Don't bother with copy and paste.

Get this complete sample business plan as a free text document.

Insurance Company Business Plan

Start your own insurance company business plan

Acme Insurance

Executive summary executive summary is a brief introduction to your business plan. it describes your business, the problem that it solves, your target market, and financial highlights.">.

By focusing on its strengths, its present client base, and new value priced products in the next year, Acme Insurance plans to increase gross sales by 10% and profit by 15%.

Our Keys to Success and critical factors for the next year are, in order of importance:

- Identify “Target Markets.”

- Institute our Property inspection program.

- Begin our “Insurance Partners” program.

- Develop a profitable property program.

- Provide small businesses with an affordable basic business package.

Acme Insurance Incorporated has been profitable, but recently we have had declining market share and this must be addressed. Therefore our goals are:

- To re-establish Acme Insurance Inc. as the market leader in quality and value-priced insurance products in Smalltown District.

- Establish good working relationships with our present insurance markets by meeting with their decision makers and plotting a mutual plan for success. Get commitments for support and products that we can market in our trading area starting April 1st of Year 1.

- Investigate new markets that meet our marketing criteria by a) committing to small rural brokerage; b) providing products suitable to our economic and social climate; and c) plans for the upload and download of insurance policies.

- Provide sales incentives to staff to meet sales goals of 10%.

- Complete inspection of all Pilot homeowners within one month before renewal date.

- Formulate plans to acquire another brokerage

Acme Insurance Inc. is dedicated to providing insurance products that provide quality protection with value pricing. We wish to establish a successful partnership with our clients, our staff members, and our insurance companies, that respect the interests and goals of each party.

Success will be measured by our clients choosing us because of their belief in our ability to meet or exceed their expectations of price, service, and expertise.

In order to implement our strategic goals, we will focus on developing the following tools.

- Knowledgeable, friendly staff that can empathize with our consumers needs and circumstances, especially in handling a loss.

- Policies that meet or exceed the expectations of our clients, and that are affordable, available, and understandable.

- Policies and endorsements delivered on time with minimal errors.

- A commitment to an annual insurance review for all of our clients. A phone call is more than any direct mass marketer offers. We believe personal contact and service is the cornerstone of our success.

Acme Insurance primarily markets and services Personal Lines Insurance. Its customers are mostly rural, lower income families or long time resident senior citizens who demand value priced insurance premiums in keeping with their lower and fixed incomes.

We also provide insurance to small business, mostly family-run seasonal operations primarily focused on the tourist trade.

Acme Insurance is a privately incorporated company in the Smalltown district and is licensed to transact both Life and General Insurance. The shares are held equally by John Smith and Peter Smith.

Our Insurance and Real Estate brokerage operates from two central locations. Our modern attractive office in Smalltown, at 178 Small Street, is located in a small plaza which is owned by the principals of our brokerage. It comprises 2,000 square feet.

In Nexttown, we operate from an 800 square foot, one-story brick veneer building overlooking Lake Small, which again is owned by the principals of our firm. The office is strategically located across from the Post Office.

We have stressed to our insureds the importance of good communication between the broker and client to insure proper coverage is in place. We have noticed as our clients become better informed about insurance that there has been a tremendous increase in clients wishing in-depth discussions about their policy coverage and how they can get the most value for their insurance dollar.

Our company’s strength lies in the quality and depth of our products and staff. Our offices, unlike our competition, are open six days a week. Because of our larger staff, we are able to service our clients even when a client’s broker is busy or out of the office on inspections.

Our staff has specialists in commercial insurance that can properly service and underwrite local business. We also have some quality commercial markets unavailable to our competition.

Our Real Estate division, which is a separate company, helps with market value and replacement cost analysis when required.

The past few years have seen tremendous upheaval in the insurance industry. The number of players has decreased in both the broker and company communities. The recession has curtailed insureds from properly maintaining their homes and automobiles, and insurance fraud has become a major issue for the entire insurance industry.

Brokers are concerned that in spite of commission reductions, quotas, contract cancellations, and refusal to write new auto business by some markets, they now may find themselves in competition with some of the traditional broker distribution companies that are setting up direct marketing facilities and branches. The banks now have announced they will open stand alone insurance offices to retail insurance.

In spite of the above, we believe that the independent broker will survive. We are more automated than most service industries. We are close to the customer, regardless of some insurance companies’ attempts to sever the traditional broker-client relationship. Our clients, in most cases, still do not care or know which company we place them with. They trust our judgement in selecting the proper coverage and company to place them in.

Upload/download capabilities are in many brokers offices, including our own. This will cut costs, improve efficiency and accuracy, and help us meet the competition from banks and direct writers. Companies that truly value and trust the broker distribution system will align themselves with professional brokers and grant more underwriting authority similar to Lloyds.

Among the substitutes that are our main competition we have Local independent brokers, Agents (such as Co-operators), Mass Markets, Mass merchandise programs heavily advertised over the radio such as “Gray Power”, and Group Plans.

We have depended in the past on a small advertisement in our local newspaper, listings in the Yellow Pages, and word of mouth. However with the changes in the market today, we must begin to investigate alternate ways to put our name in front of the public. We have set out several criteria for our marketing campaign that include”

- All advertising has to emphasize our differentiation point rather than price.

- We must sell the company, not the product. In spite of some companies’ efforts to minimize the importance of the broker, our clients still identify with the broker, not the insurance company.

- We must improve and increase our contacts with our clients.

- Make contacts and support senior citizen groups and cottage associations.

Based on these changes in our goals, outlook, and company culture, we anticipate that we will be able to increase revenues substantially by year 3 of the plan and increase net profit handsomely. The company does not anticipate any cash flow problems.

1.1 Mission

Brought to you by

Create a professional business plan

Using ai and step-by-step instructions.

Secure funding

Validate ideas

Build a strategy

1.2 Objectives

- Investigating new markets that meet our marketing criteria by a) committing to small rural brokerage; b) providing products suitable to our economic and social climate; and c) plans for the upload and download of insurance policies.

- Formulate plans to acquire another brokerage.

1.3 Keys to Success

We believe the keys to success in a small town insurance business are:

Company Summary company overview ) is an overview of the most important points about your company—your history, management team, location, mission statement and legal structure.">

2.1 company ownership, 2.2 company history.

Acme Insurance was founded as a sole proprietorship in 1938 and was owned and operated by the founder Stan Smith. He originally ran the operation from his home, but moved to the business section of Smalltown when he outgrew his home based operation.

In 1972, the company constructed a new office building in the main business section and over the course of the last 15 years has purchased four other brokerages, one of which led to the establishment of our branch office in Nexttown.

In 1988, a new company was formed “Acme Insurance Inc.” which bought the insurance business from “Acme Insurance Limited.” All shares in the new company are owned by John S. Smith and Peter Smith.

Today, the fourth generation of Smiths, Stephen and Jason Smith, are working in the firm. We are also gratified to report that our founder, Stan Smith, is still in our office every day, and although still licensed, he is only active in a “goodwill ambassador” capacity.

2.3 Company Locations and Facilities

Our Smalltown operation enjoys its own private parking lot for our clients and our staff. A second story was recently added to our office which will allow ample room for expansion. It is presently used for training, staff meetings, and conferences.

Acme Insurance is committed to providing professional sales and service for its insurance customers. We have established what we consider to be an excellent reputation in our area, and are the largest multi-line insurance broker in our trading area.

3.1 Service Description

Acme Insurance provides home, automobile, and business insurance in Smalltown District. We take pride in knowing that for over 50 years we have helped our clients to find the best coverage at the right price that suits their needs and expectations. In the event of a claim, our clients know that we are there to provide help and counsel to ensure a fast, speedy claim settlement.

Like other independent brokers, we issue binders and new policies, endorsements and process renewals.

We also provide insurance services to non-clients, such as lawyers and mortgagees, to ensure our mutual clients have proper coverage and binding notes in place for the purchase of homes, businesses, and automobiles.

3.2 Competitive Comparison

Since we are brokers, (not agents such as Co-operators), we have access to a range of standard and specialty markets.

3.3 Sales Literature

We have recently produced a pamphlet titled “Insurance Partners” which stresses that a successful insurance partnership between the client, the broker, and the company is based upon a new concept.

Not only do the broker and the company take responsibility for proper protection and indemnity in the event of loss, but in the 1990’s, the client must also take his share of responsibility to insure the safety of his property by keeping it well maintained and using qualified professionals to update or change the heating, electrical, and plumbing systems in his home. We stress that multiple claims or claims arising out of poor maintenance may adversely affect his insurance.

In addition to the above, our brokerage uses a number of boilerplate letters on our computer system that are sent along with various types of policies explaining unique features or limitations in the contracts to avoid possible Errors and Omissions claims. They also encourage our clients to contact us about reviewing their coverage and promote other products and services we provide.

3.4 Fulfillment

We call upon the ample resources of our insurance markets to help with any unusual situations which occur and may present a problem finding proper coverage for our client.

When we required trained inspectors for evaluating the safety of our insured’s solid fuel heating devices and installations, we sent one of our own producers for training and who now has W.E.T.T. certification.

We are proud that Acme Insurance Inc. has never had an errors and omissions loss, but to protect our clients against that possibility, we have in place Errors and Omissions Insurance through our Insurance Brokers Association in the amount of $1,000,000 (Employer’s Reinsurance).

3.5 Technology

We have been fully computerized since 1982 and both offices and some of our producer’s homes are connected to our main computer server located in Smalltown.

As of February 1996, we have entered into an agreement with our present computer vendor, Teleglobe, to update our computer system to a Pentium server, and to Release 74, which allows upload/download capability with our companies, as well as email.

We have elected to stay with the Teleglobe Tabs system since our staff is familiar with the program. It has exhibited excellent, reliable telecommunications ability. The high speed ISDN lines required for MS Windows-based communication between our branch office as well as our home offices are not available in our trading area, so at present we will not migrate to the new MS Windows-based products available from Teleglobe or Agency Manager.

3.6 Future Services

Although Stan Smith started out as a life insurance agent, the “life” part of our business represents only 1% of our sales. We are looking to strengthen this part of our operation in the future. Due to the complexity and number of life and disability products, we are presently using an outside service: Atlantic-Smith Insurance out of North Town, although two of our general insurance producers have life agent licenses.

We are in the process of setting up a substandard property market. We feel that there is a need for this service and that it can be profitable if strictly underwritten with proper controls in place.

Market Analysis Summary how to do a market analysis for your business plan.">

Recent demographic studies in our area reveal a total year-round population of approximately 13,000, which rises in the summer to approximately 25,000. We have a relatively high number of seniors and many younger, newly-formed families dependent on government assistance living mostly in a rural, unserviced, thinly populated area. This makes it costly to service our clients. Long distance phone bills represent our second largest expense (our two offices each have their own toll free phone numbers) and the cost of visiting our insureds to do home inspections is time consuming due to the large area we service.

We are targeting seniors which have proven to be a profitable, stable market for our brokerage in spite of our present difficult economy.

We are fortunate that we have not yet had the intrusion to a large degree of mass merchandising programs like “Silver Power.” Smaller brokers have made inroads into our traditional rural business, with low cost farm markets that sell home and auto insurance. We understand that some of these markets are in a poor financial position and may cease to be a factor in the future.

4.1 Market Segmentation

Our market consists of senior citizens, lower-income young families (many of who are on social assistance) and the small, family-run business (many of which are seasonal and based on the tourist trade). There are a few industrial risks and those that are located here are branches of larger industries which obtain their insurance through large brokers in Bigtown.

Our target market is the seniors, family business, and middle income earners in our area. Statistics show that over 42% of our permanent population is above 45 years of age. The average family income is approximately $27,000 and the unemployment rate 9%.

We are cautious about encouraging business from lower income prospects since they tend to have wood heat, homes in poor repair, and many attempt to install and repair their own plumbing, wiring, and heating systems.

Another market of concern is out-of-area clients who may have been payment or claim problems to local brokers and attempt to find a distant broker to provide coverage instead of making the necessary adjustments in their own lifestyle to prevent claims.

Clients who have moved repeatedly can be difficult to obtain proper underwriting information and past claims experience on, and we feel our staff is to be commended for their ability to properly assess if a client should be placed to our standard markets or would be better served by a specialty company.

4.2 Service Business Analysis

The past few years have seen tremendous upheaval in the insurance industry. The number of players has decreased in both the broker and company communities. The automobile product has, in the mind of the public, become unaffordable, unavailable, and impossible to understand. The recession has curtailed insureds from properly maintaining their homes and automobiles, and to exacerbate the situation, many clients have turned to wood heat and started doing their own repairs and maintenance which may have increased the number and severity of claims. Insurance fraud has become a major issue for the entire insurance industry.

Our traditional close relationship with our companies has been strained. Brokers are concerned that in spite of commission reductions, quotas, contract cancellations, and refusal to write new auto business by some markets, they now may find themselves in competition with some of the traditional broker distribution companies that are setting up direct marketing facilities and branches. The banks, even though thwarted by the federal government in its last budget to retail insurance from their premises, will continue pressure on the government and now have announced they will open stand alone insurance offices to retail insurance.

The new federal government is close to adopting a new automobile contract that hopefully will make it affordable, understandable, and available to our clients. A profitable automobile product will entice the companies to aggressively seek new sales and more brokers will see companies offering contracts.

4.2.1 Main Competitors

Local independent brokers Cal Roberts, Patrick C. Johnson, Rob Champlain

- Strengths – alternate markets, especially small farm mutuals, that still continue to give low prices, still continue to write wood stoves, and allow discounts and underwriting terms such as table 1 rates on homeowners within 8 km of fire hall protection.

- Weakness – most are smaller, one-man operations that do not have the backup or finances to aggressively impact the marketplace.

- Strengths – Large advertising budget and competitively priced products. Their commercial is difficult to compete against in some cases because they seem to not have the same restrictions on underwriting as our markets. Also they have large capacity to write certain risks.

- Weakness- one small operation that does not have the same hours as our offices. Staff, because of salary, do not appear to be very knowledgeable or aggressive.

Mass Markets

- Strengths – large advertising budget and very competitive prices.

- Weakness – not local and largely unknown to our clients at the present time.

Our own Companies

- Strengths – already known to our clients; will be competitively priced.

- Weakness – an unknown quantity to our insureds. Also, if their people skills are similar to what they now exhibit, they will have great difficulty empathizing with the client and selling the client what he needs, not what they think he needs.

Mass merchandise programs heavily advertised over the radio such as “Gray Power”

- Strengths – price.

- Weakness – a still untried, unknown quantity.

Group Plans – teachers, public employees

- Strength – group pricing.

- Weakness – very little obviously, since we insure very few of the professions.

4.2.2 Competition and Buying Patterns

The main volume of income for our brokerage is generated by automobile premiums because they are relatively higher priced to insure than property, and because automobile insurance is mandatory in the region.

As stated previously, our success is dependent on our staff and our companies convincing our clients and prospective clients that price, although important, is not the only criteria for the purchase of insurance. Our advertising stresses that we have two offices, open six days a week with after-hours support and we have been an active, concerned, community involved, local business since 1938.

Still, price is very important and we must work with our markets to ensure that our insurance products are available and affordable to a large part of the market. It is the broker’s job to ensure the client understands what he is buying, and if circumstances dictate a lower-priced product, we must make our insured aware of the trade-off in coverage versus price.

4.2.3 Business Participants

- Cal Roberts Insurance

- Markets – Royal, Dominion of Canada

- Patrick C. Johnson

- Markets – General Accident, Canadian Surety

- Rob Champlain

- Markets – Farmer’s Mutual, National Frontier

- Co-Operators

- Silver Power

- Markets – Trafalger

- Con-struct Direct

4.2.4 Distributing a Service

Our trading area is rural. Premiums are relatively low and therefore not subject to large brokerages or specialty direct writers mounting aggressive advertising campaigns to bring in business. There are few group plans providing insurance coverage with the exception of our teachers. Smalltown has two independent brokers and a Co-Operators agent, Nexttown has two independent brokers, and Southtown has one. We have just started to see some move by locals to “Silver Power” and other specialty retailers who advertise on radio and television. The banks are still a future unknown.

Strategy and Implementation Summary

- Emphasize service and ongoing support . We must avoid selling only one policy at the lowest price for each customer and concentration account selling which greatly enhances client retention.

- Build an Insurance Partnership . The customer does not want to shop every year for a new broker. Concentrate on building a long term relationship with our customers and make the client and our staff appreciate the value of a long-term relationship.

- Focus on target markets . We must focus on personal and business customers that we identify and select to insure, instead of allowing potential customers to choose us, which could result in our brokerage attracting problem clients from other brokers.

5.2 Marketing Strategy

- Emphasize service and support.

- Build a partnership business based on account selling.

- Focus on senior, claims-free personal lines business and the profitable, well-run, small family business.

- Target small, non-franchise business that does not have access to group insurance plans.

- Investigate acquiring other brokerages in our area.

5.2.1 Promotion Strategy

We have depended in the past on a small advertisement in our local newspaper, listings in the Yellow Pages, and word of mouth. We must begin to investigate alternate ways to put our name in front of the public.

- All advertising has to emphasize our differentiation point rather than price. We will be developing a “Now what do I do?” message to emphasize the need for dealing with Acme’s insurance professionals so that in the event a loss occurs, you know you have the proper protection.

- We must improve and increase our contacts with our clients. All clients should be contacted before renewal to ensure covers are current and adequate. Also, new insurance should be solicited. We are investigating the production of a company newsletter or use of the I.B.A.O. newsletter which is distributed on a bi-annual basis.

- We have put our email address in our newspaper advertising, but we must be careful about attracting clients from out of the area who may be difficult to service and properly inspect.

- Make contacts and support senior citizen groups and cottage associations. Identify sports and hobby groups that involve seniors and cottagers.

5.2.2 Distribution Strategy

- Select Seniors We will give special attention to this market in our advertising. We will make a concerted effort to support and sponsor seniors programs in our area. We will seek out Cottage associations and offer support and advice to attract new senior clients who are recently retired or about to in the near future.

- Insurance Partners We will include inserts in renewal, endorsements, and correspondence stressing the importance of the insured taking an active interest and responsibility for trying to control the severity and number of claims. Our staff should take every opportunity, when discussing insurance with a client, to emphasize the consequences of multiple claims.

- Business Partners Again we should encourage insureds to take responsibility for controlling claims in partnership with their broker by installing alarm systems and continuing to maintain and upgrade their property. We should stress the benefit that good loss ratios help to control rates and ensure markets that want to write their business.

5.2.3 Positioning Statement

Our target market is Smalltown District. The ideal client is claims-free aged between 45 – 75 who owns his own home and car and is debt free. Has exhibited stable family patterns and is known and respected in the community.

A similar profile should be used for commercial prospects with emphasis placed on the well-run, profitable business that has exhibited good claims experience.

5.2.4 Pricing Strategy

Our customers are especially sensitive to value. We must ensure that our price and service are perceived to be good value to our client.

Our markets must offer several payment options to our clients that are convenient to the client, not just to the company. Example – payment on insured’s preferred day of month, not on the company’s, and accepting payment by credit or debit card. Many insureds are on a fixed income and receive their income on a set day of each month or a paycheck on a particular day.

We encourage our companies to “Target Market.” Many of our companies are now focusing on what they have perceived to be profitable niche markets, where they can offer a competitive product with little, if any, competition.

We are seeing our commercial markets now moving toward basic coverage and limiting the “bells and whistles,” all-risk products available to only those clients who have modern, well-managed, profitable, low-risk operations. This should help stabilize pricing and, even more important, ensure that there is an insurance market available for most risks. Continued insistence by the industry on better protection, i.e. fire and burglar alarms, upgrading of buildings, etc., have started to lower loss ratios.

Many of the larger insurance markets have increased minimum premiums to $1,000 for any commercial package policy. Our Lloyds market should be able to accommodate these customers with a minimum premium of approximately $600.

5.3 Sales Strategy

We want to emphasize the benefit of dealing with professionals who live and work in our client’s area. We know their needs and their problems and we have a local reputation to protect, unlike an out-of-town market. If the out-of-town broker fails to provide proper cover or advice, they lose one client. We could stand to lose many if the public perceives a professional failure on our part.

Competitive prices for our identified target markets. Discounts of up to 25% for claims-free seniors who renew their home insurance with us.

Careful inspection and the judicious use of deductibles and warranties for insureds using wood stoves should help alleviate company concerns about solid fuel heating devices. Competitive pricing is not an important factor to attract business because competition is very limited for primary wood heat houses in our area. This may provide a chance to pick up all of the insured’s business because, in many instances, they contact us after being told by their previous broker that, in spite of their claims-free status, the broker doesn’t want their house insurance.

Business partners provide us the opportunity to sell lower-priced, basic insurance coverage to our client. Many clients have expressed interest in retaining part or all of the insurance risk, especially for burglary. They feel that if they have installed central alarms and bars, they can take the chance of self insurance.

5.3.1 Sales Programs

We are investigating sales incentives for our producers. They must encourage profitable new business and have a retention component. Presently, our producers receive $10 for every new policy written in our office, with the exception of recreational vehicles.

5.3.2 Sales Forecast

The following table and related charts show our present sales forecast. We are projecting sales to grow at a moderate but steady pace for the coming year and to continue into 1997.

5.4 Strategic Alliances

Some of our present companies have surveyed us to investigate co-operative advertising but we have not committed to any programs at present.

5.5 Service and Support

Acme Insurance is really a group of small brokerages housed under one name and location. Our producers are each responsible for a book of business. They sell, service, handle claims and are responsible for their accounts receivable. We have found over the years that our clients prefer to deal with one broker who is aware of their particular needs.

5.6 Milestones

We have listed our plan milestones in the table below.

5.7 Service and Support

Management summary management summary will include information about who's on your team and why they're the right people for the job, as well as your future hiring plans.">.

Acme Insurance is slow to hire new people and loyal to those whom we have hired. We hire only when there is a vacancy or growth dictates more staff. Most of our people have been in our organization over 15 years, which allows our clients and our companies to form long lasting business relationships with their broker.

6.1 Organizational Structure

Our brokerage is divided by client instead of service. Each broker is responsible not only to renew and service a client’s insurance, they also are responsible for collection and claims. We feel a client wants to deal with his or her broker, especially in a claim situation, instead of an unknown “specialist” whom they feel does not represent their interests.

The quickest way to turn a business idea into a business plan

Fill-in-the-blanks and automatic financials make it easy.

No thanks, I prefer writing 40-page documents.

Discover the world’s #1 plan building software

How To Write an Insurance Company Business Plan + Template

Creating a business plan is essential for any business, but it can be especially helpful for insurance companies that want to improve their strategy and/or raise funding.

A well-crafted business plan not only outlines the vision for your company, but also documents a step-by-step roadmap of how you are going to accomplish it. In order to create an effective business plan, you must first understand the components that are essential to its success.

This article provides an overview of the key elements that every insurance company owner should include in their business plan.

Download the Ultimate Insurance Business Plan Template

What is an Insurance Company Business Plan?

An insurance company business plan is a formal written document that describes your company’s business strategy and its feasibility. It documents the reasons you will be successful, your areas of competitive advantage, and it includes information about your team members. Your business plan is a key document that will convince investors and lenders (if needed) that you are positioned to become a successful venture.

Why Write an Insurance Company Business Plan?

An insurance company business plan is required for banks and investors. The document is a clear and concise guide of your business idea and the steps you will take to make it profitable.

Entrepreneurs can also use this as a roadmap when starting their new company or venture, especially if they are inexperienced in starting a business.

Writing an Effective Insurance Company Business Plan

The following are the key components of a successful insurance company business plan:

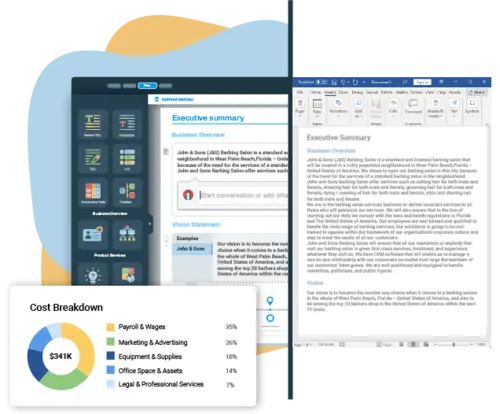

Executive Summary

The executive summary of an insurance company business plan is a one to two page overview of your entire business plan. It should summarize the main points, which will be presented in full in the rest of your business plan.

- Start with a one-line description of your insurance company

- Provide a short summary of the key points in each section of your business plan, which includes information about your company’s management team, industry analysis, competitive analysis, and financial forecast among others.

Company Description

This section should include a brief history of your company. Include a short description of how your company started, and provide a timeline of milestones your company has achieved.

If you are just starting your insurance company , you may not have a long company history. Instead, you can include information about your professional experience in this industry and how and why you conceived your new venture. If you have worked for a similar company before or have been involved in an entrepreneurial venture before starting your insurance company firm, mention this.

You will also include information about your chosen insurance company business model and how, if applicable, it is different from other companies in your industry.

Industry Analysis

The industry or market analysis is an important component of an insurance company business plan. Conduct thorough market research to determine industry trends and document the size of your market.

Questions to answer include:

- What part of the insurance industry are you targeting?

- How big is the market?

- What trends are happening in the industry right now (and if applicable, how do these trends support the success of your company)?

You should also include sources for the information you provide, such as published research reports and expert opinions.

Customer Analysis

This section should include a list of your target audience(s) with demographic and psychographic profiles (e.g., age, gender, income level, profession, job titles, interests). You will need to provide a profile of each customer segment separately, including their needs and wants.

For example, the customers of an insurance company may include individuals, families, small businesses, and large corporations.

You can include information about how your customers make the decision to buy from you as well as what keeps them buying from you.

Develop a strategy for targeting those customers who are most likely to buy from you, as well as those that might be influenced to buy your products or insurance company services with the right marketing.

Competitive Analysis

The competitive analysis helps you determine how your product or service will be different from competitors, and what your unique selling proposition (USP) might be that will set you apart in this industry.

For each competitor, list their strengths and weaknesses. Next, determine your areas of competitive differentiation and/or advantage; that is, in what ways are you different from and ideally better than your competitors.

Below are sample competitive advantages your insurance company may have:

- Specialized industry knowledge

- Proven track record

- Strong customer relationships

- Robust product offerings

- Innovative solutions

Marketing Plan

This part of the business plan is where you determine and document your marketing plan. . Your plan should be clearly laid out, including the following 4 Ps.

- Product/Service : Detail your product/service offerings here. Document their features and benefits.

- Price : Document your pricing strategy here. In addition to stating the prices for your products/services, mention how your pricing compares to your competition.

- Place : Where will your customers find you? What channels of distribution (e.g., partnerships) will you use to reach them if applicable?

- Promotion : How will you reach your target customers? For example, you may use social media, write blog posts, create an email marketing campaign, use pay-per-click advertising, launch a direct mail campaign.

- Or, you may promote your insurance company business via word of mouth.

Operations Plan

This part of your insurance company business plan should include the following information:

- How will you deliver your product/service to customers? For example, will you do it in person or over the phone only?

- What infrastructure, equipment, and resources are needed to operate successfully? How can you meet those requirements within budget constraints?

The operations plan is where you also need to include your company’s business policies. You will want to establish policies related to everything from customer service to pricing, to the overall brand image you are trying to present.

Finally, and most importantly, in your Operations Plan, you will lay out the milestones your company hopes to achieve within the next five years. Create a chart that shows the key milestone(s) you hope to achieve each quarter for the next four quarters, and then each year for the following four years. Examples of milestones for an insurance company include reaching $X in sales. Other examples include expanding to a new geographic market, launching a new product or service line, or signing on new major customers.

Management Team

List your team members here including their names and titles, as well as their expertise and experience relevant to your specific insurance industry. Include brief biography sketches for each team member.

Particularly if you are seeking funding, the goal of this section is to convince investors and lenders that your team has the expertise and experience to execute on your plan. If you are missing key team members, document the roles and responsibilities you plan to hire for in the future.

Financial Plan

Here you will include a summary of your complete and detailed financial plan (your full financial projections go in the Appendix).

This includes the following three financial statements:

Income Statement

Your income statement should include:

- Revenue : how much revenue you generate.

- Cost of Goods Sold : These are your direct costs associated with generating revenue. This includes labor costs, as well as the cost of any equipment and supplies used to deliver the product/service offering.

- Net Income (or loss) : Once expenses and revenue are totaled and deducted from each other, this is the net income or loss.

Sample Income Statement for a Startup Insurance Company

Balance sheet.

Include a balance sheet that shows your assets, liabilities, and equity. Your balance sheet should include:

- Assets : All of the things you own (including cash).

- Liabilities : This is what you owe against your company’s assets, such as accounts payable or loans.

- Equity : The worth of your business after all liabilities and assets are totaled and deducted from each other.

Sample Balance Sheet for a Startup Insurance Company

Cash flow statement.

Include a cash flow statement showing how much cash comes in, how much cash goes out and a net cash flow for each year. The cash flow statement should include:

- Cash Flow From Operations

- Cash Flow From Investments

- Cash Flow From Financing

Below is a sample of a projected cash flow statement for a startup insurance company business.

Sample Cash Flow Statement for a Startup Insurance Company

You will also want to include an appendix section which will include:

- Your complete financial projections

- A complete list of your company’s business policies and procedures related to the rest of the business plan (marketing, operations, etc.)

- Any other documentation which supports what you included in the body of your business plan.

Writing a good business plan gives you the advantage of being fully prepared to launch and/or grow your insurance company . It not only outlines your business vision but also provides a step-by-step process of how you are going to accomplish it. All in all, a business plan is a key to the success of any business.

Finish Your Insurance Business Plan in 1 Day!

Other helpful articles.

How To Write an Insurance Agency Business Plan + Template

Researched by Consultants from Top-Tier Management Companies

Powerpoint Templates

Icon Bundle

Kpi Dashboard

Professional

Business Plans

Swot Analysis

Gantt Chart

Business Proposal

Marketing Plan

Project Management

Business Case

Business Model

Cyber Security

Business PPT

Digital Marketing

Digital Transformation

Human Resources

Product Management

Artificial Intelligence

Company Profile

Acknowledgement PPT

PPT Presentation

Reports Brochures

One Page Pitch

Interview PPT

All Categories

Top 5 Insurance Business Plan Templates with Examples and Samples

Success in the insurance business is not about avoiding risks, but rather understanding and managing them effectively.

- Warren Buffett

With his remarkable business acumen, Warren Buffett shares a profound quote that captures the essence of what it takes to succeed in the insurance industry. In a world filled with uncertainties, insurance serves as a safety net, providing individuals and businesses with financial protection against unforeseen events.

Insurance agency leans on insurance business plan templates as their trusted allies, helping them through the complexities of the industry. These templates offer an insurance broker/ insurance agency structured framework to clearly define goals, strategies, and financial projections.

In this blog post, we are here to lend a helping hand and introduce you to some of the best insurance business plan templates. Whether you're venturing into a new start-up in some type of insurance like, home, life, health, automobile insurance or seeking to revamp your current insurance plan, these templates will serve as your guiding star by unveiling the finest selection of insurance business plan templates.

Elevate Your Planning with These Top 5 Insurance Business Plan Templates

Template 1 - insurance business plan powerpoint presentation slides.

This insurance business plan template presents a captivating blend of functionality and aesthetics. This content-ready PPT slide showcases the critical success factors, mission, vision, and start-up summary, while also incorporating a potential growth analysis, including SWOT analysis and Porter's five force analysis model, customer analysis, and market sizing. While adopting an appealing color palette of soothing blues, vibrant yellows, and sophisticated greys, this engaging color blend evokes a sense of trust, professionalism, and stability that are essential attributes in the insurance industry and also instils confidence in your brand. Check out more about this template here.

Download Now!

Template 2 - Insurance Business Plan Word Document Template

Designed with meticulous attention to detail, this template offers a versatile solution for insurance agencies, brokers, and professionals. It includes comprehensive sections covering every vital aspect of an insurance business plan. It encompasses market analysis, target audience identification, marketing strategies, financial projections, risk assessment, and growth plans. Its inclusive approach ensures a thorough and well-rounded plan. Get your hands on it now and leave your audience in awe with each and every delivery.

Template 3 - Insurance Business Plan PowerPoint Template Bundles

This template offers twelve slides with high-quality visuals, graphics, and images to showcase your expertise effectively. Each slide focusses different aspects of insurance, making information interpretation easier for your audience. The well-researched content stimulates strategic thinking, ensuring your message is conveyed with ease. The design's standout feature is its editable elements, allowing customization of colors, fonts, backgrounds, and more. Grab this template now for unique and captivating presentations every time.

Template 4 - Market Share Assessment for Insurance Business Plan

This ready to use PPT template is expertly designed to highlight market share assessment for an insurance business plan. It consists of a pre-built pie-chart to exhibit the scenario of a market place of insurance companies. Discuss different insurance market characteristics and help your audience make informed decision with this pre-designed PPT slide. Grab your copy now and confidently deliver a persuasive presentation that convinces your audience.

Template 5 - Business Insurance Actionable Steps Template

This ready-made PPT template covers the usage of insurance plan for organizations. Use this flexible PPT diagram and craft a compelling presentation to persuade your audience to invest in different insurance options that safeguard their finances and assets. It offers a structured approach, ensuring that the plan aligns with goals and captures the attention of stakeholders. With its visually appealing design, compelling graphics, and concise text, convey complex information in a clear and impactful manner.

Using business plan templates for an insurance broker agency is a game-changer. It streamlines the planning process, ensuring a clear roadmap for success. We have highlighted the top 5 insurance business plan templates and examples, showcasing their effectiveness in guiding your business strategy. Don't miss out on this opportunity to leverage these templates as a springboard for your own business plans, tailoring them to suit your unique goals. For further assistance, we recommend exploring additional resources and tools that can enhance your business planning journey. Check out this page to unlock your agency or brokerage's full potential.

FAQs on Insurance Business Plan

What is an insurance business plan.

An insurance business plan is a detailed roadmap that outlines the goals, strategies, and operations of an insurance company. It holds significant value in the insurance field to set clear objectives, identify target markets, and determine financial projections. For insurance startups, strong business insurance guides the company, lures investors, and ensures essential licenses.

How to start an insurance startup?

To start an insurance agency, one can conduct thorough market research, define your target audience, obtain necessary licenses, develop a comprehensive insurance business plan, establish strategic partnerships, leverage technology, and create a marketing strategy. Adapt and evolve

your strategies to seize industry opportunities.

What are the 4 types of insurance?

The four types of insurance are Health, Life, Home & Automobile insurance. Health insurance helps with medical expenses, life, and annuity insurance provides financial support to loved ones after you pass away, home/property and casualty insurance covers damage or theft of your property, and automobile insurance protects against car accidents.

What are the 7 main types of insurance?

The seven main types of insurance are Property, Marine, Fire, Liability, Guarantee, Social & Life, and annuity insurance. These cover various aspects, including financial support after death, coverage for marine-related risks, liability-related risks, guarantees, social welfare benefits, and protection for damaged assets and personnel injuries by taking property and casualty insurance.

Related posts:

- How to Design the Perfect Service Launch Presentation [Custom Launch Deck Included]

- Quarterly Business Review Presentation: All the Essential Slides You Need in Your Deck

- [Updated 2023] How to Design The Perfect Product Launch Presentation [Best Templates Included]

- 99% of the Pitches Fail! Find Out What Makes Any Startup a Success

Liked this blog? Please recommend us

Must-Have Technology Brochure Examples with Templates and Samples

Top 10 Sales Content Management Playbook Templates with Samples and Examples

2 thoughts on “top 5 insurance business plan templates with examples and samples”.

This form is protected by reCAPTCHA - the Google Privacy Policy and Terms of Service apply.

Digital revolution powerpoint presentation slides

Sales funnel results presentation layouts

3d men joinning circular jigsaw puzzles ppt graphics icons

Business Strategic Planning Template For Organizations Powerpoint Presentation Slides

Future plan powerpoint template slide

Project Management Team Powerpoint Presentation Slides

Brand marketing powerpoint presentation slides

Launching a new service powerpoint presentation with slides go to market

Agenda powerpoint slide show

Four key metrics donut chart with percentage

Engineering and technology ppt inspiration example introduction continuous process improvement

Meet our team representing in circular format

Insurance Business Plan Template

Written by Dave Lavinsky

Business Plan Outline

- Insurance Business Plan Home

- 1. Executive Summary

- 2. Company Overview

- 3. Industry Analysis

- 4. Customer Analysis

- 5. Competitive Analysis

- 6. Marketing Plan

- 7. Operations Plan

- 8. Management Team

- 9. Financial Plan

Insurance Agency Business Plan

You’ve come to the right place to create your own business plan.

We have helped over 100,000 entrepreneurs and business owners create business plans and many have used them to start or grow their insurance companies.

Essential Components of a Business Plan For an Insurance Agency

Below we describe what should be included in each section of a business plan for a successful insurance agency and links to a sample of each section:

- Executive Summary – In the Executive Summary, you will provide a high-level overview of your business plan. It should include your agency’s mission statement, as well as information on the products or services you offer, your target market, and your insurance agency’s goals and objectives.

- Company Overview – This section provides an in-depth company description, including information on your insurance agency’s history, ownership structure, and management team.

- Industry Analysis – Also called the Market Analysis, in this section, you will provide an overview of the industry in which your insurance agency will operate. You will discuss trends affecting the insurance industry, as well as your target market’s needs and buying habits.

- Customer Analysis – In this section, you will describe your target market and explain how you intend to reach them. You will also provide information on your customers’ needs and buying habits.

- Competitive Analysis – This section will provide an overview of your competition, including their strengths and weaknesses. It will also discuss your competitive advantage and how you intend to differentiate your insurance agency from the competition.

- Marketing Plan – In this section, you will detail your marketing strategy, including your advertising and promotion plans. You will also discuss your pricing strategy and how you intend to position your insurance agency in the market.

- Operations Plan – This section will provide an overview of your agency’s operations, including your office location, hours of operation, and staff. You will also discuss your business processes and procedures.

- Management Team – In this section, you will provide information on your insurance agency’s management team, including their experience and qualifications.

- Financial Plan – This section will detail your insurance agency’s financial statements, including your profit and loss statement, balance sheet, and cash flow statement. It will also include information on your funding requirements and how you intend to use the funds.

Next Section: Executive Summary >

Insurance Agency Business Plan FAQs

What is an insurance agency business plan.

An insurance agency business plan is a plan to start and/or grow your insurance business. Among other things, it outlines your business concept, identifies your target customers, presents your marketing plan and details your financial projections.

You can easily complete your insurance agency business plan using our Insurance Agency Business Plan Template here .

What Are the Main Types of Insurance Companies?

There are a few types of insurance agencies. Most companies provide life and health insurance for individuals and/or households. There are also agencies that specialize strictly in auto and home insurance. Other agencies focus strictly on businesses and provide a variety of liability insurance products to protect their operations.

What Are the Main Sources of Revenue and Expenses for an Insurance Agency Business?

The primary source of revenue for insurance agencies are the fees and commissions paid by the client for the insurance products they choose.

The key expenses for an insurance agency business are the cost of purchasing the insurance, licensing, permitting, and payroll for the office staff. Other expenses are the overhead expenses for the business office, utilities, website maintenance, and any marketing or advertising fees.

How Do You Get Funding for Your Insurance Agency Business Plan?

Insurance agency businesses are most likely to receive funding from banks. Typically you will find a local bank and present your business plan to them. Other options for funding are outside investors, angel investors, and crowdfunding sources. This is true for a business plan for insurance agent or an insurance company business plan.

What are the Steps To Start an Insurance Business?

Starting an insurance business can be an exciting endeavor. Having a clear roadmap of the steps to start a business will help you stay focused on your goals and get started faster.

1. Develop An Insurance Business Plan - The first step in starting a business is to create a detailed insurance business plan that outlines all aspects of the venture. This should include potential market size and target customers, the services or products you will offer, pricing strategies and a detailed financial forecast.

2. Choose Your Legal Structure - It's important to select an appropriate legal entity for your insurance business. This could be a limited liability company (LLC), corporation, partnership, or sole proprietorship. Each type has its own benefits and drawbacks so it’s important to do research and choose wisely so that your insurance business is in compliance with local laws.

3. Register Your Insurance Business - Once you have chosen a legal structure, the next step is to register your insurance business with the government or state where you’re operating from. This includes obtaining licenses and permits as required by federal, state, and local laws.

4. Identify Financing Options - It’s likely that you’ll need some capital to start your insurance business, so take some time to identify what financing options are available such as bank loans, investor funding, grants, or crowdfunding platforms.

5. Choose a Location - Whether you plan on operating out of a physical location or not, you should always have an idea of where you’ll be based should it become necessary in the future as well as what kind of space would be suitable for your operations.

6. Hire Employees - There are several ways to find qualified employees including job boards like LinkedIn or Indeed as well as hiring agencies if needed – depending on what type of employees you need it might also be more effective to reach out directly through networking events.

7. Acquire Necessary Insurance Equipment & Supplies - In order to start your insurance business, you'll need to purchase all of the necessary equipment and supplies to run a successful operation.

8. Market & Promote Your Business - Once you have all the necessary pieces in place, it’s time to start promoting and marketing your insurance business. This includes creating a website, utilizing social media platforms like Facebook or Twitter, and having an effective Search Engine Optimization (SEO) strategy. You should also consider traditional marketing techniques such as radio or print advertising.

Learn more about how to start a successful insurance business:

- How to Start an Insurance Business

Where Can I Get an Insurance Business Plan PDF?

You can download our free insurance business plan template PDF here . This is a sample insurance business plan template you can use in PDF format.

Upmetrics AI Assistant: Simplifying Business Planning through AI-Powered Insights. Learn How

- AI ASSISTANTS

Upmetrics AI Your go-to AI-powered business assistant

AI Writing Assist Write, translate, and refine your text with AI

AI Financial Assist Automated forecasts and AI recommendations

- TOP FEATURES

AI Business Plan Generator Create business plans faster with AI

Financial Forecasting Make accurate financial forecasts faster

Strategic Planning Develop actionable strategic plans on-the-go

AI Pitch Deck Generator Use AI to generate your investor deck

See how it works →

AI-powered business planning software

Very useful business plan software connected to AI. Saved a lot of time, money and energy. Their team is highly skilled and always here to help.

- Julien López

- BY USE CASE

Starting & Launching a Business Plan your business for launch and success

Validate Your Business Idea Discover the potential of your business idea

Secure Funding, Loans, Grants Create plans that get you funded

Business Consultant & Advisors Plan seamlessly with your team members and clients

Business Schools & Educators Simplify business plan education for students

Students & Learners Your e-tutor for business planning

- Sample Plans

- WHY UPMETRICS?

Reviews See why customers love Upmetrics

Customer Success Stories Read our customer success stories

Blogs Latest business planning tips and strategies

Strategic Planning Templates Ready-to-use strategic plan templates

Business Plan Course A step-by-step business planning course

Ebooks & Guides A free resource hub on business planning

Business Tools Free business tools to help you grow

- Sample Business Plans

- Finance & Investing

Insurance Company Business Plan

An insurance agency can become a profitable business if done right. After all, insurance companies as a business help people deal with uncertainties, and that is something all of us want.

And if you have good negotiation skills, are brilliant at planning, and have a thorough knowledge of how insurance works then you might have thought of having your insurance agency.

If yes, then what are you waiting for?

Get started because now is a time as good as any. All you need is a little industry information and an insurance company business plan to help you have a thriving business.

Industry Overview

The global insurance industry stands at a whopping value of 5.3 trillion US dollars in 2022 and is expected to grow at a rapid pace going forward too.

The major reason for the growth of the insurance sector comes from the increasing uncertainty of life, property, and everything else that concerns people.

The increase in disposable income amongst people has also contributed significantly to the growth of the sector.

But as everything good attracts competition, the insurance industry attracts a lot of competition too. And if you want to stand out amongst all of it, you’ll need to be brilliant at what you do. Proper steps to set up your business and planning can help you with that.

Say goodbye to boring templates

Build your business plan faster and easier with AI

Plans starting from $7/month

Things to Consider Before Writing Your Insurance Company Business Plan

Know the industry.

The first step towards having a successful business is to research the industry and know what you are getting yourself into. It helps you understand the ins and outs of the business and what steps you should take to help your business succeed. It also helps you stay updated with the latest trends and use them to your advantage.

Get the necessary licenses and permits

As insurance companies are prone to lawsuits, fraud, and other such problems, having all the necessary documents can help you stay on the right side of the law. The licenses and permits act as an assurance for both your clients and your business that you’ll be able to deal with any legal hassle that comes your way. And as you don’t need to worry about the legalities you can focus on what really matters.

Know your audience

Knowing your target audience, their fears, motivations, and preferences can give you the required edge over your competitors. As you know your customers you’re able to serve them better. This eventually makes them return to you and build long-term and mutually beneficial relationships with your customers.

Promote your business

Promoting your business is foundational to success because for your business to work you need to let people know that your business exists. Hence, once you get to know your target audience, it is important to promote your business in a way that speaks to your target audience.

Chalking out Your Business Plan

If you are planning to start a new insurance company, the first thing you will need is a business plan. Use our sample insurance company business plan created using Upmetrics business plan software to start writing your business plan in no time.

Before you start writing your business plan for your new insurance business, spend as much time as you can reading through some examples of insurance-related business plans .

Reading sample business plans will give you a good idea of what you’re aiming for and also it will show you the different sections that different entrepreneurs include and the language they use to write about themselves and their business plans.

We have created this sample insurance company business plan for you to get a good idea about what a perfect insurance business plan should look like and what details you will need to include in your stunning business plan.

Insurance Company Business Plan Outline

This is the standard insurance company business plan outline which will cover all important sections that you should include in your business plan.

- Keys to Success

- 3 Year profit forecast

- Startup cost

- Funding Required

- Company Ownership

- Company Locations and Facilities

- Service Description

- Competitive Comparison

- Sales Literature

- Fulfillment

- Future Services

- Market Analysis

- Competition and Buying Patterns

- Business Participants

- Distributing a Service

- Cal Roberts, Patrick C. Johnson, Rob Champlain

- Agents (such as Co-operators)

- Mass Markets

- Group Plans – teachers, public employees

- Promotion Strategy

- Distribution Strategy

- Positioning Statement

- Pricing Strategy

- Sales Programs

- Sales Forecast

- Sales Yearly

- Strategic Alliances

- Service and Support

- Organizational Structure

- Startup Funding

- Important Assumptions

- Brake-even Analysis

- Profit Yearly

- Gross Margin Yearly

- Projected Cash Flow

- Projected Balance Sheet

- Business Ratios

After getting started with Upmetrics , you can copy this sample business plan into your business plan and modify the required information and download your insurance company business plan pdf or doc file. It’s the fastest and easiest way to start writing your business plan.

The Quickest Way to turn a Business Idea into a Business Plan

Fill-in-the-blanks and automatic financials make it easy.

Download a sample insurance company business plan

Need help writing your business plan from scratch? Here you go; download our free insurance company plan pdf to start.

It’s a modern business plan template specifically designed for your insurance company business. Use the example business plan as a guide for writing your own.

Related Posts

Holding Company Business Plan

Insurance Agent Business Plan

Financial Plan for Startup Guide

Sample Business Plans Free Template

About the Author

Upmetrics Team

Upmetrics is the #1 business planning software that helps entrepreneurs and business owners create investment-ready business plans using AI. We regularly share business planning insights on our blog. Check out the Upmetrics blog for such interesting reads. Read more

Plan your business in the shortest time possible

No Risk – Cancel at Any Time – 15 Day Money Back Guarantee

Popular Templates

Create a great Business Plan with great price.

- 400+ Business plan templates & examples

- AI Assistance & step by step guidance

- 4.8 Star rating on Trustpilot

Streamline your business planning process with Upmetrics .

Insurance Agency Business Plan Template

Written by Dave Lavinsky

Over the past 20+ years, we have helped over 3,000 entrepreneurs and business owners create business plans to start and grow their insurance agencies. On this page, we will first give you some background information with regards to the importance of business planning. We will then go through an insurance agency business plan template step-by-step so you can create your plan today.

Download our Ultimate Insurance Business Plan Template here >

What is an Insurance Agency Business Plan?

A business plan provides a snapshot of your insurance agency as it stands today, and lays out your growth plan for the next five years. It explains your business goals and your strategy for reaching them. It also includes market research to support your plans.

Why You Need a Business Plan for an Insurance Agency

If you’re looking to start an insurance agency or grow your existing insurance agency you need a business plan. A business plan will help you raise funding, if needed, and plan out the growth of your insurance agency in order to improve your chances of success. Your insurance agency business plan is a living document that should be updated annually as your agency grows and changes.

Source of Funding for Insurance Agencies

With regards to funding, the main sources of funding for an insurance agency are personal savings, credit cards, bank loans, and angel investors. With regards to bank loans, banks will want to review your business plan and gain confidence that you will be able to repay your loan and interest. To acquire this confidence, the loan officer will not only want to confirm that your financials are reasonable. But they will want to see a professional plan. Such a plan will give them the confidence that you can successfully and professionally operate the business.

The second most common form of funding for an insurance agency is angel investors. Angel investors are wealthy individuals who will write you a check. They will either take equity in return for their funding, or, like a bank, they will give you a loan. Venture capitalists will not fund an insurance agency unless it is based on a unique, scalable technology.

Finish Your Business Plan Today!

Your insurance agency business plan should include 10 sections as follows:

Executive Summary

Your executive summary provides an introduction to your business plan, but it is normally the last section you write because it provides a summary of each key section of your plan.

The goal of your Executive Summary is to quickly engage the reader. Explain to them the type of insurance agency business you are operating and the status; for example, are you a startup, do you have an insurance agency that you would like to grow, or are you operating multiple insurance agency locations already.

Next, provide an overview of each of the subsequent sections of your plan. For example, give a brief overview of the insurance agency industry. Discuss the type of insurance agency you are operating. Detail your direct competitors. Give an overview of your target customers. Provide a snapshot of your marketing plan. Identify the key members of your team. And offer an overview of your financial plan.

Company Analysis

In your company analysis, you will detail the type of insurance agency you are operating.

For example, you might operate one of the following types:

- Direct Writer / Captive : this type of insurance agency only sells one insurance company’s products – like Allstate or State Farm

- Independent Insurance Agent : this type of insurance agency is privately-owned, and sells policies with may different insurance companies

In addition to explaining the type of insurance agency you operate, the Company Analysis section of your business plan needs to provide background on the business.

Include answers to question such as:

- When and why did you start the business?

- What milestones have you achieved to date? Milestones could include sales goals you’ve reached, new location openings, etc.

- Your legal structure. Are you incorporated as an S-Corp? An LLC? A sole proprietorship? Explain your legal structure here.

Industry Analysis

In your industry analysis, you need to provide an overview of the insurance business.

While this may seem unnecessary, it serves multiple purposes.

First, researching the insurance industry educates you. It helps you understand the market in which you are operating.

Secondly, market research can improve your strategy particularly if your research identifies market trends. For example, if there was a trend towards weather-related policy purchases, it would be helpful to ensure your plans call for flood insurance options.

The third reason for market research is to prove to readers that you are an expert in your industry. By conducting the research and presenting it in your plan, you achieve just that.

The following questions should be answered in the industry analysis section of your insurance company business plan:

- How big is the insurance agency business (in dollars)?

- Is the market declining or increasing?

- Who are the key competitors in the market?

- Who are the key insurance carriers in the market?

- What trends are affecting the industry?

- What is the industry’s growth forecast over the next 5 – 10 years?

- What is the relevant market size? That is, how big is the potential market for your insurance agency. You can extrapolate such a figure by assessing the size of the market in the entire country and then applying that figure to your local population.

Customer Analysis

The customer analysis section of your insurance agency business plan must detail the customers you serve and/or expect to serve.

The following are examples of customer segments: individuals, households, businesses, etc.

As you can imagine, the customer segment(s) you choose will have a great impact on the type of insurance agency you operate. Clearly baby boomers would want different pricing and product options, and would respond to different marketing promotions than recent college graduates.

Try to break out your target customers in terms of their demographic and psychographic profiles. With regards to demographics, include a discussion of the ages, genders, locations and income levels of the customers you seek to serve. Because most insurance agencies primarily serve customers living in their same geographic region, such demographic information is easy to find on government websites.

Psychographic profiles explain the wants and needs of your target customers. The more you can understand and define these needs, the better you will do in attracting and retaining your customers.

Finish Your Insurance Business Plan in 1 Day!

Don’t you wish there was a faster, easier way to finish your business plan?

With Growthink’s Ultimate Insurance Business Plan Template you can finish your plan in just 8 hours or less!

Competitive Analysis

Your competitive analysis should identify the indirect and direct competitors your business faces and then focus on the latter.

Direct competitors are other insurance agencies.

Indirect competitors are other options that customers have to purchase from you that aren’t direct competitors. This includes self pay and public (Medicare, Medicaid in the case of health insurance) insurance or directly working with an insurance carrier. You need to mention such competition to show you understand that not everyone who purchases insurance does so through an insurance agency.

With regards to direct competition, you want to detail the other insurance agencies with which you compete. Most likely, your direct competitors will be insurance agencies located in your geographic region.

For each such competitor, provide an overview of their businesses and document their strengths and weaknesses. Unless you once worked at your competitors’ businesses, it will be impossible to know everything about them. But you should be able to find out key things about them such as:

- What types of customers do they serve?

- What products do they offer?

- What is their pricing (premium, low, etc.)?

- What are they good at?

- What are their weaknesses?

With regards to the last two questions, think about your answers from the customers’ perspective.

The final part of your competitive analysis section is to document your areas of competitive advantage. For example:

- Will you provide superior insurance agency products/services?

- Will you provide insurance agency products that your competitors don’t offer?

- Will you make it easier or faster for customers to acquire your products?

- Will you provide better customer service?

- Will you offer better pricing?

Think about ways you will outperform your competition and document them in this section of your plan.

Marketing Plan

Traditionally, a marketing plan includes the four P’s: Product, Price, Place, and Promotion. For an insurance agency business plan, your marketing plan should include the following:

Product : in the product section you should reiterate the type of insurance agency that you documented in your Company Analysis. Then, detail the specific products/services you will be offering. For example, in addition to P&C insurance, will you also offer life insurance?

Price : Document the prices you will offer and how they compare to your competitors. Essentially in the product and price sub-sections of your marketing plan, you are presenting the menu items you offer and their prices.

Place : Place refers to the location of your insurance agency. Document your location and mention how the location will impact your success. For example, is your insurance agency located next to the Department of Motor Vehicles, or a heavily populated office building, etc. Discuss how your location might provide a steady stream of customers.

Promotions : the final part of your insurance agency marketing plan is the promotions section. Here you will document how you will drive customers to your location(s). The following are some promotional methods you might consider:

- Making your insurance agency’s front store extra appealing to attract passing customers

- Advertising in local papers and magazines

- Reaching out to local bloggers and websites

- Partnerships with local organizations (e.g., auto dealerships or car rental stores)

- Local radio advertising

- Banner ads at local venues

Operations Plan

While the earlier sections of your business plan explained your goals, your operations plan describes how you will meet them. Your operations plan should have two distinct sections as follows.

Everyday short-term processes include all of the tasks involved in running your insurance agency such as serving customers, procuring relationships with insurance carriers, negotiating with repair shops, etc.

Long-term goals are the milestones you hope to achieve. These could include the dates when you expect to acquire your 500th customer, or when you hope to reach $X in sales. It could also be when you expect to hire your Xth employee or launch a new location.

Management Team

To demonstrate your insurance agency’s ability to succeed as a business, a strong management team is essential. Highlight your key players’ backgrounds, emphasizing those skills and experiences that prove their ability to grow a company.

Ideally you and/or your team members have direct experience in the insurance agency business. If so, highlight this experience and expertise. But also highlight any experience that you think will help your business succeed.