- Lifestyles & Social Issues

- Philosophy & Religion

- Politics, Law & Government

- World History

- Health & Medicine

- Browse Biographies

- Birds, Reptiles & Other Vertebrates

- Bugs, Mollusks & Other Invertebrates

- Environment

- Fossils & Geologic Time

- Geography & Travel

- Entertainment & Pop Culture

- Sports & Recreation

- Visual Arts

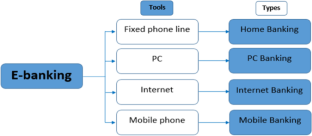

electronic banking

Electronic banking is the use of computers, phones, and other technologies to facilitate banking transactions rather than through human interaction. Electronic banking includes features like electronic funds transfer (EFT) and mobile payments for retail purchases, automatic teller machines (ATMs), automatic paycheck deposits , and automated bill payment .

In the 21st century, banks have set up secure, encrypted access to their websites—and later to mobile apps —enabling clients to access their accounts, view account balances, transfer money among accounts, purchase certificates of deposit (CDs) , and—if connected a brokerage account—buy and sell stocks, bonds, and other securities .

Electronic banking has greatly reduced the need to move paper money and coins from one place to another, and humans are no longer required to facilitate every banking transaction .

E-banking Overview: Concepts, Challenges and Solutions

- Published: 28 November 2020

- Volume 117 , pages 1059–1078, ( 2021 )

Cite this article

- Belbergui Chaimaa 1 ,

- Elkamoun Najib 1 &

- Hilal Rachid 1

4574 Accesses

23 Citations

1 Altmetric

Explore all metrics

The expansion of information technology has led to a new form of banking. Traditional banking, based on the physical presence of the customer, is only a part of banking activities. In the last few years, electronic banking has emerged, adopting a new distribution channels like Internet and mobile services. The main goal was to allow businesses to improve the quality of service delivery and reduce transaction cost, and anytime and anywhere service demand for customers. However, it increased the vulnerability to fraudulent activities like spamming, phishing and credit card frauds. Then, the main challenge that opposes electronic banking is ensuring banking security. In this context, this paper aims to provide an overview of the electronic banking service highlighting various aspects, investigating various challenges and risks, and discussing some proposed solutions.

This is a preview of subscription content, log in via an institution to check access.

Access this article

Price includes VAT (Russian Federation)

Instant access to the full article PDF.

Rent this article via DeepDyve

Institutional subscriptions

Similar content being viewed by others

Understanding the determinants of e-wallet continuance usage intention in Malaysia

Data breaches in healthcare: security mechanisms for attack mitigation

A Comprehensive Study of Artificial Intelligence and Cybersecurity on Bitcoin, Crypto Currency and Banking System

Kurnia, S., Peng, F., & Liu, Y. R. (2010). Understanding the adoption of electronic banking in China. In 43rd Hawaii International Conference on System Sciences , Honolulu, Hawaii, USA, pp. 1–10.

Vrîncianu, M., & Popa, L. A. (2010). Considerations regarding the security and protection of e-banking services consumers’ interests. The Amfiteatru Economic Journal , 12 (28), 388–403.

Google Scholar

Peotta, L., Holtz, M. D., David, B. M., Deus, F. G., & Timoteo de Sousa, R. (2011). A formal classification of internet banking attacks and vulnerabilities. International Journal of Computer Science and Information Technology, 3 (1), 186–197.

Article Google Scholar

Drig, I., & Isac, C. (2014). E-banking services – Features, challenges and benefits. 10.

Chavan, J. (2013). Internet banking – Benefits and challenges in an emerging economy. International Journal of Research in Business Management, 1 (1), 19–26.

MathSciNet Google Scholar

Singhal, D., & Padhmanabhan, V. (2009). A study on customer perception towards internet banking: Identifying major contributing factors. Journal of Nepalese Business Studies, 5 (1), 101–111.

Liao, S., Shao, Y. P., Wang, H., & Chen, A. (1999). The adoption of virtual banking: An empirical study. International Journal of Information Management, 19 (1), 63–74.

Bahl, D. S. (2012). E-banking: Challenges and policy implications. International Journal of Computing & Business Research , 229–6166.

Zarei, S. (2011). Risk management of internet banking. In 10th WSEAS International conference on Artificial Intelligence, Knowledge Engineering and Data Bases , Cambridge, UK, pp. 134–139.

Hanaek, P., Malinka, K., & Schafer, J. (2008). E-banking security - comparative study. In 42nd Annual IEEE International Carnahan Conference on Security Technology , Prague, Czech Republic, pp. 326–330.

Omariba, Z. B., & Masese, N. B. (2012). Security and privacy of electronic banking. International Journal of Computer Science Issues (IJCSI), 9 (4), 432–446.

Park, K. C., Shin, J. W., & Lee, B. G. (2014). Analysis of authentication methods for smartphone banking service using ANP. KSII Transactions on Internet & Information Systems, 8 (6).

Brar, T. P. S., Sharma, D., & Khurmi, S. S. (2012). Vulnerabilities in e-banking: A study of various security aspects in e-banking. International Journal of Computing & Business Research .

Yang, Y. J. (1997). The security of electronic. In International Systems Security Conference , pp. 41–52.

Yang, J., Cheng, L., & Luo, X. (2009). A comparative study on e-banking services between China and USA. International Journal of Electronic Finance, 3 (3), 235–252.

Zahid, N., Mujtaba, A., & Riaz, A. (2010). Consumer acceptance of online banking. European Journal of Economics, Finance and Administrative Sciences, 27 (1).

Geetha, K. T., & Malarvizhi, V. (2011). Acceptance of E-banking among customers: An empirical investigation in India. The Journal of Internet Banking and Commerce, 15 (2), 1–17.

Deb, M., & Lomo-David, E. (2014). An empirical examination of customers’ adoption of m-banking in India. Marketing Intelligence & Planning, 32 (4), 475–494.

Lee, J. H., Lim, W. G., & Lim, J. I. (2013). A study of the security of Internet banking and financial private information in South Korea. Mathematical and Computer Modelling, 58 (1–2), 117–131.

Moga, L., Nor, K., Neculita, M., & Khani, N. (2012). Trust and security in e-banking adoption in Romania. Communications of the IBIMA , 1–10.

Komb, F., Korau, M., Belás, J., & Korauš, A. (2016). Electronic banking security and customer satisfaction in commercial banks. Journal of Security and Sustainability Issues, 5 (3), 411–422.

Ranaweera, H. (2019). Risk of electronic payments of the banking sector in Sri Lanka: Case of Colombo district. 4 (1).

Rajaratnam, A. (2019). The factors influencing on internet banking adoption in Trincomalee District, Sri Lanka, Sri Lanka. International Research Journal of Advanced Engineering and Science, 4 (1), 160–164.

Hasan, A. S., Baten, M. A., Kamil, A. A., & Parveen, S. (2010). Adoption of e-banking in Bangladesh: An exploratory study. African Journal of Business Management, 4 (13), 2718–2727.

Jalal, A., Marzooq, J., & Nabi, H. A. (2011). Evaluating the impacts of online banking factors on motivating the process of e-banking. Journal of Management and Sustainability, 1 (1).

Abukhzam, M., & Lee, A. (2010). Factors affecting bank staff attitude towards E-banking adoption in Libya. The Electronic Journal of Information Systems in Developing Countries, 42 (1), 1–15.

Abdellatif, T., Jinene, C., & Khazmi, N. (2014). Une cartographie de la résistance à l’adoption du M-Banking en Tunisie [Mapping of resistance to the adoption of M-Banking in Tunisia]. 8 (1).

Halime, Z. F., & Kirmi, B. Etude de la résistance à l’adoption et l’utilisation de la banque mobile. Management Research .

Floh, A., & Treiblmaier, H. (2006). What keeps the e-banking customer loyal? A multigroup analysis of the moderating role of consumer characteristics on e-loyalty in the financial service industry. SSRN Electronic Journal .

Gunson, N., Marshall, D., Morton, H., & Jack, M. (2011). User perceptions of security and usability of single-factor and two-factor authentication in automated telephone banking. Computers & Security, 30 (4), 208–220.

Weir, C. S., Douglas, G., Richardson, T., & Jack, M. (2010). Usable security: User preferences for authentication methods in eBanking and the effects of experience. Interacting with Computers, 22 (3), 153–164.

Ahmad, D. T., & Hariri, M. (2012). User acceptance of biometrics in e-banking to improve security.

Tassabehji, R., & Kamala, M. A. (2009). Improving e-banking security with biometrics: Modelling user attitudes and acceptance. In 3rd International Conference on New Technologies, Mobility and Security , Cairo, Egypt, pp. 1–6.

Moeckel, C. Human-computer interaction for security research: The case of EU e-banking systems.

Rifà-Pous, H. (2009). A secure mobile-based authentication system for e-banking. In On the Move to Meaningful Internet Systems: OTM, 5871 , 848–860.

Hamidi, N. A., Mahdi Rahimi, G. K., Nafarieh, A., Hamidi, A., & Robertson, B. (2013). Personalized security approaches in e-banking employing flask architecture over cloud environment. Procedia Computer Science, 21 , 18–24.

Alsaiari, H., Papadaki, M., Dowland, P. S., & Furnell, S. M. (2014). Alternative graphical authentication for online banking environments.

Elkhodr, M., Shahrestani, S., & Kourouche, K. (2012). A proposal to improve the security of mobile banking applications. 2012 Tenth International Conference on ICT and Knowledge Engineering (pp. 260–265). IEEE: Bangkok, Thailand.

Chapter Google Scholar

Islam Khan, B. U., Olanrewaju, R. F., Anwar, F., & Yaacob, M. (2018). Offline OTP based solution for secure internet banking access. In 2018 IEEE Conference on e-Learning, e-Management and e-Services (IC3e) , Langkawi Island, Malaysia, pp. 167–172.

Brodi, D., & Jankovi, R. (2016). Usability analysis of the specific captcha types. In International Scientific Conference , pp. 272–277.

Hoonakker, P., Bornoe, N., & Carayon, P. (2009). Password authentication from a human factors perspective: Results of a survey among end-users. Human Factors and Ergonomics Society Annual Meeting Proceedings, 53 (6), 459–463.

Mridha, F., Nur, K., Kumar, A., & Akhtaruzzaman, M. (2017). A new approach to enhance internet banking security. International Journal of Computer Applications, 160 (8), 35–39.

Chandanshive, A., Sureka, A., Gongiwala, V., & Nalawade, A. (2018). Access control using 3 level authentications for e-banking. International Journal on Recent and Innovation Trends in Computing and Communication, 6 (4).

Shen, L., Zheng, N., Zheng, S., & Li, W. (2010). Secure mobile services by face and speech based personal authentication. In 2010 IEEE International Conference on Intelligent Computing and Intelligent Systems , Xiamen, China, pp. 97–100.

Onyesolu, M. O., Odoh, M., Akanwa, A. O., & Nwasor, V. C. (2010). Robust authentication model for ATM: A biometric strategy measure for enhancing e-banking security in Nigeria. International Journal of Advanced Research in Computer Science .

Bhosale, S. T. (2012). Security in e-banking via card less biometric. International Journal of Advanced Technology & Engineering Research, 2 (4), 457–462 2(2250).

Plateaux, A., Lacharme, P., Jøsang, A., & Rosenberger, C. (2014). One-time biometrics for online banking and electronic payment authentication. Availability, Reliability, and Security in Information Systems, 8708 , 179–193.

Darwish, S. M., & Hassan, A. M. (2012). A model to authenticate requests for online banking transactions. Alexandria Engineering Journal, 51 (3), 185–191.

Kumbhar, S., & Sahu, S. (2007). A new framework for online transaction using visual cryptography and steganography. International Journal of Innovative Research in Computer and Communication Engineering, 3 (11), 11418–11422.

Yaseen Khudhur, D., Saad Hameed, S., & Al-Barzinji, S. M. (2018). Enhancing e-banking security: Using whirlpool hash function for card number encryption. International Journal of Engineering & Technology, 7 (2.13).

Thompson, L. (2003). Smart card authentication: Added security for systems and network access.

Karia, A., Patankar, D. A. B., & Tawde, P. (2014). SMS-based one time password vulnerabilities and safeguarding OTP over network. International Journal of Engineering Research, 3 (5).

Al-Fairuz, M., & Renaud, K. (2010). Multi-channel, multi-level authentication for more secure eBanking.

Alarifi, A., Alsaleh, M., & Alomar, N. (2017). A model for evaluating the security and usability of e-banking platforms. Computing, 99 (5), 519–535.

Article MathSciNet Google Scholar

Download references

Author information

Authors and affiliations.

STIC Laboratory, Chouaib Doukkali University, El Jadida, Morocco

Belbergui Chaimaa, Elkamoun Najib & Hilal Rachid

You can also search for this author in PubMed Google Scholar

Corresponding author

Correspondence to Belbergui Chaimaa .

Additional information

Publisher’s Note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Reprints and permissions

About this article

Chaimaa, B., Najib, E. & Rachid, H. E-banking Overview: Concepts, Challenges and Solutions. Wireless Pers Commun 117 , 1059–1078 (2021). https://doi.org/10.1007/s11277-020-07911-0

Download citation

Accepted : 29 October 2020

Published : 28 November 2020

Issue Date : March 2021

DOI : https://doi.org/10.1007/s11277-020-07911-0

Share this article

Anyone you share the following link with will be able to read this content:

Sorry, a shareable link is not currently available for this article.

Provided by the Springer Nature SharedIt content-sharing initiative

- Authentication

- Find a journal

- Publish with us

- Track your research

- Search Search Please fill out this field.

What Is Online Banking?

How online banking works.

- Online Banks

Pros and Cons of Online Banking

What do you need for online banking, how can you safely use online banking, the bottom line.

- Personal Finance

What Is Online Banking? Definition and How It Works

:max_bytes(150000):strip_icc():format(webp)/John_Egan-9937-Editcopy-JohnEgan-e8c3407be32947ba95561ab855d13dc8.jpg "term paper of online banking")

Investopedia / Daniel Fishel

Online banking allows you to conduct financial transactions through the Internet. Online banking offers customers almost every service traditionally available through a local branch including deposits, transfers, and online bill payments.

Virtually every banking institution has some form of online banking you can access through a computer or app. Online banking is also known as internet banking or web banking.

Key Takeaways

- Online banking allows you to conduct financial transactions through a computer or smart phone using the internet.

- With online banking, you don’t need to visit a branch to complete many transactions.

- To take advantage of online banking, you’ll need an electronic device, an internet connection, and perhaps your debit card or account numbers.

Online banking is a popular way of doing business with a bank. With online banking, you aren't required to visit a bank branch to complete most of your basic banking transactions. You can do all of this at your own convenience, wherever you want—at home, at work, or on the go. Online banking can be done using a browser or app. Mobile banking is online banking that is done on a phone or tablet.

Here are some of common ways you can use online banking.

Bank anytime

With online banking, you don’t need to visit a physical bank branch but you can do it wherever you want—at home, work, or on the go. In addition, you can typically do online banking 24/7. However, customer support might not be available at all hours.

Access accounts with browsers and apps

You can do online banking through a financial institution’s web portal using a web browser (such as Chrome or Safari) through a mobile app. This allows you to access services from many locations.

Deposit Checks

You can usually deposit a check through a mobile app using a process known as remote deposit capture . Enter the check amount, then use the app to take a photo of the front and back of the check to complete the deposit.

Manage Finances

Many banks and credit unions offer tools to help you review and balance your budget built into apps or the website. You may also be able to track spending trends, or track savings toward a goal.

Perform Other Financial Services

Online banking transactions vary from one financial institution to another. Most banks generally provide essential services such as electronic transfers and bill payments. Some banks even let you set up new checking or CD accounts or apply for credit cards through web portals. Other online functions include ordering checks, stopping payments on checks, or reporting a change of address.

Online banking may provide fewer services than traditional banking does. For instance, you can’t exchange foreign currency.

You may be unable to complete a credit application online, such as a mortgage application. Instead, some banking business must be carried out at a bank or credit union branch.

Online Banks

Online banks operate exclusively online, meaning they don’t operate branches where you can conduct business in person. The best online banks offer low-cost or free banking, plus above-average interest rates on savings accounts , certificates of deposit (CDs) , and money market accounts .

These banks handle customer service by phone, email, or online chat rather than in person. Prominent online banks in the U.S. include Ally Bank , Discover Bank , and Synchrony Bank .

Online-only banks might not provide direct automatic teller machine (ATM) access but usually enable customers to use ATMs at other banks and retail stores. They might even reimburse some or all of the ATM fees other financial institutions charge. The savings gained by not maintaining physical branches typically allows online banks to deliver significant savings on banking fees.

While you can deposit or take out a certain amount of cash at an ATM or store, most online banks impose a dollar limit.

As of October 2023, just 6% of U.S. adults with bank accounts reported their primary bank was an online bank.

Fast and efficient

Easy to monitor accounts

Customer service challenges

Tech and connectivity required

Hacking risk

Pros explained:

- Convenience : Basic banking transactions can be done at any time of day or night, seven days a week. If your bank offers a payment network such as Zelle , you can use your online bank account to send money to a person or business. You can also open and close various accounts online, such as checking and savings accounts.

- Fast and efficient : Funds can be transferred between accounts almost instantly, especially if the two accounts are held at the same institution. Plus, mobile check deposits can be made in just a few minutes.

- Ease of monitoring accounts : You can closely monitor your accounts to spot suspicious activity. Around-the-clock access to banking information provides early fraud detection, serving as a guardrail against financial losses.

Cons of Online Banking

- Customer service challenges : Sometimes, you might need to visit a branch to handle certain transactions, such as buying a cashier’s check. In other cases, you might not even have access to a branch. Furthermore, you may prefer depositing checks, withdrawing money or discussing your financial needs face-to-face.

- Tech and connectivity required : Some customers may need to be more comfortable with the tech-heavy aspects of online banking. For example, they may need help with some online tasks, such as setting up automatic payments . In addition, online banking depends on a reliable internet connection. Connectivity issues make it difficult to process transactions when you want to.

- Hacking risk : Although security continually improves, online accounts remain vulnerable. Customers should use their wireless plans rather than public WiFi networks when logging into an online bank account. This can help prevent unauthorized account access.

To take advantage of online banking you’ll need an internet connection and an electronic device like a computer or mobile phone. After setting up your account, you’ll keep handy a debit or other bank card, and access to your account numbers.

Setting up your online banking account can also be reasonably straightforward. But you’ll need a few things to set up an online checking account or savings account, just like a brick-and-mortar bank account. The bank will spell out exactly what you need on its website, but it typically requires:

- Your name, date of birth, address, and other information

- Social Security number

- Government-issued ID with a photo, such as a driver’s license or passport

- A way to fund your account

To shield your money and your personal information from cyber crooks, you should take these safety precautions:

- Set a strong, unique password, and change it regularly. The federal Cybersecurity & Infrastructure Security Agency recommends a password with at least 16 characters. The password should contain a random string of uppercase letters, lowercase letters, numbers, and symbols.

- Rely on a password manager to help discreetly set and remember passwords.

- Enable two-factor authentication or multi-factor authentication if it’s available. This involves using at least two forms of identification, such as a password and a fingerprint, to access an online account.

- Never provide your online banking details to other people.

- Avoid online banking when using public WiFi, such as at a coffee shop or restaurant.

- Check your accounts regularly for suspicious activity and report suspected fraud immediately.

Can You Use Online Banking to Pay Bills?

You can use online banking to pay bills by logging into your online banking account to arrange bill payments electronically or by check. Online bill pay is a simple way to take care of your bills and help ensure you're always on time with payment by setting up automatic payments. It works especially well for bills with regular, set amounts, such as a mortgage payment, insurance premium, or car payment.

What Is the Best Online Bank?

The best online bank for you will depend on your banking service needs and priorities. Investopedia's choice for best online bank overall is Ally bank. Our top choice for savings is Synchrony Bank and our top choice for checking is Discover.

Online banking is a fast, inexpensive, and convenient way to handle many of your everyday financial needs. You can probably access online banking if you already do business with a bank or credit union. All you need to do is sign up for online banking services. And while you can use online banking features from a traditional bank, picking an online-only bank for your banking needs might boost the interest you earn on savings and help reduce fees.

Consumer Financial Protection Bureau. " Online and Mobile Banking Tips for Beginners. "

Civic Science. " Online-Only Banks Are Gaining Ground With Gen Z ."

Cybersecurity & Infrastructure Security Agency. " Use Strong Passwords ."

:max_bytes(150000):strip_icc():format(webp)/GettyImages-1469602094-b13b5453a78241329cfc05ad814504ab.jpg "term paper of online banking")

- Terms of Service

- Editorial Policy

- Privacy Policy

Term Paper on Banks (For School and College Students) | Banking

Here is a term paper on ‘Banks’ especially written for 9, 10, 11 and 12. Find paragraphs, long and short term papers on ‘Banks’ especially written for college and banking students.

Term Paper on Banks

Term Paper Contents:

- Term Paper on the Role of Banks in Economic Development

Term Paper # 1. Meaning of Bank:

ADVERTISEMENTS:

‘Bank’ is an English word. The history of the use of the term bank is very old. Even at present, the term is very popular. But there is no evidence as to time and place associated with the origin of this term. There is dissension even among scholars in this regard. Some people held that ‘Bank’ has been derived from the Italian term ‘BANCO’ which was later called ‘BANKE’ in French. On the other hand some people consider the origin of this term from the German term ‘BANCK’.

Besides these, BANQUE, BANKE and BANC etc. are also considered as mythological terms for BANK. Whatsoever be the origin of this term, all the scholars agree on the concept that the present system of banking starred in Italy. Merchants in Italy and other European Countries used to sit on benches to exchange money in ancient times. These people kept money of different places with them and could change the money (currencies) of traders in the currencies of the desired place for their convenience.

These merchants used to lend money to one another. In this regard the origin of the term BANK can be considered from ‘BANCO’ because Banco means to sit around the benches. The benches of merchants were broken into pieces if they violated their agreements or failed in their enterprises. This was how the term ‘Bankrupt’ originated.

On the other hand, ‘BANK’ means—Joint Stock fund. It means centralisation of money deposited by many people at a place.

So long as the starting of modern banking is concerned, it is supposed to have taken place in the 17 th century A.D. Bank of Amsterdam in 1609 in Holland; Bank of Hamburg in 1619 in Germany and Bank of England in 1694 were the initially set up banks in number on modern line of banks. Since then banks have been increasing gradually in different countries of the world.

Term Paper # 2. Definitions of Bank:

Today the term ‘bank’ simply means commercial banks.

The definitions of banks can be classified as follows for the convenience of study:

(A) General Definitions:

Following are important general definitions of banks:

(1) According to H. L. Hart, “A banker is one who in the ordinary course of his business receives deposits and he pays by honoring cheques.”

(2) According to Kinley, “Bank is an establishment which makes to individuals such advances of money as may be required and safely made and to which individuals entrust money when not required by them for use.”

(3) According to Sayers, “Bank as an institution whose debts, or bank- deposits is commonly accepted in final settlement of other people’s debts.”

(4) According to Crowther, “The banker’s business is to take deposits of other people, to offer his own exchange facility and there by create money.”

(B) Functional Definitions:

Following are the functional definitions of bank:

(1) According to Findly Shirras, “A banker or bank is a person or a firm or company having a place of business where credits are opened by the deposit or collection of money or currency subject to be paid or remitted upon draft, cheques of order or where money is advanced or loaned on stock, bonds, bullion and bills of exchange and promissory notes are received for discount and sale.”

(2) According to Webster’s Dictionary, “Bank is an institution which trades on money, establishment for the deposit, custody and issue of money, as also for making loans and discount and facilitating the transmission of remittances from one place to another.”

(C) Legal Definitions:

The term ‘Bank’ has been defined in the Banking Regulation Acts of various countries.

Some prominent legal definitions are given below:

(1) According to England’s Bills of Exchange Act, 1882, “Banker includes anybody or person whether incorporated or not who carry on the business of banking.”

(2) According to the Negotiable Instrument Act, 1881, “Banker includes any person acting as a banker and any post office saving bank.”

(3) According to Indian Companies Act, 1936, “A company which carries on as its principal business by accepting the deposits of money on current account or otherwise subject to withdrawal by cheque, draft or order.”

(4) According to Indian Banking Companies Act, 1949, “The accepting for the purpose of lending or investment of deposits of money from public, repayable on demand or otherwise, and withdrawable by cheque, draft, and order or otherwise.”

After a thoughtful observation of the above mentioned all definitions, we come to a conclusion that the definitions given in the general category are incomplete. Functional and legal definitions have glimpses of completion. On this basis, a proper or ideal definition of bank can be given.

(D) Proper Definition:

In a nutshell, it can be said, “A Bank is an institution that performs the task of exchanging money and credits.” But in a detailed description, we can say, “A bank is such money-dealing institution where money is deposited, loans are granted and the facility of transactions of money is provided. With these the conservation of deposits and credit formation also take place.”

Term Paper # 3. Principles of Investment Policy of Bank:

Banks invest money received through various sources at one place or the other. Banks get interest through investments and give interest on money received from share and deposits. In this condition, it becomes essential that banks should invest their resources at proper places.

The policies and principles of bank keep on changing according to the circumstances of the country. So, the bank officials have to work on the basis of their prudence and experience.

At present banks keep the following principles under consideration while investing their capital:

(1) Safety of Funds:

Safety of funds is the most important among the principles of investment policy of banks. Safety mustn’t be overlooked due to the hope of earning high profits. If banks neglect safety of funds at the time of investment, there can be problem of existence.

Banks should keep in mind following points for the safety of investment:

(i) Banks should not invest their total capital with one person, in one area, one enterprise or one industry. If it is done and that class faces some crisis, the bank would also face that crisis. So banks should invest their capital in different areas.

(ii) Before advancing loans, banks should gather information regarding the nature/character, financial position and creditworthiness of the borrowers. Loans should be always granted to persons with good character, strong financial condition and good credit. Such loans don’t become Bad Debts.

(iii) Loans should be granted on safe and proper collateral. In case, the situation of non-repayment comes up the money can be obtained by selling the collateral.

(iv) As far as possible, banks should grant short-term loans only and avoid granting long-term loans. Short-term loans are considered safe.

(v) Banks should not very often grant loan on taking immovable assets at, collateral.

(vi) Banks should not adopt Cheap Credit policy because it develops the tendency of extravagance among borrowers.

(2) Liquidity of Funds:

Faith of people is essential for the success of banks. People deposit their money with banks with the hope that they can withdraw it any time they want to do so. To retain this faith of people banks should take care of liquidity, while investing their funds.

Thus banks should invest their funds in such securities that can be sold without any loss in the hours of need. However banks retain a certain percent of cash funds to meet the demands of customers, when it appears to be inadequate there emerges, situation of the selling of shares.

The points to be considered with the view of liquidity are:

(i) Bank should not invest their total capital. Instead they must retain 20 to 30 percent as Cash Funds. Though, the Cash Fund is a passive source, it is needed to retain the faith of people.

(ii) Funds should be invested in government securities, Blue chip companies and debentures which can be sold within a short time to obtain money.

(iii) In this respect Tannen says, “A true banker is one who well understands the differences between bill of exchange and Mortgage. Bill of exchange is short-term credit investment, which can be easily converted into money in the hour of needs. But mortgage is an asset which can’t be suddenly changed into money. Due to this, demand requiring cash can’t be fulfilled at short notice.”

(3) Profitability of Funds:

A Bank is a profit earning institution. It earns the maximum of its profit from investments. So, a bank should invest its surplus capital in such a way that it can get a good and steady income.

But it is worth- mentioning here that liquidity and profitability are contradictory to each other. If investment is done by keeping liquidity in mind, it will give less profit and if investment is done with the objective of earning more profit, it will have less liquidity.

In other words, the more a bank will stress on profitability, the farther it will become from liquidity. But for banks, at the time of investment both liquidity and profitability are necessary elements of consideration. In this condition banks should invest their resources in different areas in such a way that a proper balance between liquidity and profitability can be maintained.

(4) Diversification of Risks:

Diversification of Risks in the investment policy of the banks means that banks should not invest the entire surplus amount in one enterprise, industry, area or place but diversify it. If the whole sum is invested in one area and that collapses due to any reasons, the bank would fail.

So, for the sake of safety, the banks should diversify investment of their funds. For example, if the money is to be invested in shares only, then some part of it should be invested in equity shares and the remaining in preference shares, bonds and debentures. Similarly if loans have to be granted to industries, it should be distributed to different industries.

(5) Marketability:

While investing money, banks should take care of the marketability of shares and assets. Marketability refers to the availability of markets, where shares and assets can be sold easily without any loss.

Generally market for good shares and movable property is available, so these have the quality of marketability. On the contrary, there is no market for fixed assets like land, buildings etc. So with this point of view bank should not invest their money in fixed assets.

(6) Price Stability:

However nobody knows what is stored in the future; yet banks should invest their capital on the basis of their experiences in such shares in whose price there is less fluctuation/shares with high fluctuation may give better hopes of profit, but there is also an equal chance of acquiring loss.

(7) Exemption from Tax:

For increasing their income banks should invest their surplus money in such shares, income from which is exempted from income tax and other taxes.

(8) Productivity of Funds:

While investing money as loans, banks should give top priority to production sector. If it is done so, there is safety of investment.

(9) Study of Investment Policy of Central Banks:

The Central Bank of the country is also called the bank of banks. The Central Bank regulates all the commercial banks of the country, so the commercial banks should study the investment policy of the Central Bank and take care of its guidelines.

(10) National Interest:

It is true that the objective of a bank is to earn profit, but the social responsibilities are also associated with it. So while investing banks should keep the national interest also under consideration so that the maximum national development can be achieved.

Term Paper # 4. Importance of Banks:

Banks are the lifeline of modern economy. Banks have made important contribution in the prosperity of developed countries. It is not easy to overlook banks in the present day commercial system. Today, banks are considered the ‘Nerve Centre’ of commerce, trade and industries.

The importance and utility of banks in the economic development of a country can be understood from the following points:

(1) Capital Formation:

Banks accept the deposits from people and pay interest on them. This encourages the saving tendency in people and small savings lead to big capital formation. Besides, banks also accept deposits from the people.

(2) Promotion of Trade and Industry:

Banks give economic support to people associated with trade and industries. This leads to development of trade, industries and finally of economy. Due to this liberty of banks, new entrepreneurs enter the field of trade and industries.

(3) Mobility of Capital:

Banks not only help in capital formation, but also increase the mobility of capital. Banks accept deposits from people who have surplus money and give it to those who need it. This brings a balanced development of the economy and also of the country.

(4) Transfer of Money:

People, particularly those who are associated with the trade, have the need to transfer money from one place to another. Banks perform this task at a very low cost in so many different ways. Cheque, draft, EFT, RTGS etc. facilities given by banks help in transferring of money.

(5) Discounting of Trade Bills:

Trade bills are becoming of increasing in use in India also on the line of western countries. Banks give monetary help to traders by granting immediate discounting of trade bills. Some countries have special department for this purpose which are called Discount Houses.

(6) Advancing Loans:

Banks advance a big proportion of their deposits as loans for useful purposes. Entrepreneurs make important contribution in the national economy with the help of these loans. The national development would be hampered if banks stop granting loans.

(7) Safe Custody of Valuables:

Banks grant locker facility for keeping precious metals, important documents etc. Banks charge general annual rent for this facility.

(8) Provision of Foreign Exchange:

The field of trade and commerce has developed enormously recently. Trade has also expanded in terms of export and import. Foreign currency is needed for export and import. Banks manage foreign currency for their customers and hence help them in their trade.

(9) Facility of Letter of Credit:

A Letter of Credit is that which is not money but works like money. Banks encourage cheques, drafts and other kinds of letters of Credit and thus help in the development of trading system.

(10) Help to Government:

Contribution of the role of bank for the government is also important. Collecting different kinds of taxes on behalf of the government, making governmental payments, setting government loans etc. are works with banks devote to the government.

(11) Agency Functions:

Banks work as the agents of their customers and give them chance to save their time and money. They pay insurance premium and rents and sell and purchase shares on the behalf of their customers.

(12) Aid to Trade and Industry:

Besides other work for trade and industries, bank also collect and publish data. This helps trade and industries in deciding their directions.

Term Paper # 5. Role of Banks in Economic Development :

Banks play a vital role in the economic development of underdeveloped economies in number of ways:

1. Banks promote optimum utilization of resources.

2. Banks promote growth and stability.

3. Banks promote balanced regional development.

4. Banks promote capital formation.

5. Banks promote expansion and credit.

6. Banks finance priority sectors.

(i) Banks Promote Optimum Utilization of Resources:

It is difficult to see how, in the absence of banks, could small savings of the people be mobilised or even made possible. It is also difficult to see who would distribute these savings among enterprises. It is through the agency of the banks that the community’s savings automatically flow into channels which are productive.

The banks exercise a degree of discrimination which not only ensures their own safety but which makes for optimum utilisation of the financial resources of the community. We see in India that the period of economic development has coincided with a phenomenal increase in the bank deposits and increasing advances for agricultural and industrial development.

(ii) Banks Promote Growth and Stability:

Through their influence on the rate of interest the banks can regulate the rate of investment. If cheap money is helping development at too great a speed, they will raise interest rates under the direction of the central bank. On the other hand, they can encourage investment when the speed of development has slowed down. In this way, the banks promote growth with stability.

In India, the primary function of the Reserve Bank of India was to regulate the issue of bank notes and keep adequate reserves to ensure monetary stability. But now it has assumed wider responsibilities to help in the task of economic development. In addition, to traditional responsibility of regulating currency and controlling credit, the Reserve Bank of India has been playing a vital role in financing and supervision of the development programmes for agriculture, trade, transport and industry.

It has created special funds for promoting agricultural credit and it has created special institutions for widening facilities for industrial finance. The other banks too readily fall in line. They open new branches to tap the savings of the people and lend them to entrepreneurs. An increasing degree of control is exercised in respect of management financing and development of banks so that they do not sabotage the development programmes but are made to further these programmes.

(iii) Banks Promote Balanced Regional Development:

By opening branches in backward areas the banks make credit facilities available there. Also, the funds collected in developed regions through deposits may be channelised for investment in the underdeveloped regions of the country. In this way, they bring about more balanced regional development.

(iv) Banks Promote Capital Formation:

In any plan of economic development, capital occupies a position of crucial and strategic importance. No economic development of sizable magnitude is possible unless there is an adequate degree of capital formation in the country. A very important trait of an underdeveloped economy is deficiency of capital which is due to small savings made by the community.

Backward economies hardly save 5 per cent of the national income, whereas they should save and invest at least 12 per cent in order to secure a reasonable level of development. In 1950, Colin Clark estimating the capital needs of China, India and Pakistan pointed out that they must save 12.5 percent of the national income to absorb the increasing labour force and maintain the fast rate of increase in productivity.

The role of the banks in economic development is to remove the deficiency of capital by stimulating savings and investment. A sound banking system mobilises the small and scattered savings of the people and makes them available for investment in productive enterprises.

In this connection, the banks perform two important functions:

(a) They attract deposits by offering attractive rates of interest, thus converting savings which otherwise would have remained inert into active capital, and

(b) They distribute these savings through loans among enterprises which are connected with economic development.

(v) Banks Promote Expansion and Credit:

It is recognised that to maintain a high level of economic activity, credit must expand. In an era of economic development, banks create credit more liberally and thus make funds available for the development projects. In this way, the banks make a valuable contribution to the speed and the level of economic development in the country.

(vi) Banks Finance Priority Sectors:

In order to meet additional demands arising out of economic development, the banking system has to undergo certain changes in its structure and all other financial institutions must operate in such a manner as to conform to the priorities of development and not in terms of return on their capital. The banks have now to play a more positive role.

Thus, the central bank is not merely to content itself with its regulatory role i.e., regulation of bank credit but it must play a developmental role. It must create or help to create machinery or agencies for financing development plans. It must ensure that the available finance is diverted to the right channels. For successful implementation of the development programmes it becomes necessary to make credit facilities available to high priority sectors and to see that the available funds are not squandered a way in non-essential or non-plan expenditure.

Conclusion:

The above descriptions make it clear that banks are very important for trade, commerce, industries, society and government. Banks are the basis of economic development and they serve us as the common path finder. In the present era, a society without banks is like a bloodless creature.

Related Articles:

- Term Paper on the World Bank (For School and College Students) | Banking

- Term Paper on the Central Banks (For School and Banking Students) | Banking

- Role of Banks in the Economic Development of a Country

- Term Paper on High Powered Money | Economics

| You might be using an unsupported or outdated browser. To get the best possible experience please use the latest version of Chrome, Firefox, Safari, or Microsoft Edge to view this website. |

A Glossary Of Basic Banking Terms

Updated: Jun 10, 2024, 1:35pm

Being a bank customer and navigating everyday financial transactions can introduce you to basic banking terms and plenty of financial jargon. Do you know the difference between APR and APY? What about a CD (certificate of deposit) and a money market account?

Here are some commonly used banking terms you should know to be better informed about your financial life.

Glossary of Basic Banking Terms

Account. A type of financial property or obligation held and owned under your name. When you open a financial account —whether it’s a checking account, savings account, CD or money market account—you have certain rights and responsibilities as an account holder.

ACH (Automated Clearing House). ACH is a type of electronic funds transfer system that operates between banks, businesses and individual consumers in a nationwide network. Banks use ACH payments to move money between them. When you sign up for direct deposit of your paycheck at work, that money often moves into your bank account via ACH.

APR (Annual Percentage Rate). The total annualized cost of a loan. When you borrow money, whether it’s via a credit card, car loan or another loan, the lender is required to disclose the APR, so you understand the full cost of borrowing the money.

APY (Annual Percentage Yield). The annual yield earned on a deposit account, such as a savings, money market or CD account. Savers can use APY as one of several factors to help determine which savings options are the best.

ATM (Automated Teller Machine). A convenient location for basic banking transactions, such as withdrawing cash , depositing checks or making balance inquiries. Many banks offer access to a network of fee-free ATMs.

Available balance. The amount of money you have in your bank account that is available to spend or withdraw . If you have recently deposited a check or made purchases, those transactions may still be marked as pending and may not be included in your available balance.

Cash equivalents. Highly liquid accounts holding funds that can be accessed immediately without penalty or risk of loss. Savings accounts, checking accounts and money market accounts insured by the FDIC (Federal Deposit Insurance Corporation) at banks and the NCUA (National Credit Union Administration) at credit unions are generally considered safe, liquid accounts to hold your cash.

Certificate of deposit (CD). A type of time deposit account, generally insured by the FDIC at banks and the NCUA at credit unions, where customers can put their savings to earn a yield. There are many types of CDs , but most require that you lock up your money for a minimum term, such as six months or one year. The APY that you can earn on a CD depends on the bank, the term and other factors.

Check. A type of financial instrument that instructs the check writer’s bank to make a payment to the recipient indicated on the check. Some people write paper checks and other people use their bank’s online bill pay feature to issue electronically generated checks.

Checking account. Your checking account , sometimes called a bank account, is your home base for making financial transactions. The account can be interest-bearing, or non-interest-bearing, depending on the bank or credit union.

Compound interest. When you save money in an interest-earning account, such as a savings account or CD, compound interest is the powerful financial effect that helps your savings grow over time. With compound interest, your savings multiply over time by earning interest on top of the principal plus interest, year after year.

Conditions. Also known as terms and conditions, this is the fine print of a bank account or loan agreement. Make sure you read and understand the implications of your financial accounts and obligations.

Credit/credit history/credit score . Credit generally refers to your ability to borrow—the willingness of banks and other lenders to extend a loan to you. If you have a strong credit history, that means you have a proven track record of paying bills on time and paying your debts. Your credit score is a measure of creditworthiness based, in part, on your credit history. Having a higher credit score can help you qualify for lower interest on loans, better credit terms, larger loan amounts and higher credit limits.

Debit card. This is a payment method that’s connected to your checking account. Debit cards work similarly to credit cards and can be accepted at the same points of sale, but the money you spend is deducted from your checking account balance.

Direct deposit. A payment method where people can sign up to have paychecks automatically deposited into their account without endorsing and depositing a check. Many banks offer reduced fees to customers who have recurring direct deposits.

Electronic funds transfer (EFT). A method of transferring funds between banks, businesses or individual people. Two types of EFT are the automated clearing house (ACH) network and wire transfers.

Electronic signatures. Under U.S. federal law, electronic signatures or e-signatures have the same legal validity as signatures on paper contracts. Online contracts may have the same legal status as paper contracts.

Endorsement. To cash or deposit a check , you must sign your name on the back. This is known as an endorsement.

Federal Deposit Insurance Corporation (FDIC) . The FDIC is a federal government agency that helps ensure the stability of the U.S. financial system and protects bank customers. If you deposit your money into an FDIC-insured bank account, your money is protected up to $250,000 per depositor, for each account ownership category, in the event of a bank failure.

Fraudulent charges. Many banks have strong protections against fraudulent transactions. If a suspicious transaction occurs on your account, your bank may prevent the payment from going through until they talk with you to confirm that the purchase is valid.

Grace period . A certain amount of time when a borrower can delay making a payment on a loan or credit card account without paying a penalty or incurring interest charges. It can also refer to the period after the maturity date of a certificate of deposit when you can withdraw funds without penalty.

Investments. Investments are financial assets purchased and sold by investors with the goal of earning a return on investment (ROI) . Common types of investments include stocks, bonds, mutual funds, index funds, exchange traded funds and real estate. Alternative investments include gold, commodities, fine art, wine and more. Unlike bank savings and checking accounts, investments are not FDIC insured and have a risk of loss.

Joint account. An account with two or more owners that own the account equally, with the same rights and obligations of using the account. For example, many married couples have a joint checking account that allows them both to write checks and make deposits into the same shared account.

Maturity date. This is the date of expiration for the contractual obligation of a financial instrument. For example, certificates of deposit have a maturity date that depends on the length of the CD term. When the CD matures, you have the option to withdraw the money. Some banks and credit unions also allow you to roll it into a new CD or enable the CD to renew automatically.

Money market account . A type of FDIC-insured deposit account that generally pays interest. Money market accounts tend to have higher minimum balance requirements than a typical savings account. While it is a type of savings deposit, a money market account may also offer features usually found with a checking account, such as a debit card or check-writing privileges.

Online bank. Online banks , also called digital or internet banks, operate primarily via the internet. You can manage your accounts at an online bank from a computer or mobile device from anywhere at any time.

Overdraft. Something that occurs when you make a purchase with your debit card or write a check for an amount that exceeds your checking account’s available balance. Many bank accounts offer overdraft protection to help avoid overdraft fees. Some banks don’t charge overdraft fees at all.

Savings account. A savings account may have been your first experience with the banking industry. You have a number of options for where to stow your savings safely, both at banks and credit unions.

Solvency. When banks have enough money to cover potential losses. Banks are expected to maintain a sufficient level of capital to remain solvent and avoid failure. The FDIC and other federal regulators work with banks to maintain standards for solvency.

Wire transfers. Another type of electronic funds transfer is a wire transfer that typically involves paying a fee, depending on whether the transfer is incoming or outgoing and domestic or international.

Find The Best Online Banks Of 2024

- Best CD Rates

- Best High-Yield Savings Accounts

- Best Online Banks

- Best Checking Accounts

- Best Money Market Accounts

- Best Budgeting Apps

- Best Credit Unions

- Best 5% Interest Savings Accounts

- Best Business Savings Accounts

- Best Savings Accounts For Kids

- Best No-Fee Savings Accounts

- Best Savings Accounts With Debit Cards

- Best Student Savings Accounts

- Best 1-Year CD Rates

- Best 5-Year CD Rates

- Best 3-Month CD Rates

- Best 6-Month CD Rates

- Best Jumbo CD Rates

- CD Interest Rates Forecast

- Best High-Yield Checking Accounts

- Best Business Checking Accounts

- Best Teen Checking Accounts

- Best Joint Checking Accounts

- Best No-Fee Checking Accounts

- Best Student Checking Accounts

- Best Bank Bonuses and Promotions

- Capital One Promotions

- Chase Bank Promotions

- U.S. Bank Promotions

- CIT Bank Review

- Marcus By Goldman Sachs Review

- SoFi Bank Review

- Chime Review

- Discover Bank Review

- Axos Bank Review

- Best Allowance And Chore App For Kids

- Best Debit Cards For Kids

- CD Calculator

- Budget Calculator

- Emergency Fund Calculator

- Best Places To Keep Emergency Fund

10 LGBTQ-Friendly Banks Of 2024

BMO Alto Review of 2024

Best Savings Accounts Of June 2024

Quicken Simplifi Review 2024

Credit Karma App Review 2024

Copilot Budget App Review 2024

Ben Gran is a freelance contributor for Forbes Advisor on banking. He also writes for The Ascent (a Motley Fool service), where he covers insurance, credit cards, personal finance and investing. Ben has over 10 years of experience as a freelance content writer for regional banks, tech startups, and financial services companies like LendingTree and Prudential. He also works as a ghostwriter for business executives, with bylines in publications such as Fast Company, Entrepreneur and TechCrunch.

Daphne Foreman is a former Banking and Personal Finance Analyst for Forbes Advisor. She has worked as a personal finance editor, writer, and content strategist covering banking, credit cards, insurance and investing. As a small business owner and former financial advisor, Daphne has first-hand experience with the challenges individuals face in making smart financial choices.

- Credit cards

- View all credit cards

- Banking guide

- Loans guide

- Insurance guide

- Personal finance

- View all personal finance

- Small business

- Small business guide

- View all taxes

You’re our first priority. Every time.

We believe everyone should be able to make financial decisions with confidence. And while our site doesn’t feature every company or financial product available on the market, we’re proud that the guidance we offer, the information we provide and the tools we create are objective, independent, straightforward — and free.

So how do we make money? Our partners compensate us. This may influence which products we review and write about (and where those products appear on the site), but it in no way affects our recommendations or advice, which are grounded in thousands of hours of research. Our partners cannot pay us to guarantee favorable reviews of their products or services. Here is a list of our partners .

Banking Terms and Definitions

Amber is a former banking writer for NerdWallet. Her work has been featured by USA Today, The Christian Science Monitor and The Associated Press. She holds a bachelor's degree in comparative literature from UCLA.

Erica Harrington manages the copy desk at NerdWallet. She has more than 20 years of copy-editing experience, including at the Chicago Tribune and CNN Digital. At those outlets, she edited content including business, city and state politics, arts and entertainment, and national and international affairs. Erica also has taught English as a second language at corporations in Santiago, Chile. She has produced white papers for the United Nations. She is based in Atlanta.

Many or all of the products featured here are from our partners who compensate us. This influences which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money .

When you're dealing with your finances, unfamiliar words and acronyms can make complicated processes even more confusing. Here's a quick guide to help you navigate banking terms.

Member FDIC

SoFi Checking and Savings

4.60% SoFi members with Direct Deposit or $5,000 or more in Qualifying Deposits during the 30-Day Evaluation Period can earn 4.60% annual percentage yield (APY) on savings balances (including Vaults) and 0.50% APY on checking balances. There is no minimum Direct Deposit amount required to qualify for the stated interest rate. Members without either Direct Deposit or Qualifying Deposits, during the 30-Day Evaluation Period will earn 1.20% APY on savings balances (including Vaults) and 0.50% APY on checking balances. Interest rates are variable and subject to change at any time. These rates are current as of 10/24/2023. There is no minimum balance requirement. Additional information can be found at http://www.sofi.com/legal/banking-rate-sheet.

EverBank Performance℠ Savings

on Wealthfront's website

Wealthfront Cash Account

on Betterment's website

Betterment Cash Reserve – Paid non-client promotion

5.50% *Current promotional rate; annual percentage yield (variable) is 5.50% as of 4/2/24, plus a .50% boost available as a special offer with qualifying deposit. Terms apply; if the base APY increases or decreases, you’ll get the .75% boost on the updated rate. Cash Reserve is only available to clients of Betterment LLC, which is not a bank; cash transfers to program banks conducted through clients’ brokerage accounts at Betterment Securities.

Marcus by Goldman Sachs High-Yield CD

5.10% 5.10% APY (annual percentage yield) as of 06/25/2024

Bask Bank CD

5.30% The annual percentage yield is effective as of Thursday, June 25, 2024. APY is a fixed rate and a $1,000 minimum balance is required. Bask Bank will pay this rate and APY through your CD maturity date. Fees could reduce the earnings on your account, and an early withdrawal penalty may be imposed for early withdrawal. If your CD is not funded with at least $1,000 within 10 business days after the date the account is opened, it will automatically be closed. Read the full terms here: https://www.baskbank.com/terms-and-disclosures.pdf

5.15% 5.15% APY (annual percentage yield) as of 06/25/2024

Discover® Cashback Debit

Chase Total Checking®

Deposits are FDIC Insured

Chime Checking Account

Discover® Money Market Account

Automated Clearing House, a system operated by the National Automated Clearing House Association that banks use to process electronic transfers such as direct deposits and tax refunds.

Annual percentage rate. The amount of interest you gain from keeping money in an account in a year, not including compounding interest.

Annual percentage yield. The amount of interest you gain from keeping money in an account in a year, including compounding interest.

A plastic card issued by a financial institution that gives you access to an ATM. It does not necessarily allow you to purchase items as a debit card would.

A fee that banks and interbank networks charge when you use an ATM outside your bank's network.

CASHIER'S CHECK

A check issued by a bank, usually for a fee, funded by the bank's money and signed by a cashier or teller. It may be requested by some sellers in place of a personal check to ensure the check won't bounce for lack of funds.

CERTIFICATE OF DEPOSIT

Commonly known as a CD, an account in which you deposit money for a specified length of time. The account typically pays higher interest rates than standard savings and checking accounts.

» MORE : NerdWallet's best CD rates

A way of organizing a sum of money into separate certificates of deposit of varying lengths so that they mature at different times. The method allows greater accessibility to your money than putting all of it in one certificate for a long period.

CHECKING ACCOUNT

An account at a financial institution into which you can deposit money and from which you can write checks for purchases. Most people use checking accounts to receive their wages and pay their bills.

CHEXSYSTEMS

An agency that banks use to see whether you have mishandled any accounts in the past. Banks and credit unions communicate with ChexSystems when you apply to open a new account with them.

COMPOUND INTEREST

Interest that applies to the original deposit as well as any newly earned interest. For example, if you put $100 in an account that earns compound interest at 5% a year, in the next year you will earn 5% on $105. Non-compounding interest would continue to earn 5% on $100.

CREDIT UNION

A financial institution similar to a bank that is not-for-profit and is owned by its members. Credit unions tend to have reduced fees, higher saving rates and lower loan rates than banks.

A plastic card issued by a financial institution that allows access to ATMs and can be used to pay for items at stores or online. Funds are drawn directly from your checking account.

DIRECT DEPOSIT

Money transferred directly from a payer's account to a recipient's account electronically rather than with a paper check. It is typically used for paychecks, Social Security checks, pensions or other recurring payments.

The interest paid on money in a savings account at a credit union.

DORMANT ACCOUNT

An account, usually checking, savings or money market, that has had no activity for a certain period of time, which varies from state to state. Accruing interest is not considered an activity.

EARLY CLOSURE FEE

A fee that financial institutions may charge customers for closing an account before a specified amount of time from when it was opened, usually several months.

The Federal Deposit Insurance Corporation . A government-run organization that insures customers' bank deposits up to $250,000 if the bank fails.

FOREIGN TRANSACTION FEE

An extra charge that you may incur when you use a debit, ATM or credit card in a foreign country.

INACTIVITY FEE

A fee your financial institution may charge you if you have not made any transactions in an account for a specified time.

INTEREST RATE

The rate the bank pays on the money in your accounts.

JOINT ACCOUNT

A bank account that has two owners who can access and view transactions. The accounts are commonly used by couples, parents and their teenage children, and adults assisting aging parents.

» MORE : How to write a check

LINKED ACCOUNT

A checking or savings account that's connected to another account, usually with the same owner, to facilitate transfers between the two.

MOBILE BANKING

The process of accessing or using banking products and services through a mobile device. It's usually accessed through an app your financial institution provides.

MOBILE DEPOSIT

A way to deposit checks into your bank account using your mobile device. It typically requires you to take a picture of the check and send that picture to your bank through an app.

MOBILE WALLET

A program that allows you to hold common financial items such as credit cards, debit cards or store loyalty cards in digital form on a mobile device. They are usually collected under one app.

MONEY MARKET ACCOUNT

An account similar to a savings account that typically pays higher interest rates and a higher minimum balance requirement. Some also may have limited check-writing and debit card capabilities.

MONEY ORDER

A prepaid, secure way to send money to others, issued by a bank or post office. It is a physical slip of paper and must be signed by both the sender and receiver for it to be valid.

The National Credit Union Administration. A government organization that regulates and supervises credit unions, and insures up to $250,000 worth of deposits.

Non-sufficient funds fee. A fee your bank or credit union charges when you don't have enough funds in your account to cover the amount of a check. An NSF fee means the bank rejected the check or card payment.

ONLINE BANK

A bank that is operated entirely online. Most offer higher interest rates or lower fees because they don't have to maintain branches.

OVERDRAFT FEE

A fee incurred when your checking account doesn't have enough funds to cover a payment that is requested. The financial institution will pay what your account lacks, after which your account may have a negative balance.

» MORE : Overdraft fees: What banks charge

OVERDRAFT LINE OF CREDIT

Money you borrow from your bank or credit union if you go over the amount available in your account. You will have to pay interest on the overdraft.

OVERDRAFT PROTECTION

A service offered by financial institutions that allows you to pay for an item even though you don’t have the total funds available in your account. This means your card will not be denied, but the service usually comes with a hefty fee.

PEER-TO-PEER (P2P) AND PERSON-TO-PERSON PAYMENTS

A way to send money from your checking account or credit card to another person's account through the internet. Many P2P platforms are used on mobile devices, including platforms such as Venmo, PayPal and Snapcash.

PREPAID DEBIT CARD

An alternative plastic banking card that must be loaded with money before it can be used. Only the amount put on the card may be spent. Once loaded, the card can be used like a regular debit card.

RELATIONSHIP INTEREST RATE

A higher amount of interest you can get on your checking, savings or certificate accounts, if you hold other accounts at the same financial institution. Availability depends on the financial institution.

RETURNED ITEM FEE

A bounced-check fee, charged to the person trying to deposit the check. It can be charged if there are insufficient funds in the check writer's account or the account is closed.

ROUTING NUMBER

A nine-digit number that identifies your financial institution. Larger banks may have multiple routing numbers that are based on the geographic location where the account was opened.

SAFE DEPOSIT BOX

A secured container in a vault at a bank or credit union that only its owner(s) can access. It comes with a yearly fee and can be used to store valuable items such as jewelry, keepsakes or important documents.

SAVINGS ACCOUNT

An account that usually pays interest at a financial institution that holds money you want to keep for long-term goals or emergencies.

» MORE : NerdWallet's best savings accounts

SAVINGS AND LOAN ASSOCIATION

A financial institution that accepts deposits in exchange for a share of ownership, and primarily lends money for mortgages. Deposits are insured by the FDIC for up to $250,000.

SHARE CERTIFICATE

The equivalent of a certificate of deposit for credit unions. An account in which deposits are left for a designated period of time to collect interest. Interest rates for share certificates are often higher than rates for savings and checking accounts offered at the same financial institution.

SHARE DRAFT ACCOUNT

The equivalent of a checking account for credit unions. It functions the same way as a checking account but indicates that you are a partial owner of the credit union.

STOP PAYMENT

A request you can make to your financial institution to deny a check or payment that has not cleared.

TIME ACCOUNTS

Another name for a certificate of deposit. An account that holds your money for a specified amount of time and typically offers higher interest rates than a regular savings or checking account.

WIRE TRANSFER

A quick way to send money electronically to another person, domestically or internationally, through a bank or another provider.

WITHDRAWAL LIMIT FEE

A federal limit on how many times you can transfer and withdraw money from your savings or money market account, which is six times per month. Going above the cap usually results in a charge from your financial institution.

On a similar note...

IMAGES

VIDEO

COMMENTS

Online banking , also known as internet banking, e-banking or virtual banking, is. an electronic payment system that enables customers of a bank or other financial institution to. conduct a range ...

Published: September 01, 202 3. Abstract— The study aimed to present a systematic literature Review based on scientific research extracted for the Impact of e-banking. on Customer satisfaction ...

The aim of this paper is to investigate the association and impact between online banking service practices on e-customer satisfaction, and e-customer loyalty. ... In terms of the monthly usage frequency of online banking services, 40.1% of respondents used Internet banking up to five times per month, whereas 32% used it more frequently than 5 ...

This study reviewed research articles on internet banking published during. a span of 15 years (2002 to 2016). The review adopted a multidisciplinary. approach, examining literature on internet ...

Term Paper on Online Banking - Free download as PDF File (.pdf), Text File (.txt) or read online for free. This document discusses some of the challenges of writing a thesis on online banking, including: 1) Keeping up with constant changes in the online banking industry makes it difficult to ensure research stays relevant. 2) The vast amount of information available on online banking can be ...

Term Paper on Banking and Finance - Free download as PDF File (.pdf), Text File (.txt) or read online for free. This document discusses some of the key challenges of writing a thesis on banking and finance. It notes that such a thesis requires extensive research into complex financial concepts, which can be an overwhelming task. The first challenge is choosing a relevant and feasible topic ...

Term Paper on Mobile Banking - Free download as PDF File (.pdf), Text File (.txt) or read online for free. Writing a thesis on mobile banking can be challenging due to the complex and evolving nature of the topic, the vast amount of available information, and the need for expertise across multiple disciplines like finance, economics, and computer science.

Updated: June 04, 2024. Electronic banking is the use of computers, phones, and other technologies to facilitate banking transactions rather than through human interaction. Electronic banking includes features like electronic funds transfer (EFT) and mobile payments for retail purchases, automatic teller machines (ATMs), automatic paycheck ...

The expansion of information technology has led to a new form of banking. Traditional banking, based on the physical presence of the customer, is only a part of banking activities. In the last few years, electronic banking has emerged, adopting a new distribution channels like Internet and mobile services. The main goal was to allow businesses to improve the quality of service delivery and ...

This study was undertaken to evaluate the service quality, customer sat isfaction, a nd overall consumer preference of. services in online banking. In this study, the numbers of participan ts were ...

Online Banking and Bill Payment. PAGES 7 WORDS 2337. exchange of currency have proliferated the Internet marketing world. Customers have faster and easier access to methods of exchange, deposits and payments, than ever before and the changes have come rapidly as more and more Internet commerce demands more and more ease of exchange.

Online banking allows a user to execute financial transactions via the internet. Online banking is also known as "internet banking" or "web banking." An online bank offers customers just about ...

E-banking Term Paper - Free download as PDF File (.pdf), Text File (.txt) or read online for free. e-banking term paper

Term Paper on the Role of Banks in Economic Development. Term Paper # 1. Meaning of Bank: ADVERTISEMENTS: 'Bank' is an English word. The history of the use of the term bank is very old. Even at present, the term is very popular. But there is no evidence as to time and place associated with the origin of this term.

3.1Present Security Systems for Online Ba nking. 3.1.1User id & Transaction Password: Firstly, New York introduces online banking using user id and text password. in the early 1980s. To access ...

2. Gather Research on Your Topics. The foundation of a good term paper is research. Before you start writing your term paper, you need to do some preliminary research. Take your topics with you to the library or the Internet, and start gathering research on all of the topics you're interested in.

Glossary of Basic Banking Terms. Account. A type of financial property or obligation held and owned under your name. When you open a financial account —whether it's a checking account, savings ...

Term Paper on Online Banking in Bangladesh - Free download as PDF File (.pdf), Text File (.txt) or read online for free. The document discusses the challenges of writing a thesis on online banking in Bangladesh. It notes that the topic is complex, constantly evolving, and involves a large amount of information. Researching and analyzing trends in the economic, social, cultural, and technical ...

The main objective of the study is to review the research conducted about online banking, focusing on the effect of the Covid-19 pandemic on using online banking services as a marketing channel ...

Check 21 Act. Check 21 is a Federal law that is designed to enable banks to handle more checks electronically, which is intended to make check processing faster and more efficient. Check 21 is the short name for the Check Clearing for the 21st Century Act, which went into effect on October 28, 2004.

Online Banking Term Paper - Free download as PDF File (.pdf), Text File (.txt) or read online for free. online banking term paper

C. A check issued by a bank, usually for a fee, funded by the bank's money and signed by a cashier or teller. It may be requested by some sellers in place of a personal check to ensure the check ...

e ISSN 1303-5150. 405. A Review of Cyber Security Issues in Online Banking. and Online Transactions. Dr.Bhupali shah. Asst.Prof, Pratibha Institute of Business Management Pun e, Maharashtra. ORCID ...