a supportive ecosystem for your entrepreneurial dreams.

Disruptive Partners OÜ Harju maakond, Tallinn, Kesklinna linnaosa, Tornimäe tn 3 / 5 / 7, 10145

PitchBob, Inc 2261 Market Street #10281 San Francisco, CA 94114

Oct 3, 2023

Startup Incubator

Go-To-Market

If you’re in the process of launching a startup, you’ve probably thought about applying for a startup incubator. In this guide, we cover all the basics: what they are, what they cost, what the requirements are and so much more. We also cover how they compare to other startup resources, such as accelerators, and we provide an overview of the top startup incubators. Finally, we provide tips on how to select the right incubator for you—let’s dive in!

What is a startup incubator?

A startup incubator, also known as a ‘business incubator’, is a program that provides resources and support to new small businesses and first-time founders. Incubators typically provide access to mentorship, discounted technology, physical workspaces, and networking opportunities. It is designed to help startups test their ideas, hone their business plans, and secure their first customers—which is helpful for getting a new initiative off the ground and securing funding from venture capitalists down the line.

How do startup incubators work?

Startup incubators typically have an application process that entrepreneurs must complete to be considered. Once accepted, entrepreneurs are typically required to participate in a program that lasts anywhere from a few months to a year. During said time, founders are provided with a ton of resources including mentorship, office space, and networking opportunities to help hone their business plan and grow their business. At the end of the program, entrepreneurs present their businesses to potential investors to secure funding.

What are the requirements to get into a startup incubator?

The requirements to get into a startup incubator vary from program to program. Most incubators require founders to have an idea for a startup, a business plan, and a team of at least two people. In addition, some incubators also require that entrepreneurs meet a minimum funding threshold before applying. Outside of the basic requirements, some incubators focus on specific niches, like med tech startups or health tech startups, some have specific requirements for the types of businesses they accept, and some only focus on startups in a particular area, like Silicon Valley.

Why do founders use startup incubators?

Startup incubators are a great way for first-time founders and early-stage startups to get their businesses off the ground quickly and find product market fit. As mentioned above, they provide a ton of key resources to ensure the highest possibility of success. In addition to the resources, incubators may also provide founders with introductions to mentors, investors, and industry experts to help scale their ideas. Finally, startup incubators typically provide entrepreneurs with exposure to investors during the final phase of the program: demo day.

What are the types of startup incubators?

Startup incubators come in a variety of shapes and sizes. They can either be for-profit or non-profit, and they can be focused on specific industries or they can be open to all kinds of businesses. Here are some of the common types of startup incubators:

- For-profit incubators : These incubators make money by taking equity in the businesses they help launch.

- Non-profit incubators : These incubators are typically funded by grants or donations, and they don’t take equity in the businesses they help launch.

- Industry-specific incubators : These incubators are focused on a specific industry such as healthcare, technology, or fashion.

- Geographic incubators : These incubators are focused on a specific geographic area, and they typically offer access to local resources and networking opportunities.

What are the benefits of going through a startup incubator?

There are many benefits to going through a startup incubator. Here are some of the top benefits:

- Access to resources : Incubators typically provide access to resources including physical workspace, discounted software, and potentially even raw materials.

- Guidance and support : Incubators typically provide founders with the guidance and support they need to launch their businesses through introductions to mentors and industry experts.

- Exposure : Incubators typically provide founders with the opportunity to gain exposure to investors to potentially secure funding.

What are the drawbacks of going through a startup incubator?

While there are many benefits to going through a startup incubator, there are a few drawbacks to consider, here are some of the most common:

- Equity : Some incubators charge a percentage of equity in exchange for the resources, guidance, and exposure they provide.

- Time commitment : Incubators typically require founders to participate in a program that lasts anywhere from a few months to a year, which may not work for everyone.

- Restrictions : Some incubators have restrictions such as specific industries or geographic areas they focus on.

What is the difference between startup incubators and startup accelerators?

Startup incubators and accelerator programs are similar in that they both provide resources and support to entrepreneurs. However, there are some key differences between the two.

Startup incubators typically have a longer program that lasts anywhere from a few months to a year. They provide access to resources such as mentorship, workspaces, and networking opportunities. They also provide guidance and support to entrepreneurs to help them develop their business ideas and launch their startups.

Startup accelerators, like YCombinator or 500 startups , on the other hand, are typically shorter programs that last anywhere from a few weeks to a few months. They provide access to similar resources such as mentorship, funding, workspace, and networking opportunities, but they are designed to help founders scale their startups, not launch them, and help prepare them to take on seed funding or venture capital.

What does participating in a startup incubator cost?

The cost of participating in a startup incubator varies depending on the program. Some incubators are free, while others may charge fees or require you to give them equity.

Do startup incubators provide capital to startups?

Some incubators provide access to funding and grants to help startups get off the ground, others do not. It depends on how large the incubator is and what type of incubator it is (for-profit vs not-for-profit).

What are the top startup incubators in the United States?

There are many great startup incubators out there, but some of the top ones include Idealab, The Batchery , Upward , SteelBridge Laboratories , and Invenshure .

- Idealab is a technological incubator out of Pasadena, CA that gives start-ups the resources they need to launch new products and services quickly.

- The Batchery is a global incubator situated in Berkeley, CA that focuses on seed-stage firms that are primed for rapid growth.

- Upward is a global incubator based out of New York City that is dedicated to reviving second-tier towns through innovation.

- SteelBridge Laboratories is an incubator based out of Pittsburg, PA for FinTech startups.

- Invenshure is a medical device and imaging incubator based out of Minneapolis, MN that invests in medicines, developing platform technologies, and medical device and imaging startups.

What to look for and how to select a startup incubator?

When selecting a startup incubator, it’s important to do your research and talk to other founders who have graduated from the program. Here are some of the things to look for when deciding between multiple startup incubators:

- Resources : What resources does the incubator provide? Does it provide access to mentors, investors, and industry experts? What about workspace, funding, and other resources?

- Equity : Does the incubator take equity in the businesses they help launch? Am I okay with giving up equity in my business in exchange for the services it provides?

- Time commitment : What is the length of the program? Am I committed to putting in the time required to make the program successful?

- Reviews : What did other founders say about the program, did they think it was worth it? What are some of the critiques other founders had and are you okay with that?

- Track record : What is the historical performance of the companies that have graduated from the program? Are there only one or two stand-out successes or many successes?

Final thoughts on startup incubators

Startup incubators are a great way for founders to initially get their startups off the ground quickly. They provide access to a ton of resources which can be invaluable to founders that are strapped for cash. Before deciding to participate in an incubator, make sure to do your research so you understand exactly what is required of you to graduate. Also, make sure to talk to other founders to ensure the program fits your needs and what you are looking to get out of it.

Stay up to date

Get the latest from Arc in your inbox:

Share this post

- Startup Funding

- Startup Incubator

- Venture Advisory

What is a Startup Incubator? – Everything you need to know: The Ultimate Guide

Hey there, ambitious founders! Are you dreaming of turning your groundbreaking idea into a thriving business? Well, you’re in for a treat! Let’s talk about one of the most valuable resources at your disposal – a startup incubator. Trust me; these incubators can work wonders for your startup journey!

So, what’s the buzz about startup incubators? Imagine a nurturing environment, a safe haven where your fledgling startup gets all the support it needs to take flight. That’s exactly what an incubator is all about.

In this post, we'll cover:

- 1 What is a Startup Incubator?

- 2 How do Startup Incubators Work?

- 3 What Can Startup Incubators Offer You?

- 4 How to Choose the Right Incubator?

- 5 How does a startup incubator differ from an accelerator?

- 6 How can a startup incubator help my business grow?

- 7 What kind of support and resources do startup incubators provide to early-stage startups?

- 8.1 Benefits of Joining an Incubator:

- 8.2 When You Might Not Need an Incubator:

- 9 What are the typical criteria and qualifications for getting accepted into a startup incubator program?

- 10.1 Commitments Involved:

- 11 What are the potential costs or equity implications of joining a startup incubator?

- 12 Examples of successful startups that have graduated from specific incubators?

- 13 How can I best prepare my startup to make the most of the incubator program and maximize our chances of success?

- 14 TL;DR – Startup Incubator

- 15 Ready to Take the Leap?

What is a Startup Incubator?

Think of startup incubators as the ultimate mentors, cheerleaders, and protectors for your business. These organizations are designed to help early-stage startups find their footing and grow stronger. They provide a structured program with expert guidance, resources, and funding to fuel your growth.

Check out – list of the world’s top startup incubators

How do Startup Incubators Work?

Picture this: you’ve got an incredible startup idea , but you’re not quite sure how to turn it into a full-fledged business. That’s where the magic of incubators comes into play. When you join an incubator, you’re not just entering an office space; you’re entering a whole community of like-minded entrepreneurs.

Incubators typically run cohort-based programs, where a group of startups starts and completes the program together. Throughout the program, you’ll receive hands-on guidance, workshops, and access to industry experts, all tailored to meet your specific needs.

What Can Startup Incubators Offer You?

Mentorship Galore : Imagine having a team of seasoned entrepreneurs, investors, and industry experts guiding you through the ups and downs of entrepreneurship. Incubators provide you with mentors who’ve “been there, done that” and can help you avoid common pitfalls.

Access to Funding : Money talks, and incubators can help you find investors who are willing to back your vision. They often have strong networks with angel investors and venture capitalists looking for promising startups.

World-Class Resources : From office space and technology infrastructure to legal and accounting services, incubators ensure you have all the essential resources at your fingertips.

Networking Nirvana : Remember, it’s not just about what you know, but who you know. Incubators offer a unique opportunity to connect with other entrepreneurs, potential partners, and customers, giving your startup a head start.

Validation and Credibility : Being associated with a reputable incubator can add instant credibility to your startup. It tells the world that your idea has potential, which can attract customers and investors alike.

How to Choose the Right Incubator?

Now that you’re all pumped up about startup incubators, it’s time to find the perfect match. But, hold your horses! Not all incubators are created equal, and what works for one startup might not work for another. Here are some key factors to consider when making your choice:

Focus Area : Look for an incubator that specializes in your industry or domain. They’ll understand your unique challenges and provide tailored support.

Track Recor d: Do your research! Check out the success stories of startups that have graduated from the incubator. It’s an excellent indicator of what you can expect.

Program Duration : Incubator programs can vary in length, from a few months to a year or more. Choose one that aligns with your startup’s needs and timeline.

Equity vs. No-Equity : Some incubators may take a small percentage of equity in return for their support. Decide if you’re comfortable with this arrangement. For example, Y Combinator takes a 7% equity while many others like StartupGuru are equity-free.

How does a startup incubator differ from an accelerator?

The terms “startup incubator” and “ accelerator ” are often used interchangeably, but they serve distinct purposes for your startup and offer different types of support to early-stage startups.

While both startup incubators and accelerators aim to support early-stage startups, incubators focus on idea validation and foundational support over a more extended period, while accelerators are geared towards rapid growth and scaling over a shorter, intensive program.

The choice between an incubator and an accelerator depends on the specific needs and stage of development of the startup .

How can a startup incubator help my business grow?

A startup incubator can be a game-changer for your business growth, offering a wealth of benefits and support. Here’s how a startup incubator can help your business take flight:

Mentorship and Guidance : Incubators provide access to experienced mentors and industry experts who can offer valuable insights, feedback, and guidance. They have “been there, done that” and can help you navigate the challenges and pitfalls of entrepreneurship.

Networking Opportunities : Incubators create a supportive community of like-minded entrepreneurs. You’ll have the chance to network with fellow founders, potential partners, customers, and investors. Building strong connections can open doors for your startup.

Access to Funding : Incubators often have connections with angel investors, venture capitalists, and other funding sources. They can help you secure the necessary capital to fuel your growth and take your startup to the next level.

World-Class Resources : From office space and technology infrastructure to legal and accounting services, incubators provide essential resources that might otherwise be costly and challenging for a young startup to access.

Structured Program : Incubators offer a structured and focused program designed to accelerate your startup’s progress. Through workshops, seminars, and one-on-one support, you’ll gain the knowledge and skills needed to succeed.